Analysing greenhouse gas emissions: It’s not as easy as 1-2-3

Analysing greenhouse gas emissions: It’s not as easy as 1-2-3

Finance professionals dedicate significant time to scrutinising companies’ financial statements. It is fundamental to ensuring financial performance is accurately reflected. As companies increasingly set climate targets, applying the same level of rigour to analysing emissions data becomes essential – but this is no easy process. Emissions accounting is fraught with complexities and inconsistencies. We explore the key challenges investors face, and the steps they can take to overcome them.

The common standard for accounting for carbon emissions is the Corporate Accounting and Reporting Standard, developed by GHG Protocol. This organisation was established in 1998 as a collaboration between governments, industry associations, NGOs and corporations, and it provides guidance to companies on how to measure and report their GHG emissions. More than 9 out of 10 Fortune 500 companies reporting to CDP (formerly the Carbon Disclosure Project) use GHG Protocol directly or indirectly.

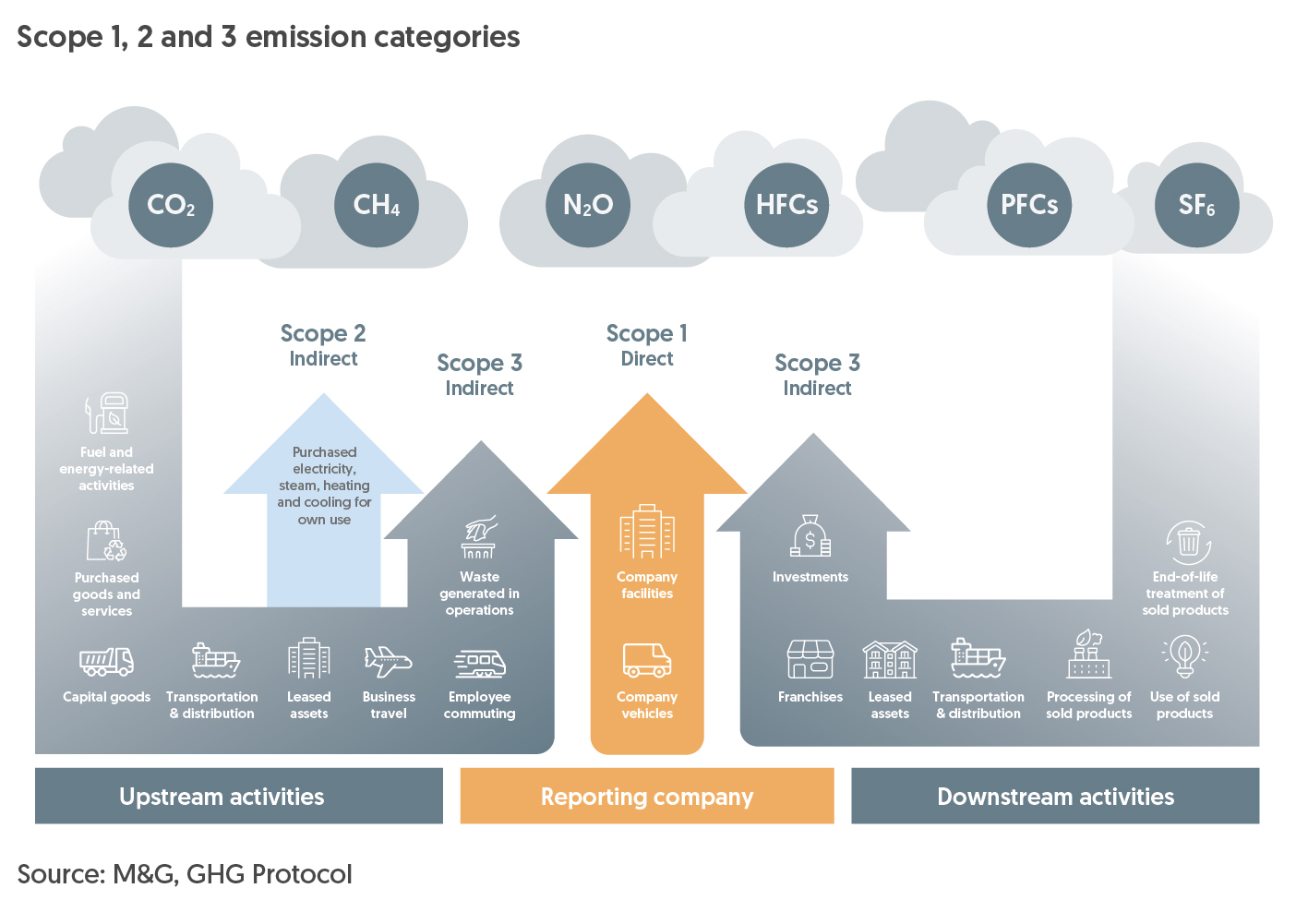

The standard defines three areas or “scopes” of emissions, which together account for a company’s total direct and indirect emissions. Scopes 1 and 2 relate to the operations of the business – the former being from company-owned assets, and the latter from electricity purchased from energy suppliers.

Scope 2 can be categorised further as location-based emissions, derived from the emissions intensity of the grid where the operations occur, and market-based, which reflects the emissions of the actual electricity contracts purchased. This means that if a company enters into a power purchase agreement (PPA) to procure renewable energy, for example, this will reduce market-based emissions but not location-based emissions. We therefore believe that market-based figures give a truer reflection of a company’s efforts to reduce its emissions.

Emissions in the supply chain

A company’s carbon footprint extends beyond its own operations, and includes emissions in its wider supply chain. These are accounted for in Scope 3, which is split into 15 categories, covering both upstream and downstream emissions. Upstream emissions include purchased goods, transportation of goods and employee commuting, while downstream emissions include the use of products sold by the company and end-of-life treatment of products. When it comes to reducing emissions, some areas can be much more easily influenced than others, such as the choice of suppliers compared to the use of products.

