Understanding the financial wellness of Singaporeans

Economic uncertainty and market volatility have impacted Singaporeans' financial wellness in 2022.

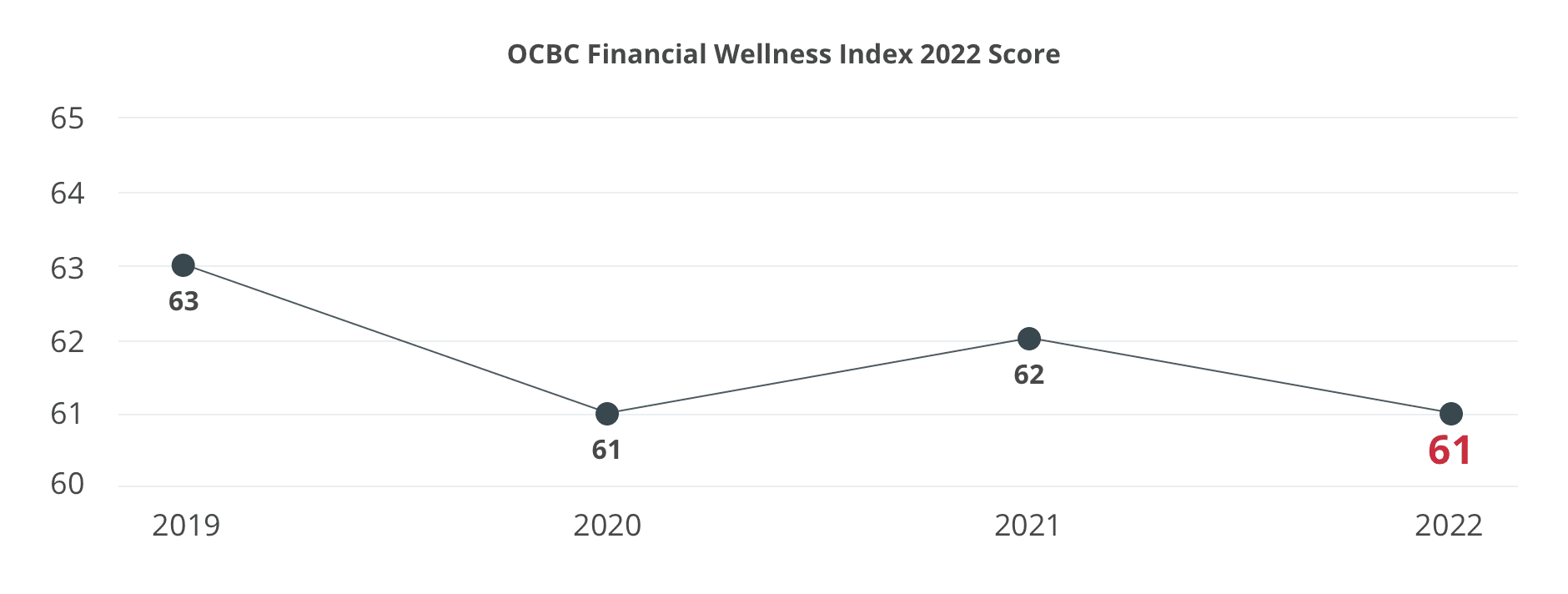

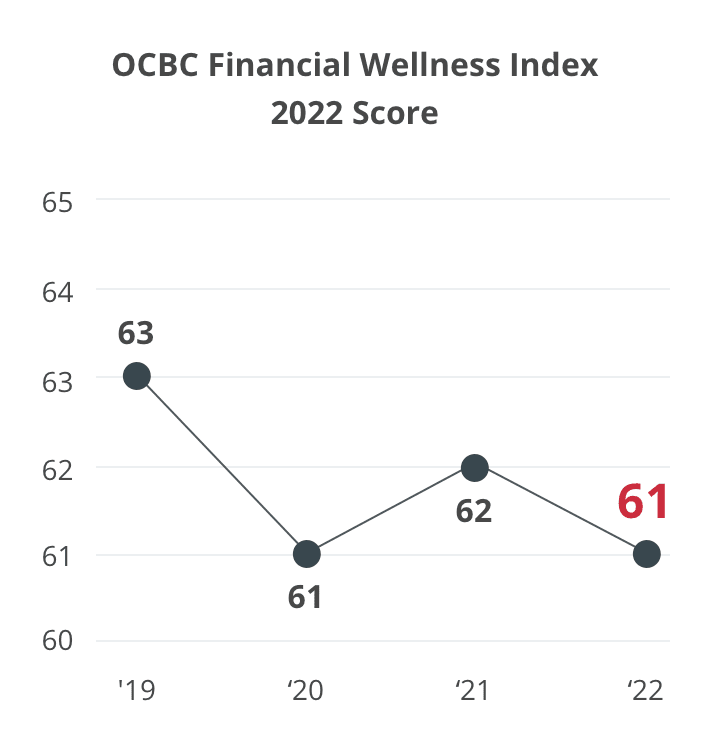

The OCBC Financial Wellness Index 2022 dipped one point from last year to 61.

