Global Renewables - Race to build the future

Global Renewables - Race to build the future

Investment summary

Prior to Russia’s invasion of Ukraine, countries were already stepping up on their investments in renewable energy. China, for example, is expected to install almost half of new global renewable power capacity over 2022-2027, according to the International Energy Agency (IEA). The war expedited Europe’s clean energy transition as energy security emerged as a strong motivator to accelerate renewable energy deployment. In the US, the Inflation Reduction Act (IRA) provided unprecedented long-term policy visibility for wind and solar projects, amongst other energy transition projects.

Indeed, the US IRA has significant implications. Ever since it was released last year, there have been cheers from various companies and stakeholders, especially the potential beneficiaries of the Act. Most of the positive sentiment was understandably concentrated in the US and companies overseas with close business ties to the US. In Europe, apart from companies that already have operations in the US which can benefit from the IRA and those who supply to US beneficiaries, there have been concerns that potential capital may be attracted to the US instead, along with potential trade barriers that may keep out non-US companies. As such, the European Commission (EC) published its proposal for the EU “Green Deal Industrial Plan for the Net-Zero-Age”, which is meant to be the EU’s response to the US IRA.

Beneficiaries in the renewable energy industry include solar/wind installers, module and equipment makers as well as asset owners which range from traditional energy players to utility companies developing solar and wind farms. We believe the stimulus ahead is meaningful at both the sector and company levels, providing opportunities for investments in equities across the supply chain. Investors should note, however, that this is a multi-year theme with time required for incremental investments as well. Geopolitical tensions are also set to persist in renewables, a strategic area of importance for countries.

Countries are racing to increase their renewable energy capacities

Prior to Russia’s invasion of Ukraine, countries were already stepping up on their investments in renewable energy. China, for example, is expected to install almost half of new global renewable power capacity over 2022-2027, according to the IEA. The war expedited Europe’s clean energy transition as energy security emerged as a strong motivator to accelerate renewable energy deployment. In the US, the IRA provided unprecedented long-term policy visibility for wind and solar projects, amongst other energy transition projects.

Europe to finalise own version of the IRA

Indeed, the US IRA has significant implications. Ever since it was released last year, there have been cheers from various companies and stakeholders, especially the potential beneficiaries of the Act. Most of the positive sentiment was understandably concentrated in the US and companies overseas with close business ties to the US. In Europe, apart from companies that already have operations in the US which can benefit from the IRA and those who supply to US beneficiaries, there have been some concerns that potential capital may be attracted to the US instead, along with potential trade barriers that may keep out non-US companies.

As such, the EC published its proposal for the EU “Green Deal Industrial Plan for the Net-Zero-Age”, which is meant to be the EU’s response to the US IRA. In the paper, the EC details one main objective: to achieve a massive increase in the manufacturing of net-zero equipment and the installation of clean energy products. The plan builds on previous initiatives and relies on the strengths of the EU Single Market, complementing ongoing efforts under the European Green Deal and REPowerEU.