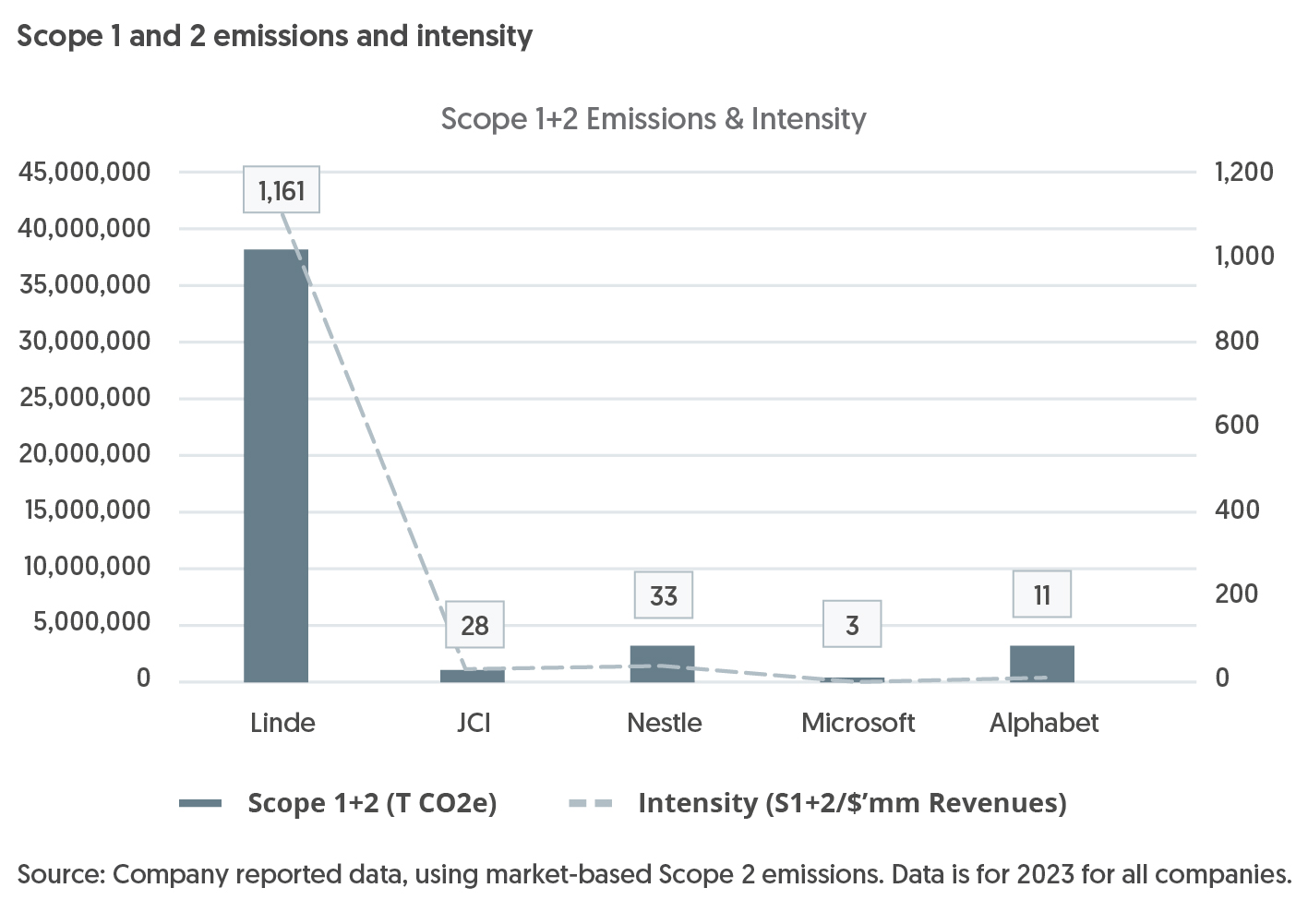

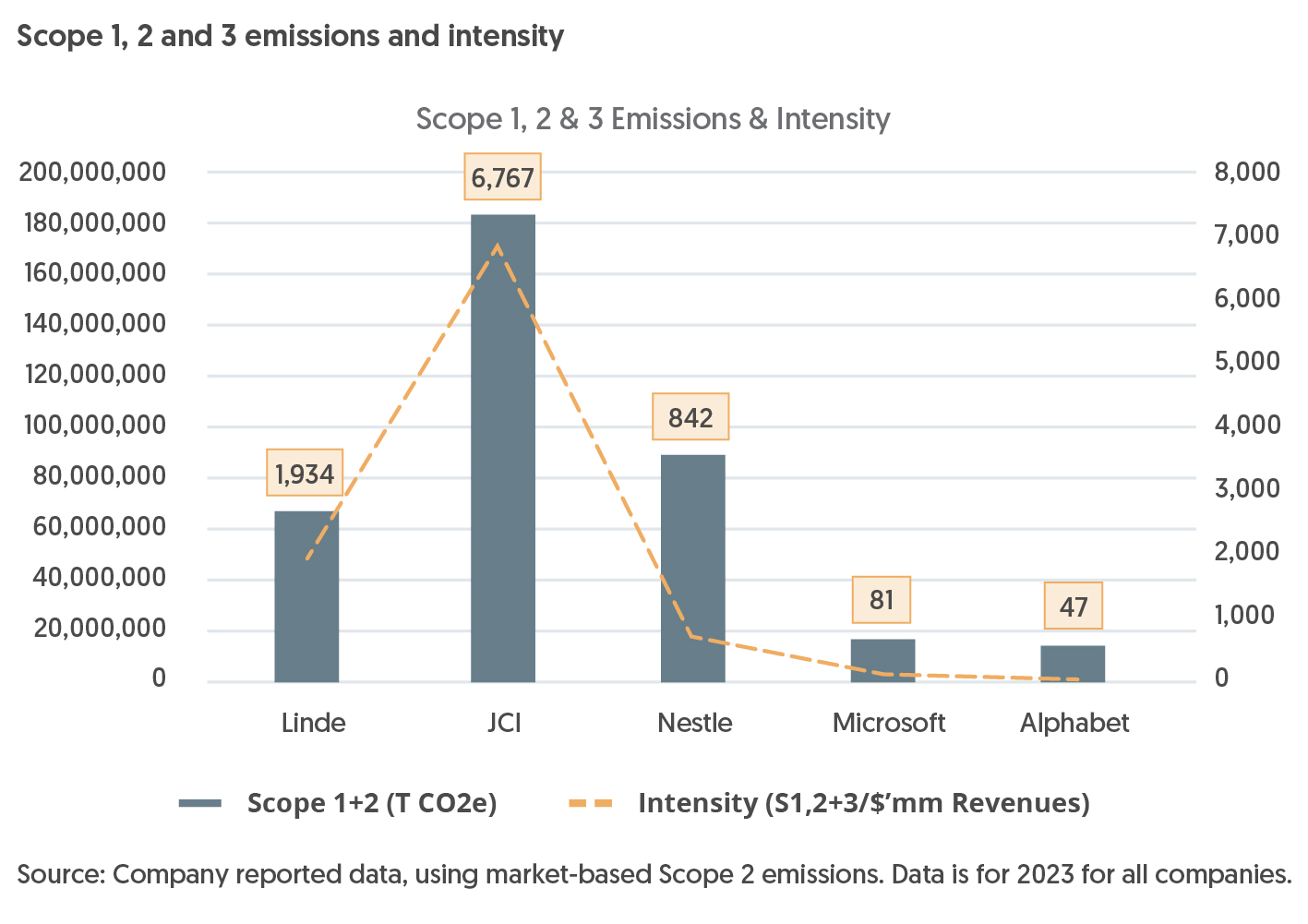

Scope 3 emissions can be a material contributor to a company’s carbon footprint, although this tends to vary across industries. For example, Linde is an industrial gases company held in our Sustain Paris Aligned strategies. The company reports materially higher emissions from its own operations than other investees, such as Johnson Controls (JCI), a heating controls company, and Nestlé. However, when Scope 3 emissions are included, Johnson Controls and Nestlé’s absolute emissions are two to three times higher than Linde’s. This can be explained by the use of energy in JCIs heating control products, and upstream emissions from dairy in the case of Nestlé.

Conversely, technology companies tend to maintain a low level of Scope 3 emissions, unless they provide cloud computing services, such as Microsoft. Furthermore, when emissions are adjusted for the size of their operations (using revenues), they are among the least carbon intensive companies.

Scope 3: the wild west of emissions data

To make analysts’ jobs more difficult, Scope 3 emissions can be subject to large discrepancies in methodologies and estimates. This can affect the ability to effectively assess a company’s emissions performance compared to peers.

For example, assessing emissions from the use of a company’s products involves many management estimates, unlike emissions produced from the company’s own operations, which should be more easily measurable – akin to reading your own electricity meter at home. Furthermore, as with financial accounting, management teams can take differing approaches to measurement. This makes it challenging to make apples-with-apples comparisons across companies and industries. But contrary to financial accounting, judgements are not always made in the favour of the reporting company.