Inflation, rising interest rates and a market downturn led to poorer investment returns, fewer Singaporeans being on track with retirement goals, and increased debt stress. This resulted in a net negative impact on Singaporeans’ financial wellness compared to last year:

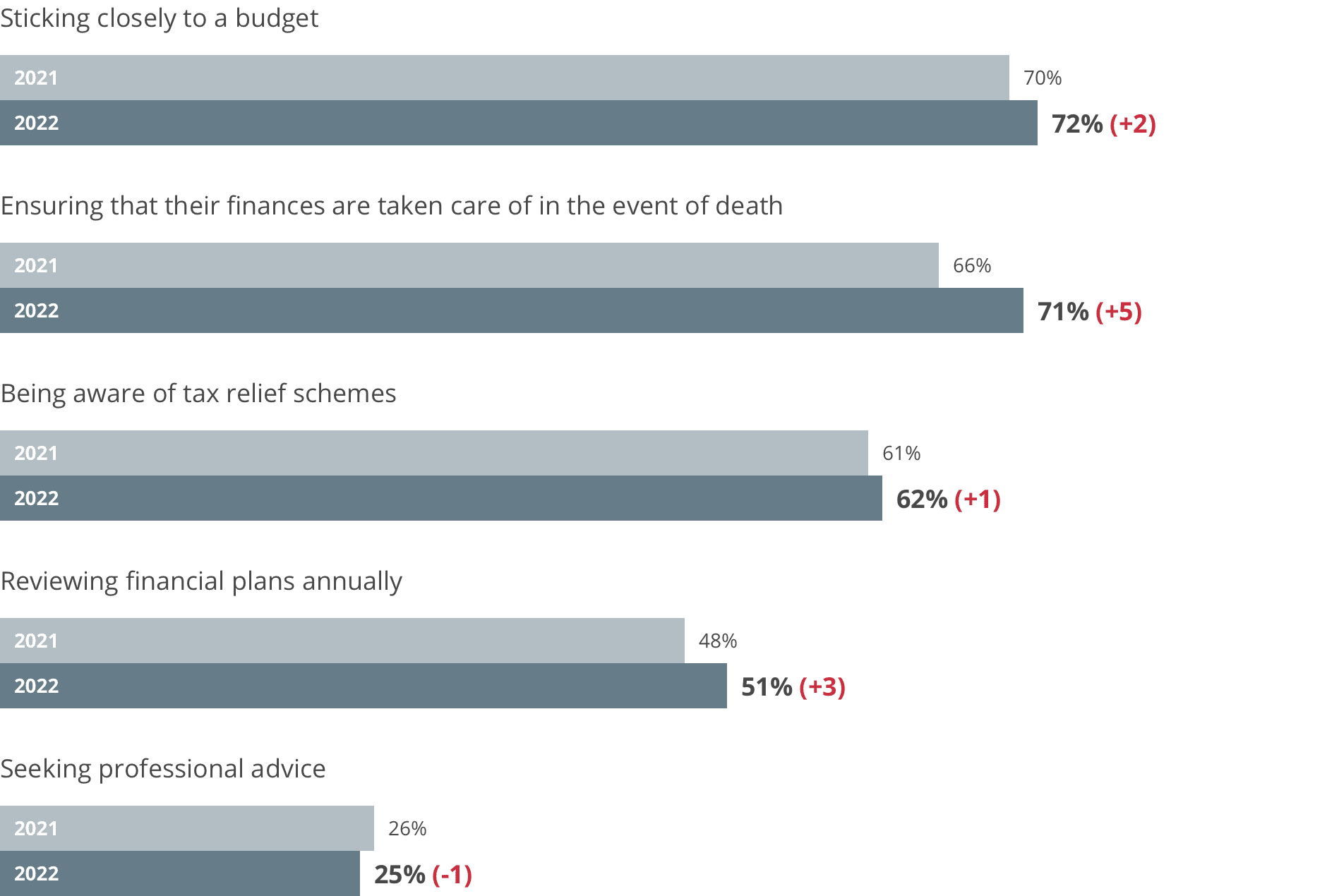

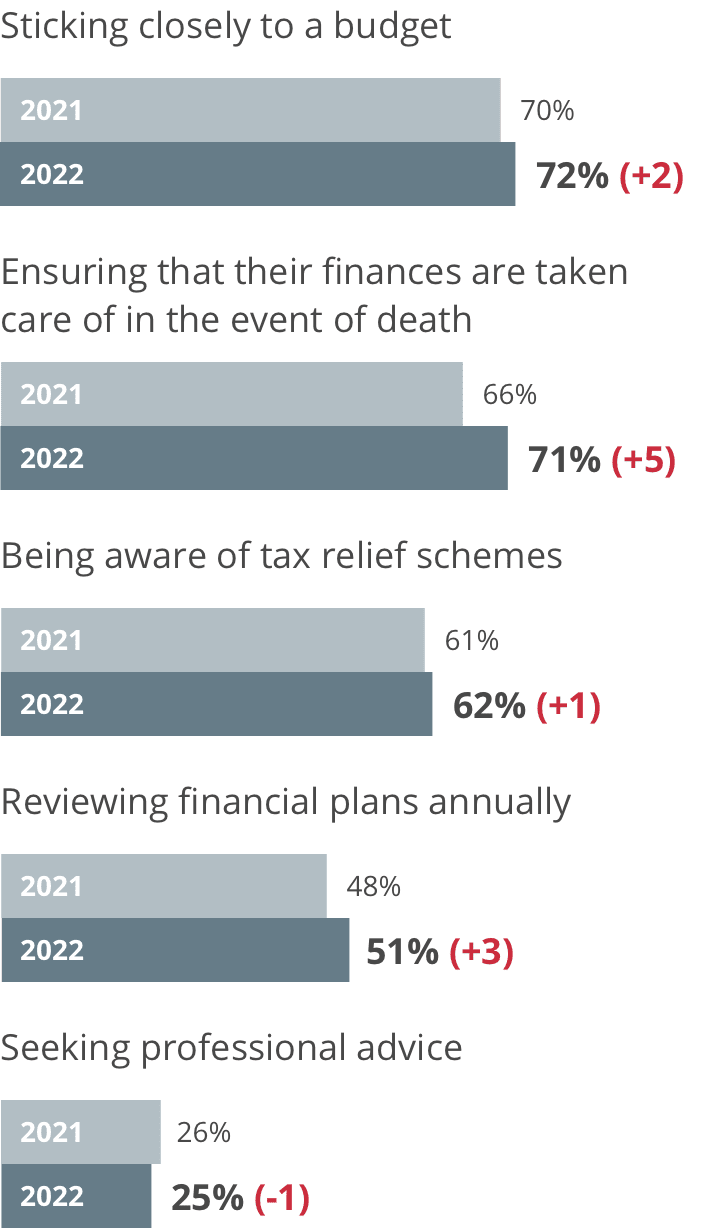

While Singaporeans persisted with financial virtues such as:

