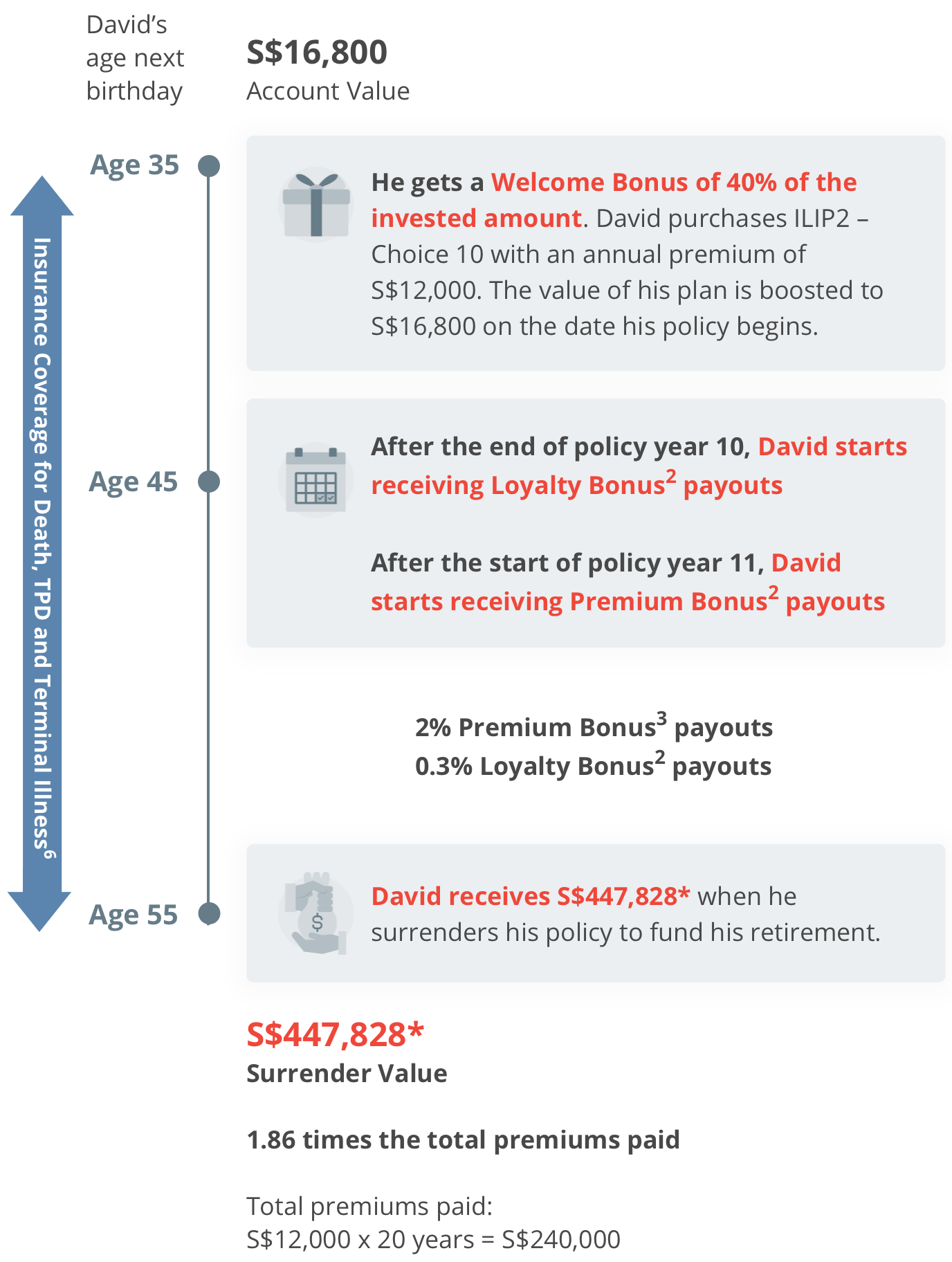

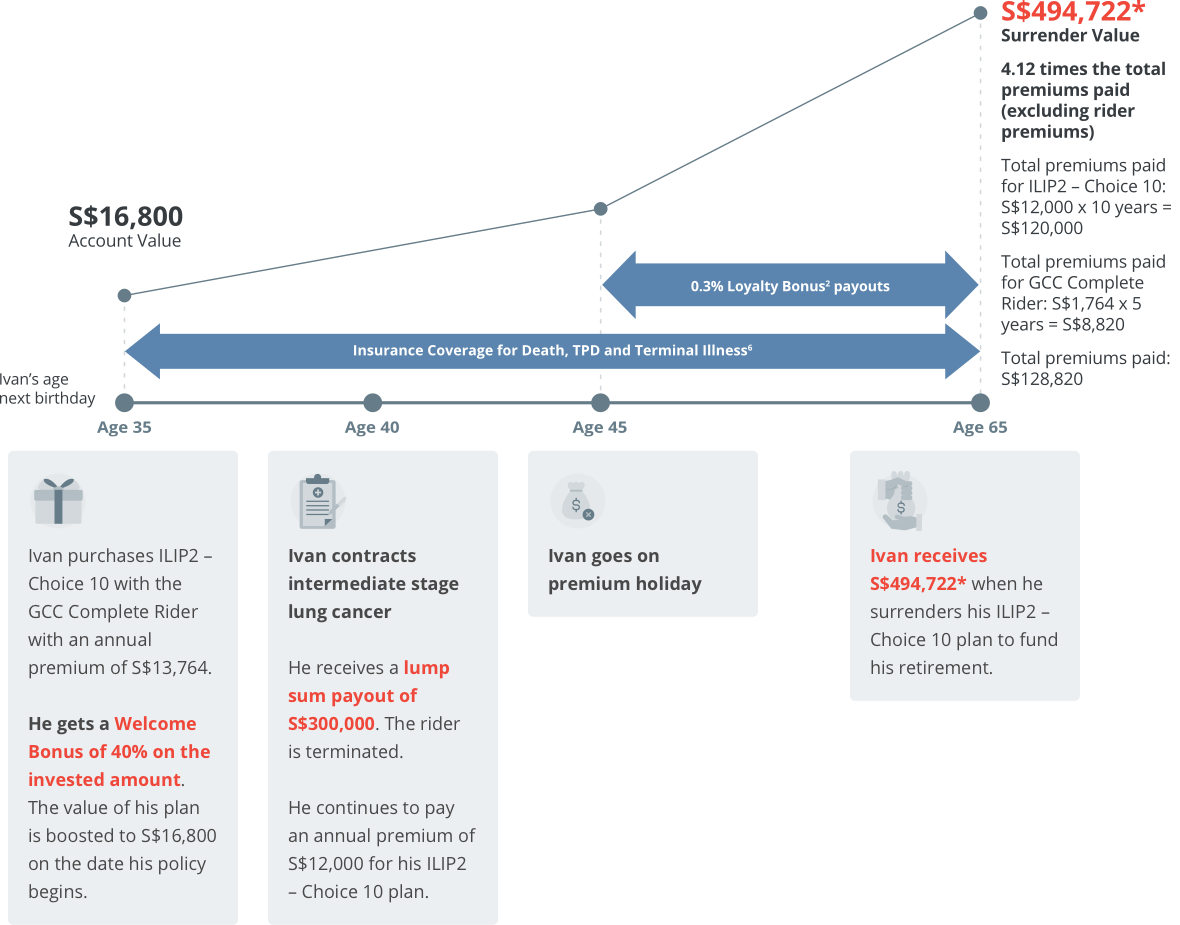

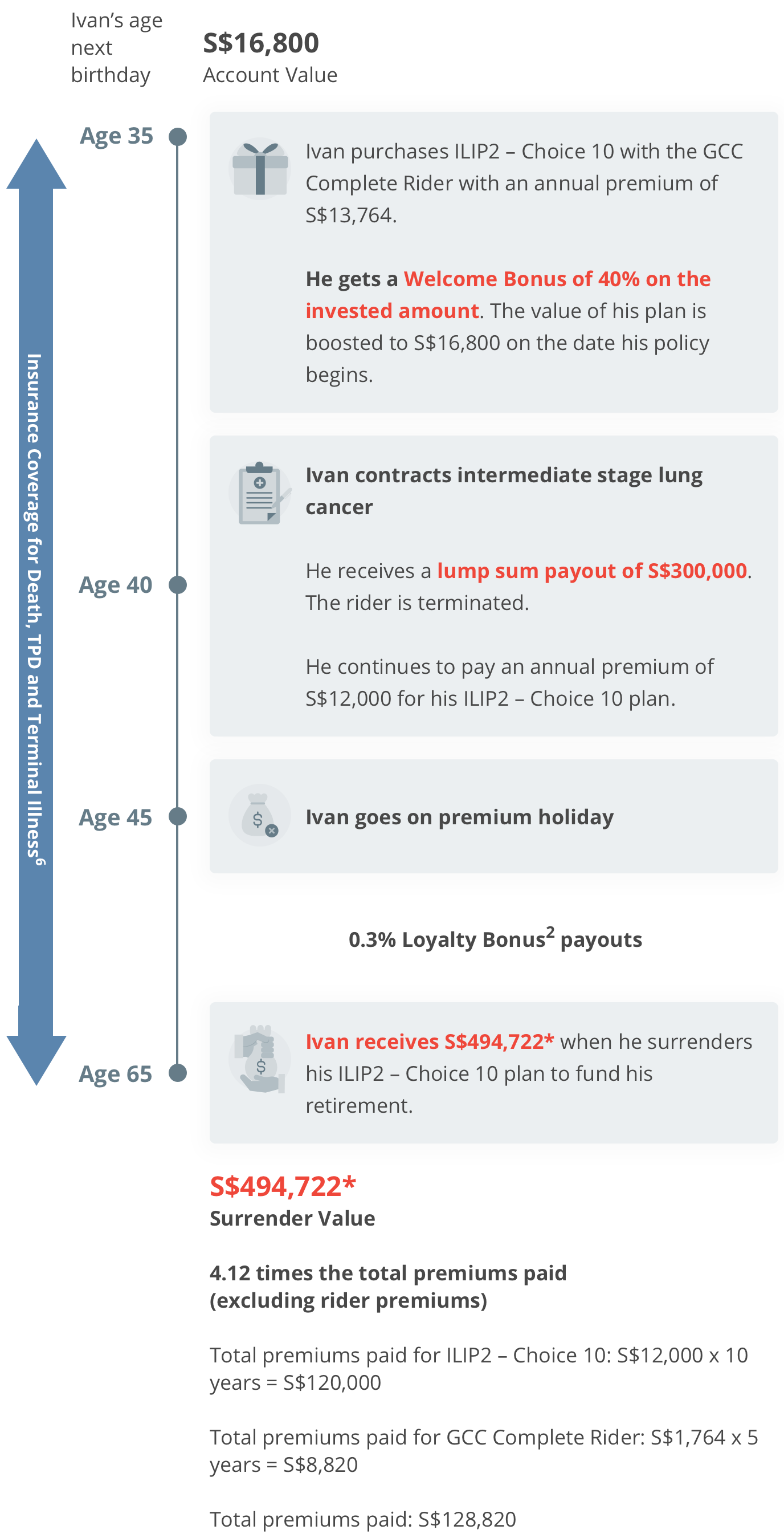

1The amount of Welcome Bonus you receive will vary depending on the plan you choose and the basic regular premiums (i.e. excluding any rider premiums) you pay annually. To enjoy 40% Welcome Bonus in the first policy year, you can apply for Investment-linked Insurance Plan 2 – Choice 10 with a basic annual premium of S$12,000 or more. After paying each modal premium in the first policy year, you will receive the bonus in the form of units to be added to your account value. The number of units to be granted will depend on the unit price available on the next valuation date following our receipt of each premium payment during the first policy year. We regret that if you are on premium holiday or make a single premium top-up, you will not earn any Welcome Bonus.

2The Loyalty Bonus you receive every year – starting from the end of the 10th policy year – will be equal to 0.30% of your policy’s value at the end of each policy year. As long as no partial withdrawals are made during the policy year for which the Loyalty Bonus is being paid for, you will receive the Loyalty Bonus in the form of extra units. The number of units to be granted will depend on the unit price available on the next valuation date following the end of the relevant policy year.