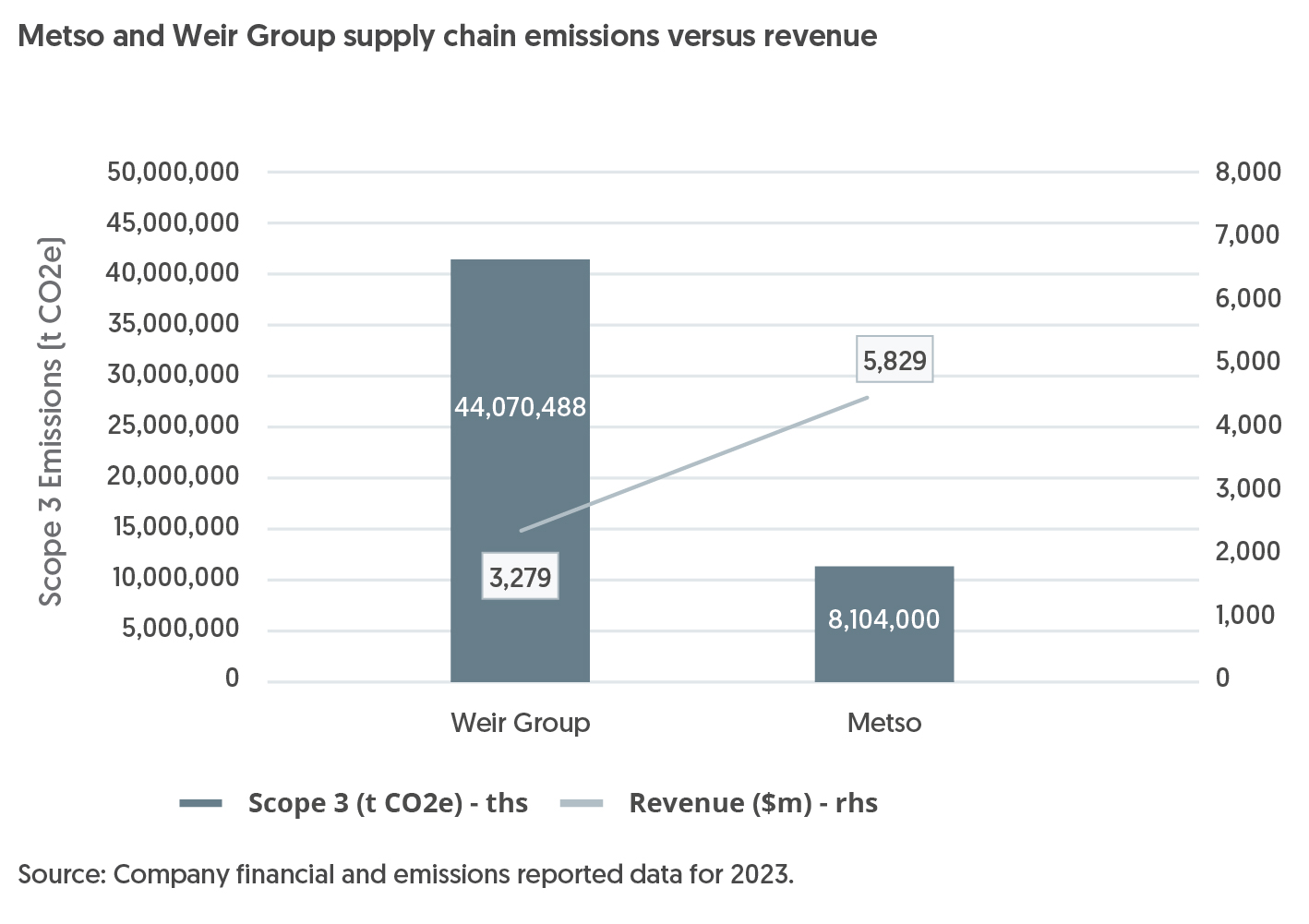

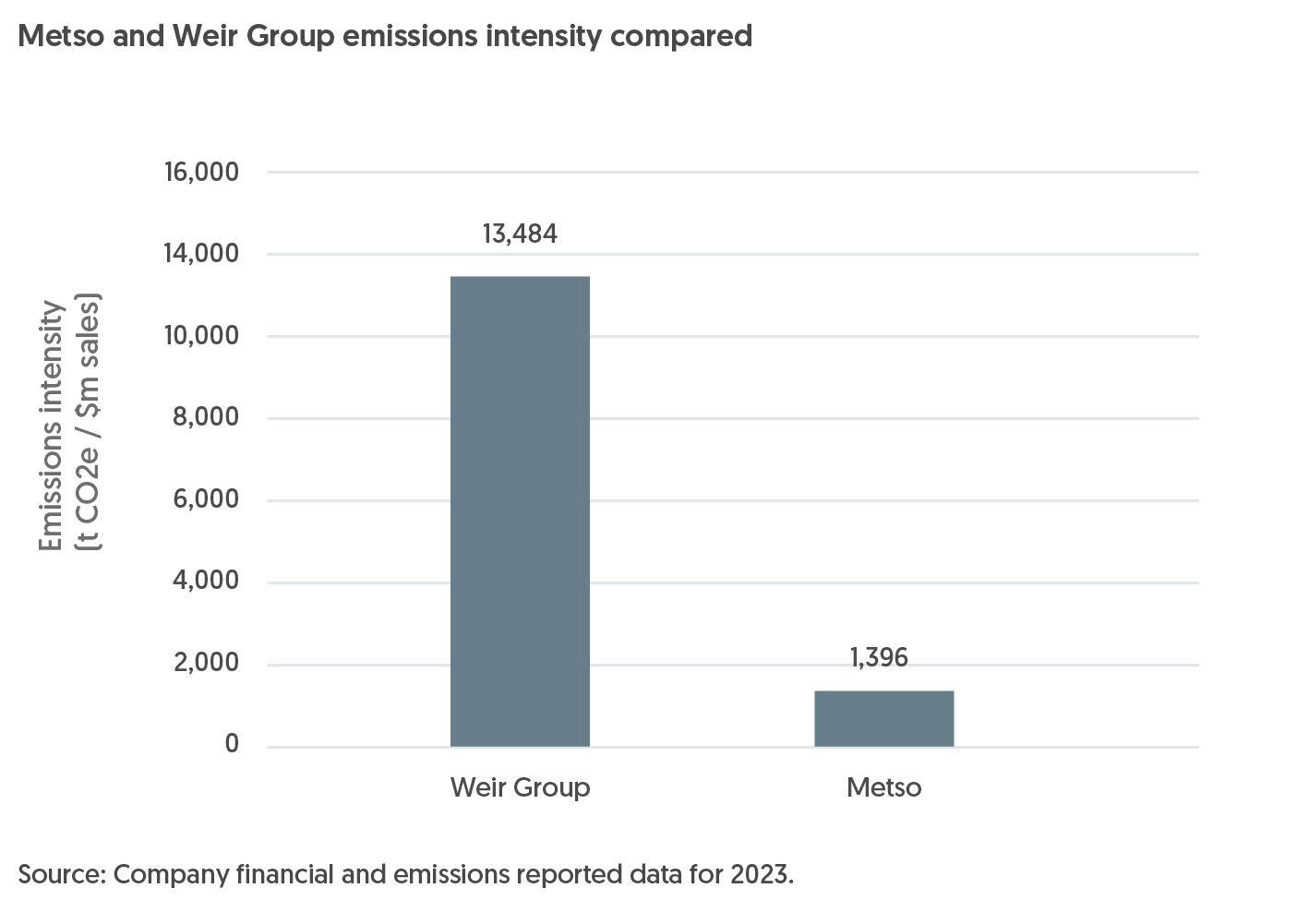

A clear example of this is Metso and Weir Group, two holdings in our Sustain Paris Aligned strategies that produce industrial equipment and operate in similar markets. While Metso is twice as large as Weir Group, the latter has reported Scope 3 emissions that are five times higher than the former.

This is because Weir Group takes the approach of accounting for every piece of equipment it has ever sold that is currently in use, whereas Metso only accounts for equipment sold in that year. Weir Group’s equipment has an assumed average lifetime of 20 years, and therefore this has a material effect on the difference between the two. As a result, when including supply chain emissions, Weir Group appears to have a carbon intensity that is 10 times greater than Metso.

But we can’t analyse what we don’t have...