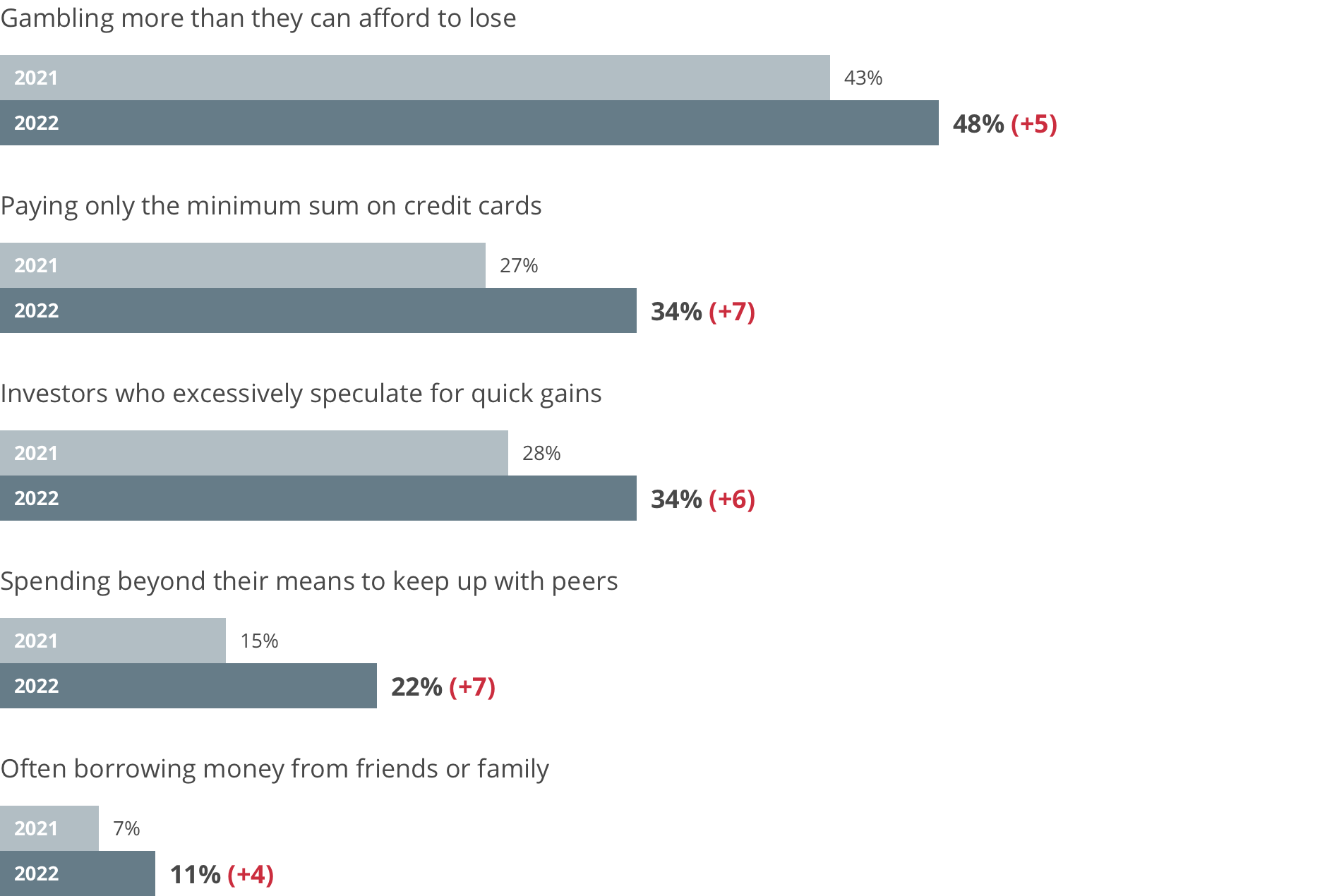

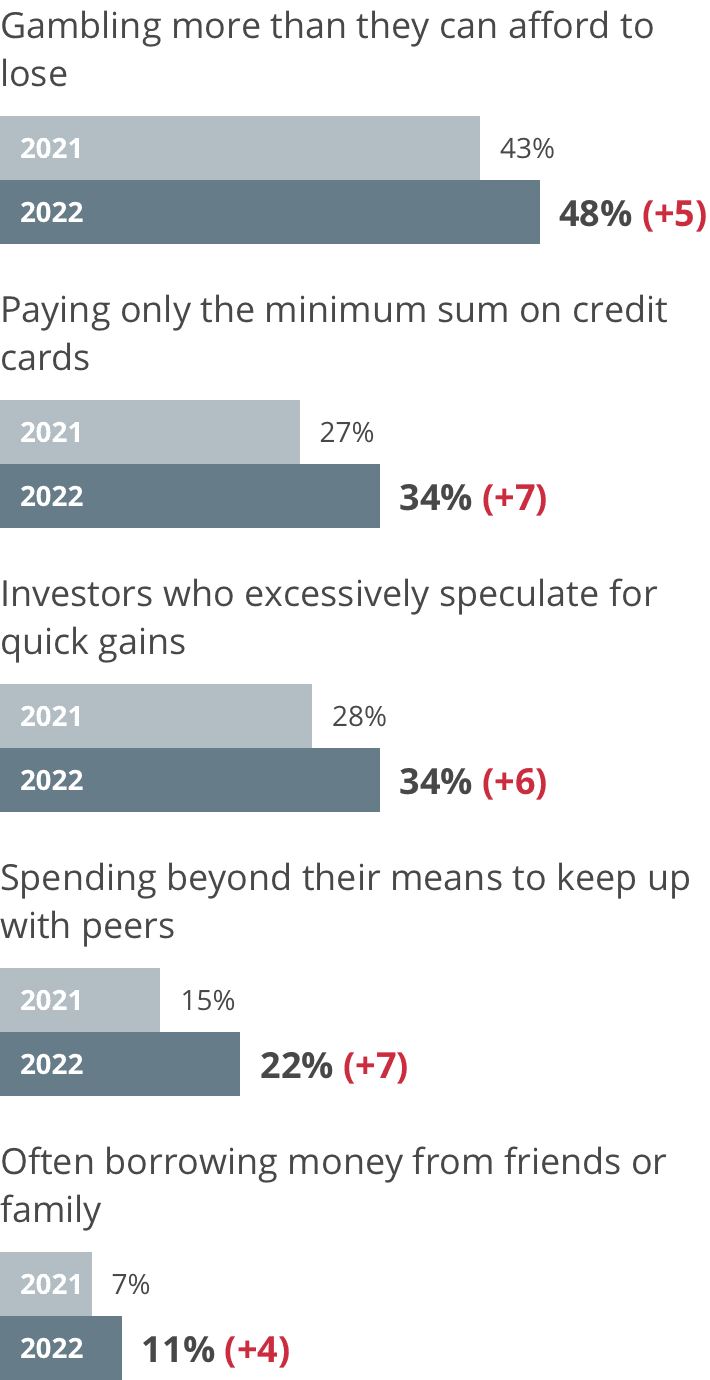

More Singaporeans committed undesirable financial habits:

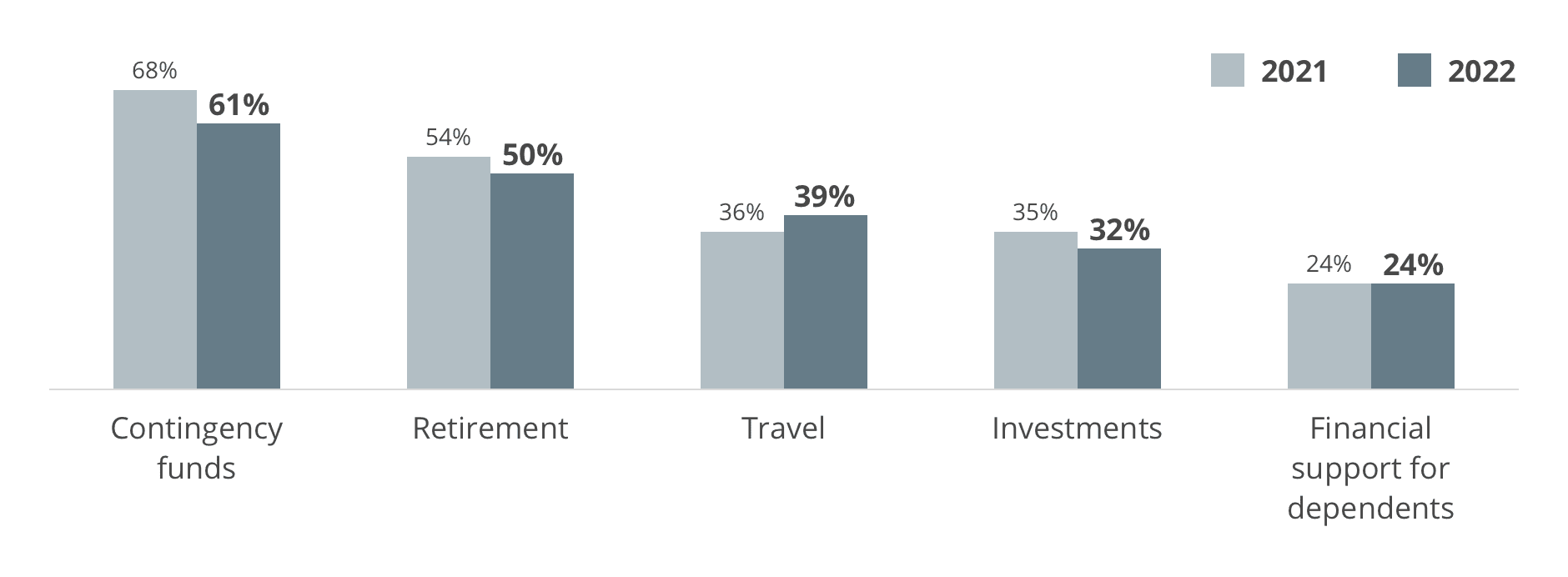

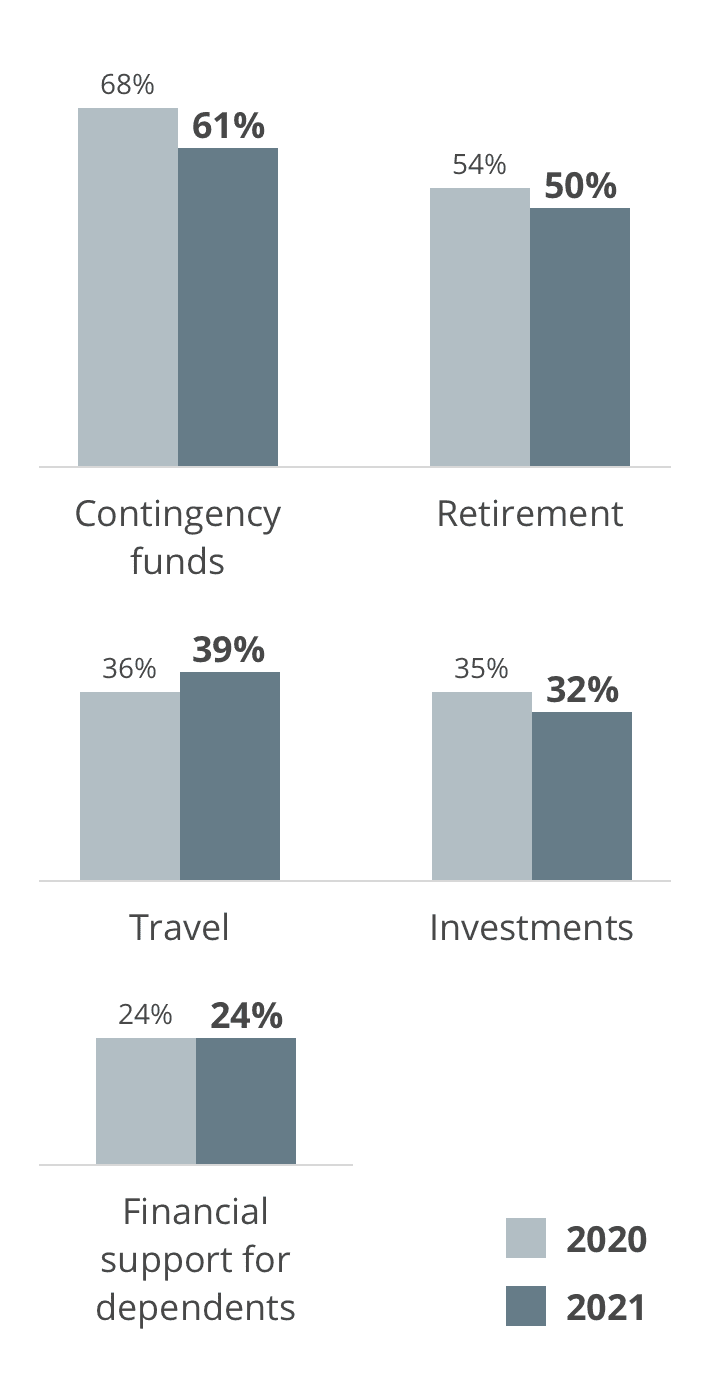

Singaporeans continue to be strong savers but are allocating more to pleasures and not their investments, retirement or contingencies.

91% of Singaporeans save at least 10% of their salary. Here’s a breakdown of what they’re saving for:

Just 53% have accumulated 6 months of current salary to overcome crisis.

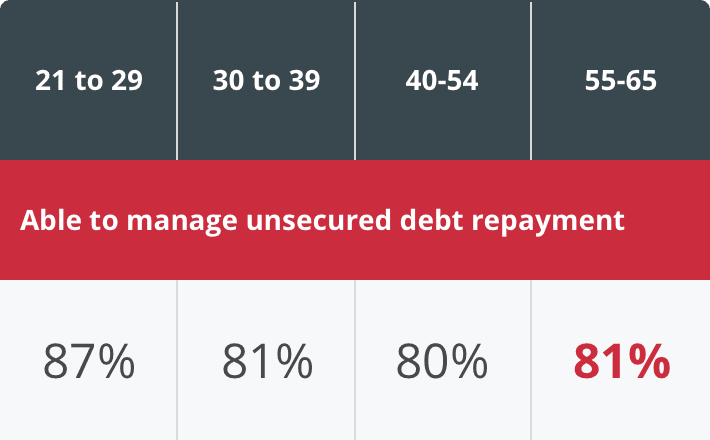

More Singaporeans across all age groups have poorer unsecured debt management.

This is especially so among older Singaporeans.

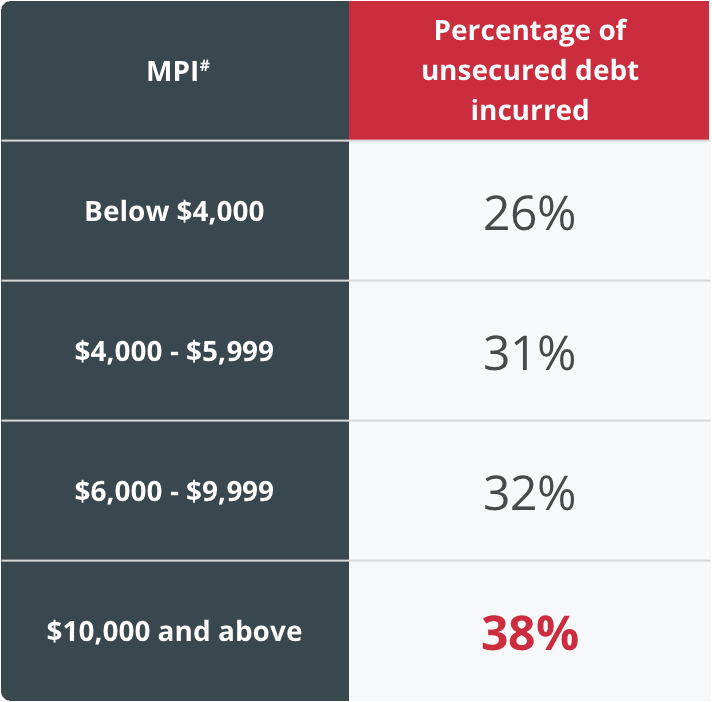

Notably, the more Singaporeans earned, the more unsecured debt they incurred.