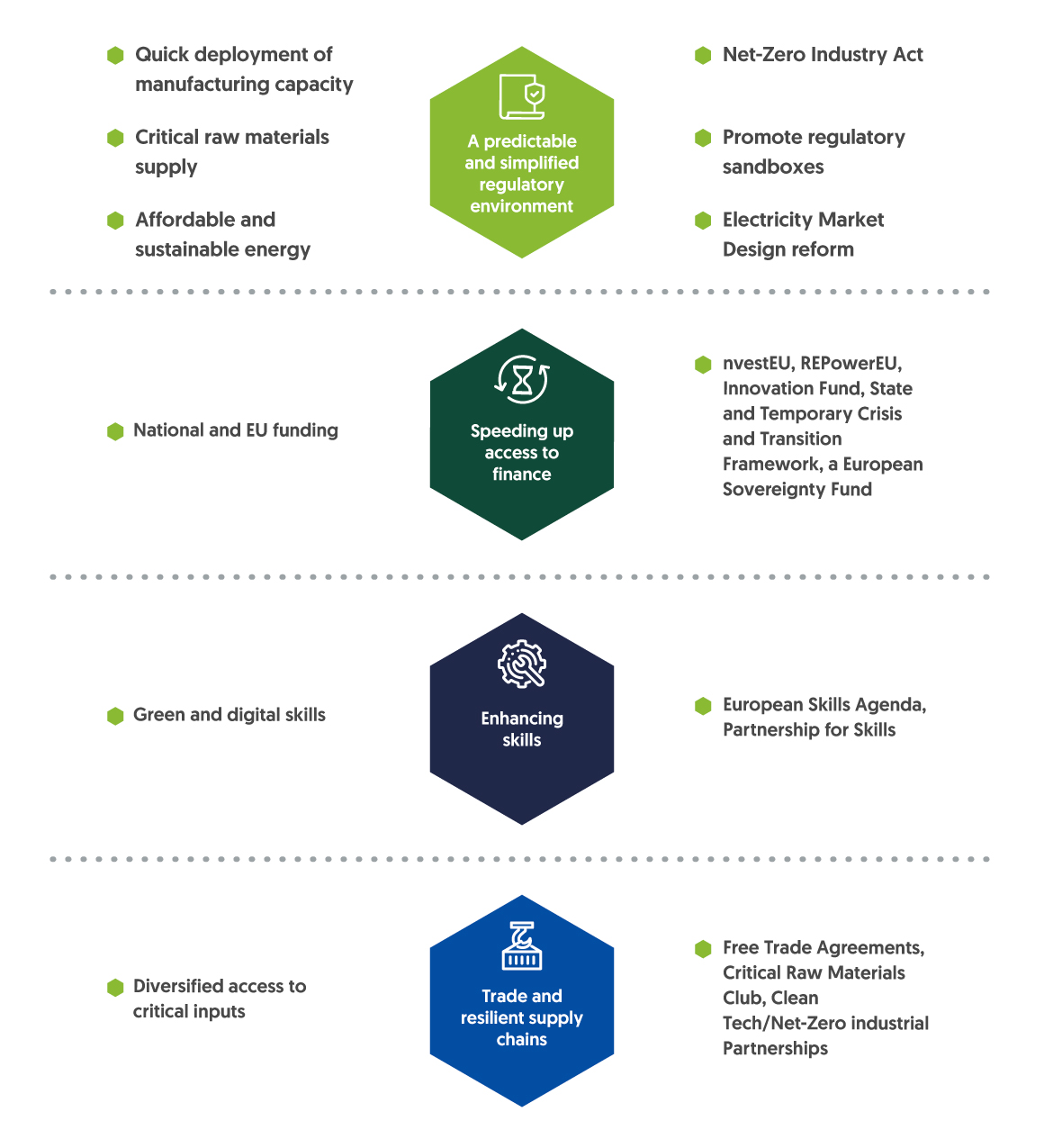

Based on four pillars, the plan seeks to 1) build a predictable and simplified regulatory environment, 2) speed up access to finance, 3) enhance relevant skills, and 4) open trade for resilient supply chains.

Exhibit 1: Four pillars of the Green Deal Industrial Plan

Source: European Commission

Within these measures, the introduction of the second point (speeding up access to finance) is a new measure. The relaxation of state aid regulations for the sector under the Temporary Crisis Framework would enable EU member states to support new investments in production facilities in defined, strategic net-zero sectors, including tax benefits. In terms of EU funding, the EC refers to the REPowerEU (~EUR250b Recovery and Resilience Facility (RRF) grants and loans), InvestEU programme (over EUR372b in additional investment to be mobilised between 2021-2027) and Innovation Fund (~EUR40b) as their financing vehicles for the EU’s net-zero industry, with REPowerEU being the dedicated funding vehicle.

We do point out that this interpretation of the plan remains incomplete with some parts still difficult to project, given the need for further clarification through additional discussions and firmer proposals from the EC.

Geopolitical trade tensions and risks in renewables, a strategic area of importance

Besides inducing concerns in Europe, the US IRA also resulted in uncertainty amongst some Chinese renewable energy companies. This was in addition to some developments relating to import tariffs.

On 8 February 2022, Auxin Solar, a US solar module maker, filed a petition to request the investigation of imported modules from Southeast Asia (SEA), which allegedly bypassed tariffs. The US Department of Commerce started to investigate whether solar imports coming from SEA include materials sourced from China, which could be viewed as circumventing anti-dumping/countervailing duties imposed in 2012 by the US on Chinese products. Note that Chinese module makers have expanded capacity in SEA a few years ago, as they would manufacture and ship their module products from SEA to the US.

The White House then announced in early June 2022, through an administrative order from US President Joe Biden, that the US will not impose new tariffs on solar imports from SEA for two years, while also invoking the Defence Production Act to promote domestic solar manufacturing. The US Department of Commerce’s investigation would continue, but no tariffs will be imposed for two years.

Subsequently, in December 2022, the US Department of Commerce released its preliminary determination wherein four out of the eight companies they have investigated have been found to be circumventing the rules. A final determination will be made in May 2023. Given Biden’s earlier decision, tariffs will not be imposed until June 2024. The companies not listed will be permitted to certify individually whether they are circumventing or not.

Exhibit 2: US Department of Commerce preliminary determination

| Third Country | Company | Finding |

| Cambodia | BYD HK | Circumventing |

| New East Solar | Not circumventing | |

| Malaysia | Hanhwa | Not circumventing |

| Jinko | Not circumventing | |

| Thailand | Canadian Solar | Circumventing |

| Trina | Circumventing | |

| Vietnam | Boviet | Not circumventing |

| Vina Solar (LONGi's subsidiary) | Circumventing |

Source: US Department of Commerce

As seen from Exhibit 2, firms such as BYD HK, Canadian Solar, Trina Solar and Vina Solar (a subsidiary of LONGi Green Energy Technology) have been found to be “circumventing”.

Implications for China’s solar sector

Given the two-year tariff exemption, we expect the negative impacts to be realised from 2H24. US markets make up ~9% of the total demand in 2022 (based on Bloomberg New Energy Finance estimates) and around 1/3 of demand is satisfied by thin-film technology (a type of product the China solar value chain does not produce). Thus, the implication on the addressable market size for China solar is even smaller. Meantime, we expect share price performance to be driven more by the cycle of individual components in 2023, such as polysilicon prices.

Given the strategic importance of solar energy to countries, the EU and US could diversify away from China’s solar supply chain due to policies surrounding forced labour and planned industry subsidies. As such, China’s global solar market share may decline as a result. In the near-term, however, given rapidly rising demand and limited available capacity in the EU and the US, China’s exports could still remain supported over the next few years. Over the longer-term, import tariffs and local subsidies may offset China’s cost advantage.

Important information

This advertisement has not been reviewed by the Monetary Authority of Singapore. Cross-Border Market Disclaimers