Sustainable investing: Five themes for 2024

Sustainable investing: Five themes for 2024

Pragmatism is the watchword as we look forward to the topics that may shape sustainable investing in the new year. Here are the five themes to watch.

Key points

- In 2024, we welcome a pragmatic, risk-based approach to addressing critical sustainability-related challenges.

- High-quality, innovative data capture increasingly allows for a robust quantification of risks that underpins ESG 2.0.

- The topic of transition will be an increasing focus, including from regulators.

Although the world heads into 2024 facing a number of sustainability-related challenges, we are encouraged by an increasingly pragmatic, risk-based approach to addressing them. This is despite some clear political divisions. As 2023 concludes, slowing economic growth, stubbornly high inflation, fragile politics and tangible evidence of climate change amount to a polycrisis – a cluster of related global risks with compounding effects as foreseen by the World Economic Forum.

But as attention turns to 2024, we think we can look forward to an important change of emphasis in key areas, even as the political context remains challenging.

1. The political agenda could pack a “delayed” punch

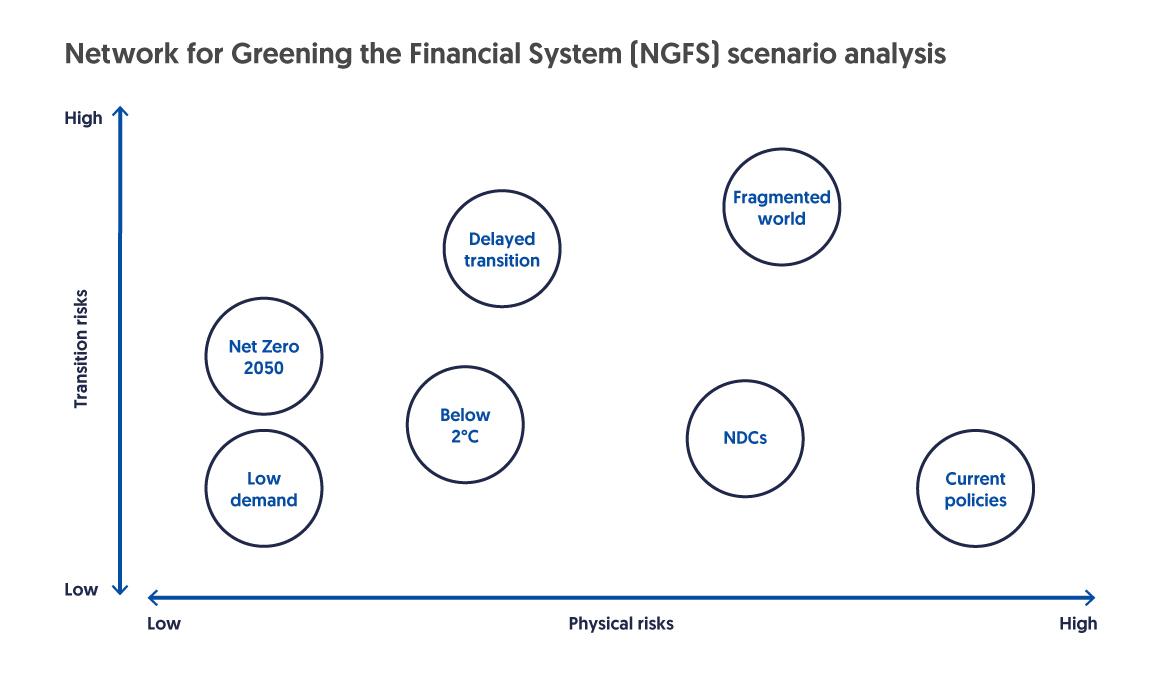

The coming year will see elections in 40 countries that together account for 41% of the global population and 42% of global GDP.1 The political resonance of the climate topic could peak in 2024 as nations grapple with the economic and cost of living challenges. This political agenda risks delaying the financing and implementation of transition plans, and could result in a higher probability of a “delayed transition scenario” as described by the Network for Greening the Financial System.2 Such a scenario has significant implications for economic growth and risk modelling; it also increases the finance needed to achieve the transition at a later date.3 Already, we are quantifying the potential impact on client portfolios in terms of the drag on returns.