#MPI stands for monthly personal income.

More Singaporeans are worried about not being able to pay off their personal loans.

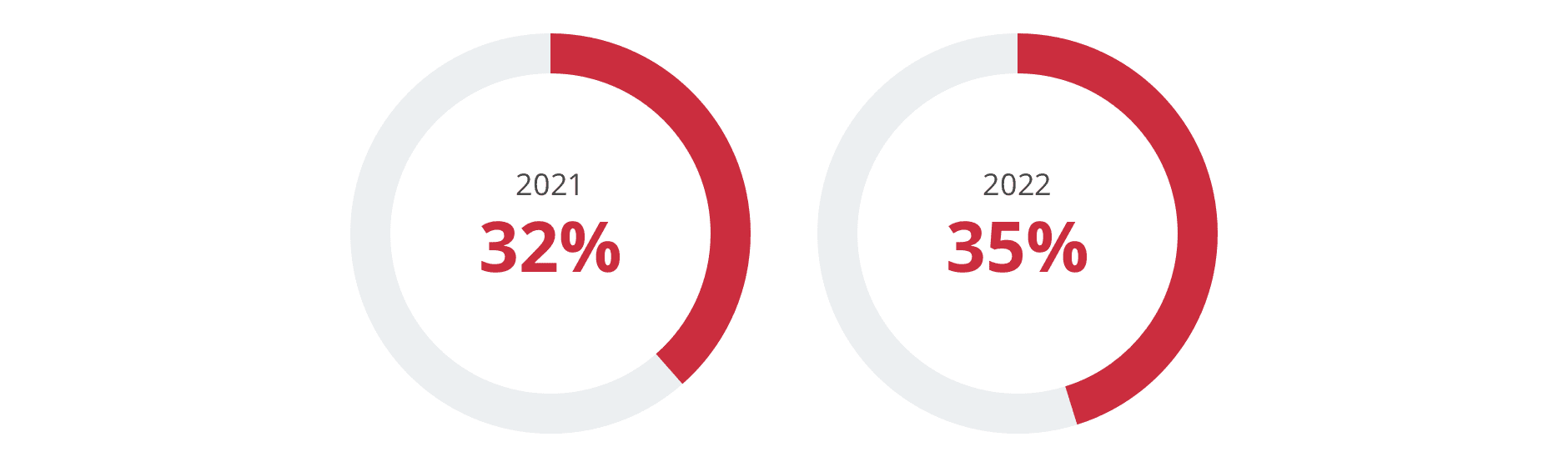

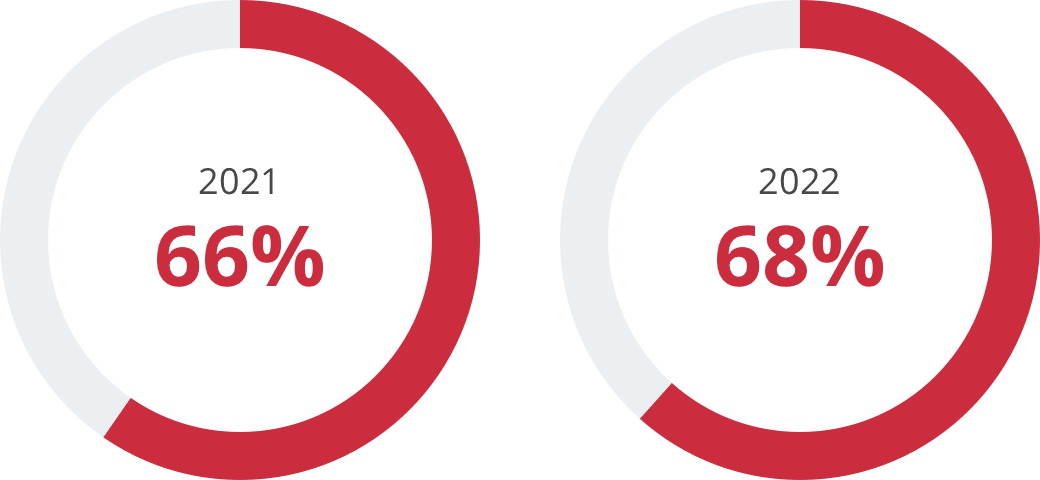

More Singaporeans across all age groups are also facing greater mortgage stress.