3The Premium Bonus you receive will be equal to 2% of each basic regular premium (i.e. excluding any rider premiums) you pay, starting from the year shown below. To receive the bonus, a) all prevailing basic regular premiums must be paid up to date; and b) no partial withdrawals can be made from your policy within 12 months of the date the bonus would be payable to you.

| Plan |

Premium Bonus to be paid out with each basic regular premium paid from |

| Investment-linked Insurance Plan 2 - Choice 5 |

The start of the 6th policy year |

| Investment-linked Insurance Plan 2 - Choice 10 |

The start of the 11th policy year |

4The distribution of dividends may reduce the Net Asset Value of the fund, which is used to calculate the value of the fund and the benefits you will receive under your policy. The dividend rate and frequency will vary depending on the dividend-paying funds you have chosen. Dividend distributions are not guaranteed and are determined by the relevant fund manager in its absolute discretion.

5From the second policy year, you may request to change the life assured – and do so up to two times during the policy term. If the change is approved, we will inform you in writing. For more details, please refer to the product summary.

6The Death Benefit will be payable in one lump sum as follows, if the life assured dies:

(a) 101% of total basic regular premiums paid plus 101% of total single premium top-ups paid (if any), less 101% of total partial withdrawals (if any, including any partial withdrawal charges); or

(b) the account value,

whichever is higher, less any debt (if any) owed under the policy.

If the life assured is diagnosed with a Terminal Illness or Total and Permanent Disability (TPD), the Death Benefit will be paid in one lump sum.

For TPD that takes the form of total and irrecoverable loss of the sight in both eyes; the use of two limbs at or above the wrist or ankle; or the sight in one eye and the use of one limb at or above the wrist or ankle, coverage will be for the whole of the policy term. For other forms of TPD, it must occur before the policy anniversary on which the life assured is age 65. You are advised to refer to the policy contract for more details on TPD definitions.