Source: NGFS Scenarios Portal, https://www.ngfs.net/ngfs-scenarios-portal/explore/, November 2023

See portal for more explanation of the different scenarios.

2. From climate change to climate impact

Amid these divisions, climate is likely to shift from a distant 2050 concept to a nearer-term priority. While academic studies have modelled temperature and emission increases, they have been less effective at determining the impacts of these increases. The frequency, severity and locations of damaging weather-related events exhibit significant volatility, and the return of El Niño will likely test records in the coming year. Rising financial risk materiality could prompt a rethink, particularly given the costs of the very sizeable and rising fossil fuel subsidies.4 Meanwhile, hotter temperatures are placing additional burdens on already stretched healthcare services5 and biodiversity risks are rising within the global supply chain.6 These topics could influence future sovereign strategies and disclosures as they approach the next wave of nationally determined contributions (NDCs) – the national commitments on climate that countries make as part of the Paris Agreement.

3. ESG is dead, long live ESG 2.0

We anticipate that this greater appreciation of risk materiality will trigger a revived – and significantly refined – return of ESG. When the term “ESG” was introduced in 2004, it sought to broadly classify the key factors contributing to an entity’s long-term operating and financial resilience.7 This was often simply summarised into a blunt, overly simplified ESG score. Since then, ESG has suffered mission creep. It is increasingly associated with “doing good” or imposing values or responsible investing outcomes. In addition, it was assessed using opaque, qualitative assessments with low correlation among the main providers.8 Now, however, we see a trend in high-quality, innovative data capture that will allow for a robust quantification of both impact and dependency risks at company, sector and regional levels. You can expect a thematic paper from us in 2024 on how we will evolve our risk materiality data capture in our Sustainability Insights Engine (SusIE) to include new innovative specialist provider offerings, alongside reviewing new artificial intelligence (AI) data capture techniques.

4. From the transition of regulation to the regulation of transition

The past year has seen sustainability regulation move from fatigue to functioning. With the UK’s proposed Sustainability Disclosure Requirements (SDR), the ASEAN Taxonomy9 and subsequent adjustments to the European Union’s Sustainable Finance Disclosure Regulation (SFDR), we appear to be entering a more pragmatic “norming” phase. As a result, we expect a greater regulatory focus on the concept of “transition”10 to be steadily embedded into climate, impact and sustainability investment frameworks. In September 2023, this was underscored by the Glasgow Financial Alliance for Net Zero, which launched a consultation on transition finance strategies.11 We expect “just transition” to be a focus again at the COP 28 meeting12 amid greater clarity around just energy transition partnerships, which direct money from wealthier economies to support developing nations as they shift away from fossil fuels.13

5. Finding a solution with impact

In 2023, the World Economic Forum issued several publications around the need to invest in solutions, ranging from existing technologies that need to be scaled up to those that do not currently exist. At a time when the market focus is on lowering footprints (i.e, the impact that an entity itself has), we need to focus on the handprint opportunities to facilitate this mitigation – in other words, the solutions that will support widescale improvements. The public markets can learn from the private markets and impact investing worlds on how they articulate and measure positive impact, and the governance around targeting and achieving this impact through the life cycle of a project.

In July 2023, we published a whitepaper on how we at Allianz Global Investors approach the topic14 as we roll out new client offerings, and we expect some of the notions we discussed to be increasingly influential in public markets next year.

Sources:

1Bloomberg, November 2023

2NGFS – Network for Greening the Financial System, November 2023

3International Monetary Fund, October 2022

4International Monetary Fund, August 2023

5Health is wealth?, Allianz Global Investors, October 2023

6The rules of engagement to protect biodiversity, Allianz Global Investors, June 2023

7UN Environment Programme Finance Initiative, 2004

8CFA Institute, August 2021

9ASEAN Taxonomy for Sustainable Finance, November 2023

10OECD, November 2023

11Glasgow Financial Alliance for Net Zero, September 2023

12UN Climate Change, July 2023

13International Institute for Sustainable Development, December 2022

14Investing for meaningful impact in private markets, Allianz Global Investors, July 2023

Important information

This advertisement has not been reviewed by the Monetary Authority of Singapore. Cross-Border Market Disclaimers