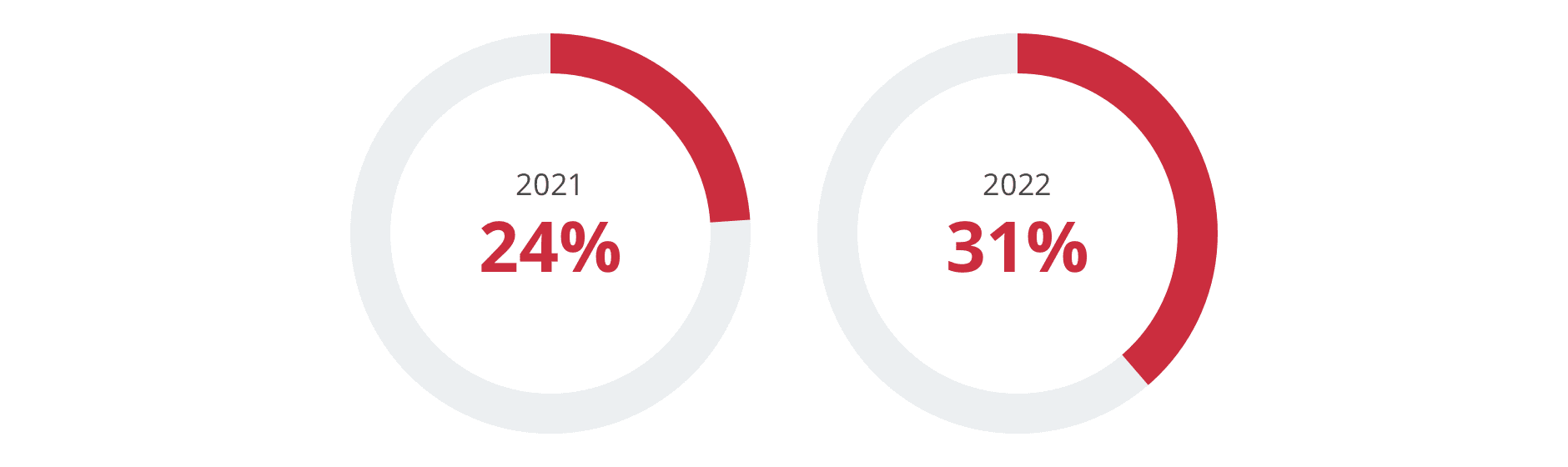

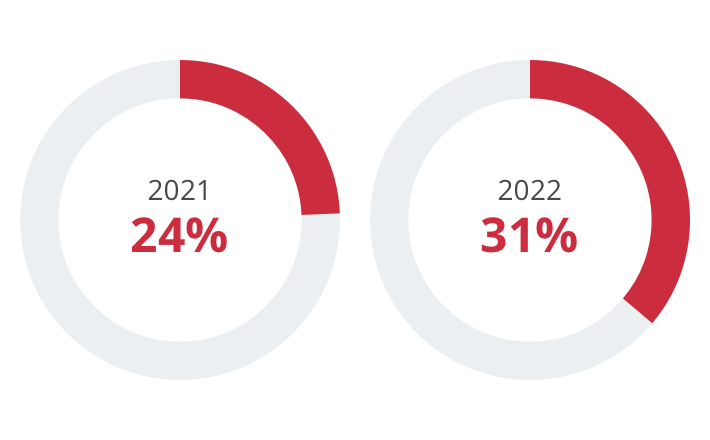

This year, 2 in 5 Singaporeans face some difficulties in paying off their mortgage loans, a 9-percentage point increase from 2021.