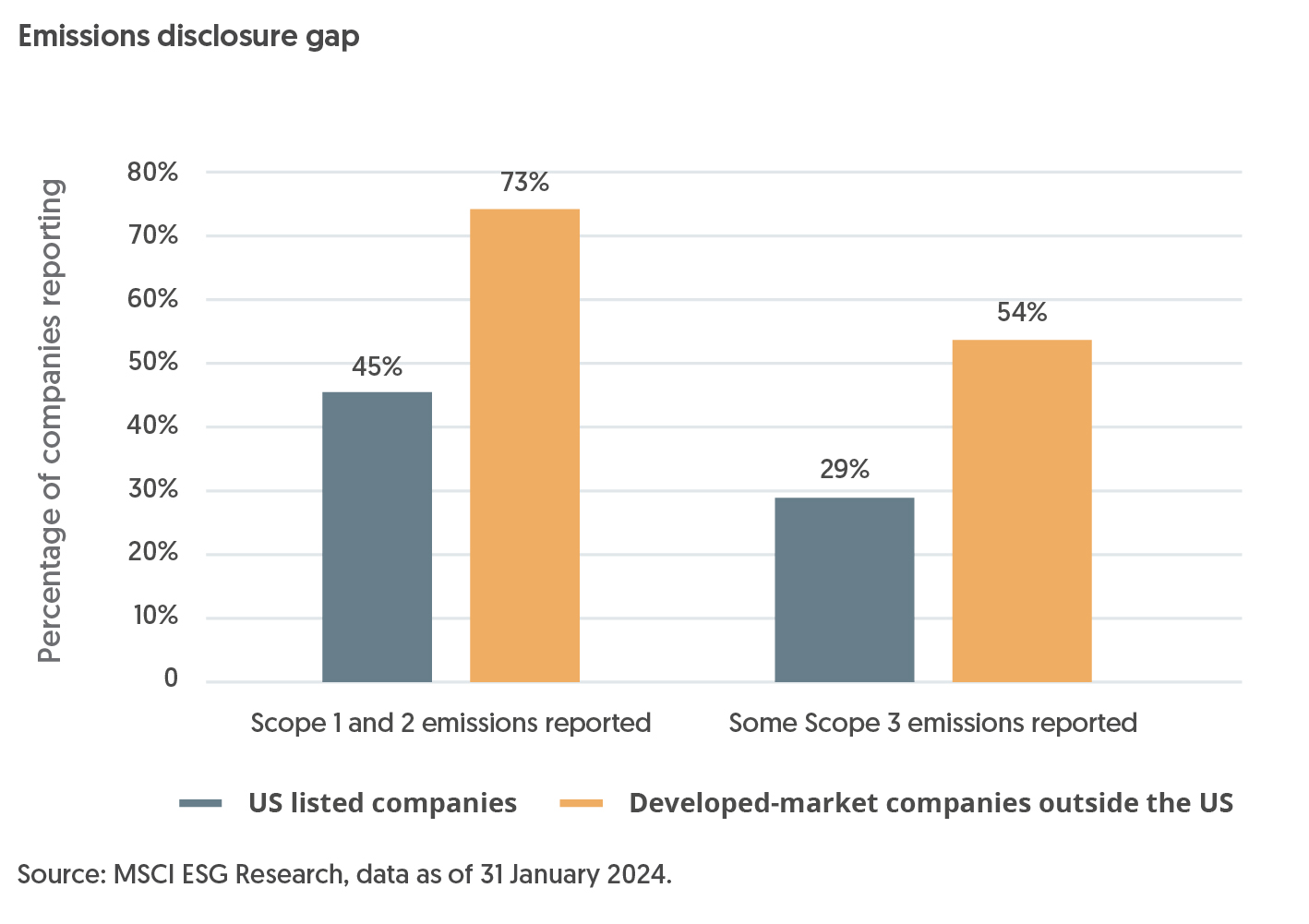

In addition to the challenges of comparing emissions across companies and industries, reporting of emissions, particularly Scope 3, is still sporadic and often only includes a select few categories. For example, MSCI reports that as of January 2024, only 60% of listed companies disclose Scope 1 and/or 2 emissions, while only 42% report any Scope 3 categories. However, disclosure is improving, with the former increasing by approximately 16 percentage points and the latter by 17 percentage points since January 2022.

The increase has been catalysed by regulation, such as the European Union’s Corporate Sustainability Reporting Directive (CSRD), which requires emissions disclosures by companies starting in 2025, and the SEC’s climate disclosure rules. These should ensure a continued increase in emissions reporting over the coming years, while also narrowing the wide gap in disclosures between US and European companies across all scopes.

The rigour with which financial analysts approach financial accounting should also be applied to companies’ GHG emissions, to avoid misinterpreting the figures. Furthermore, we must understand the true reflection of a company’s efforts to reduce its emissions. The work of an analyst just became more challenging – but at least, we believe it is more meaningful.

Important information

This advertisement has not been reviewed by the Monetary Authority of Singapore. Cross-Border Market Disclaimers