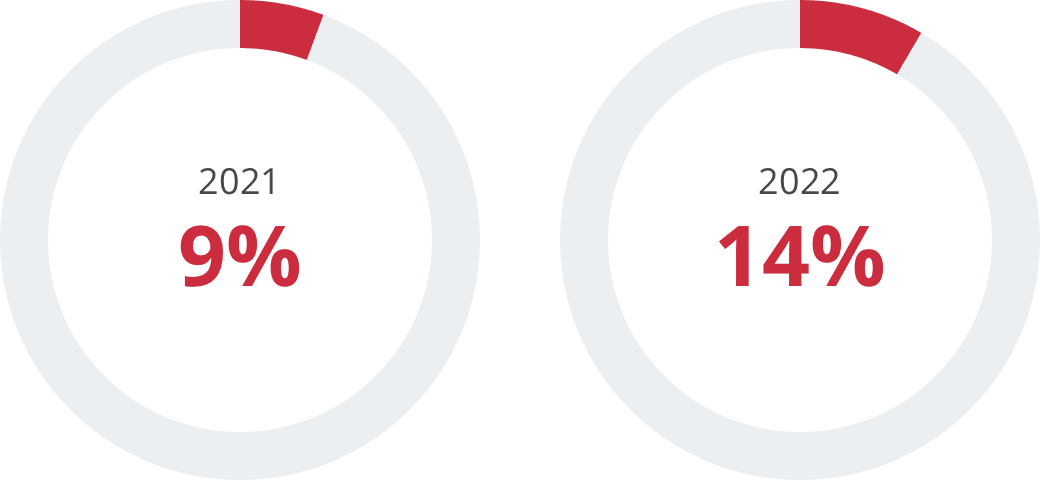

More Singaporeans are unable to pay off their loans on time

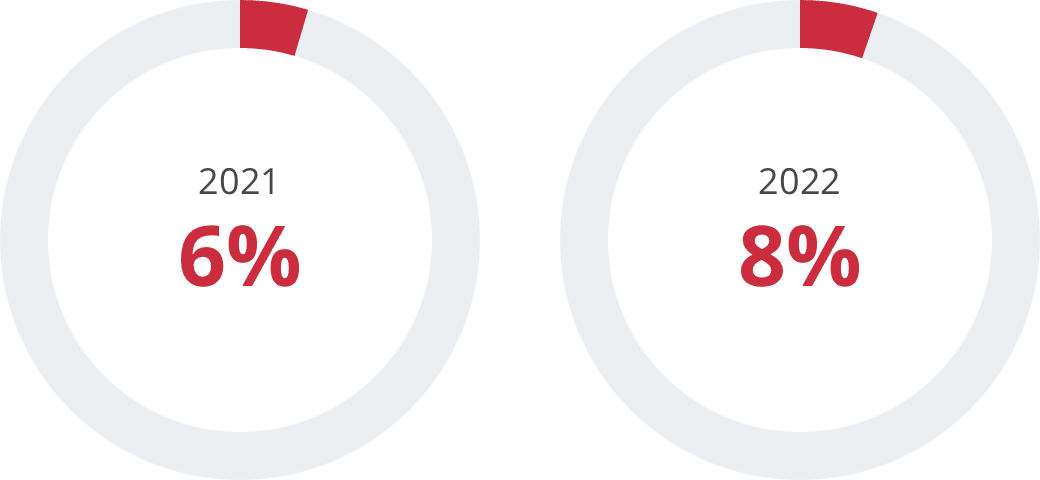

With more indicating they would have to sell or downgrade their homes to pay their loans

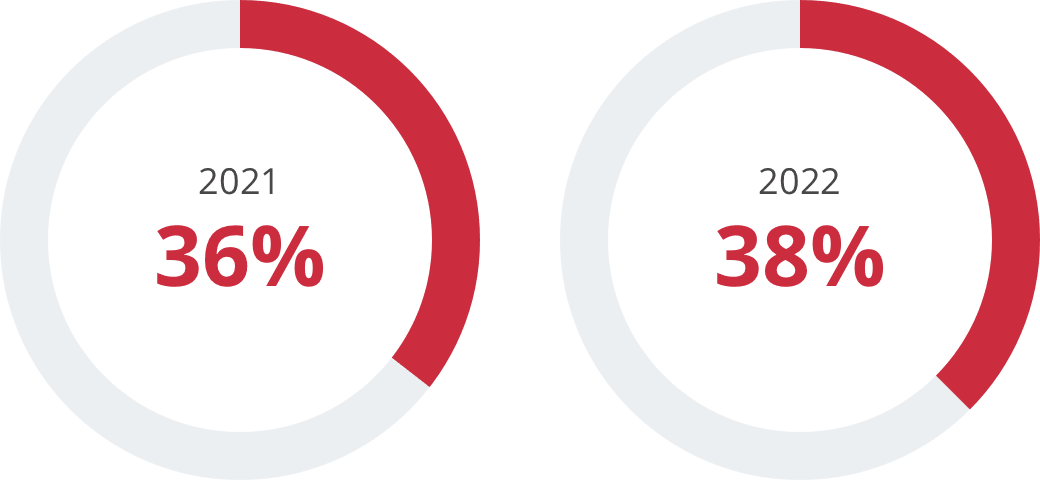

As such, more Singaporeans are worried about not being able to afford a home

More Singaporeans are planning for retirement.

Compared to 2021, there has been a 2% increase in Singaporeans that have retirement plans

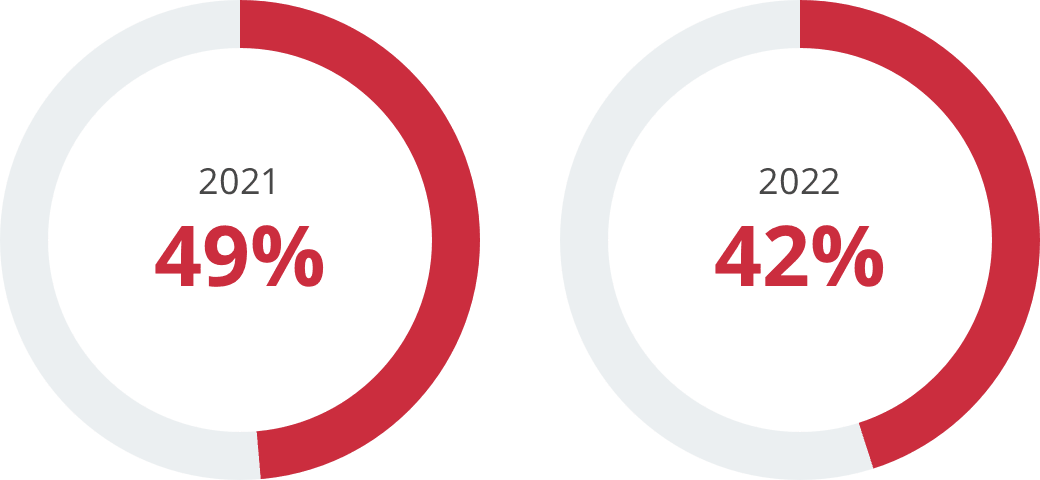

Yet, among those who have started making retirement plans, fewer are on track with achieving their goals this year.

Out of three retirement lifestyles that they could pick based on broad considerations, Singaporeans are choosing a more luxurious lifestyle despite high inflation. This year, 41% chose Retirement Lifestyle B—a 6 per cent increase from 2021.

While Singaporeans indicated that they are taking inflation into consideration, they are still underestimating the amount needed for their chosen retirement lifestyle.

- Retirement Lifestyle A

- Retirement Lifestyle B

- Retirement Lifestyle C

| Retirement Lifestyle A | Retirement Lifestyle B | Retirement Lifestyle C |

|---|---|---|

|

|

|

|

Singaporean’s estimated cost of chosen lifestyle: $1,916 |

Singaporean’s estimated cost of chosen lifestyle: $2,372 |

Singaporean’s estimated cost of chosen lifestyle: $3,617 |

|

Actual cost of chosen lifestyle: $2,550 |

Actual cost of chosen lifestyle: $3,210 |

Actual cost of chosen lifestyle: $5,760 |

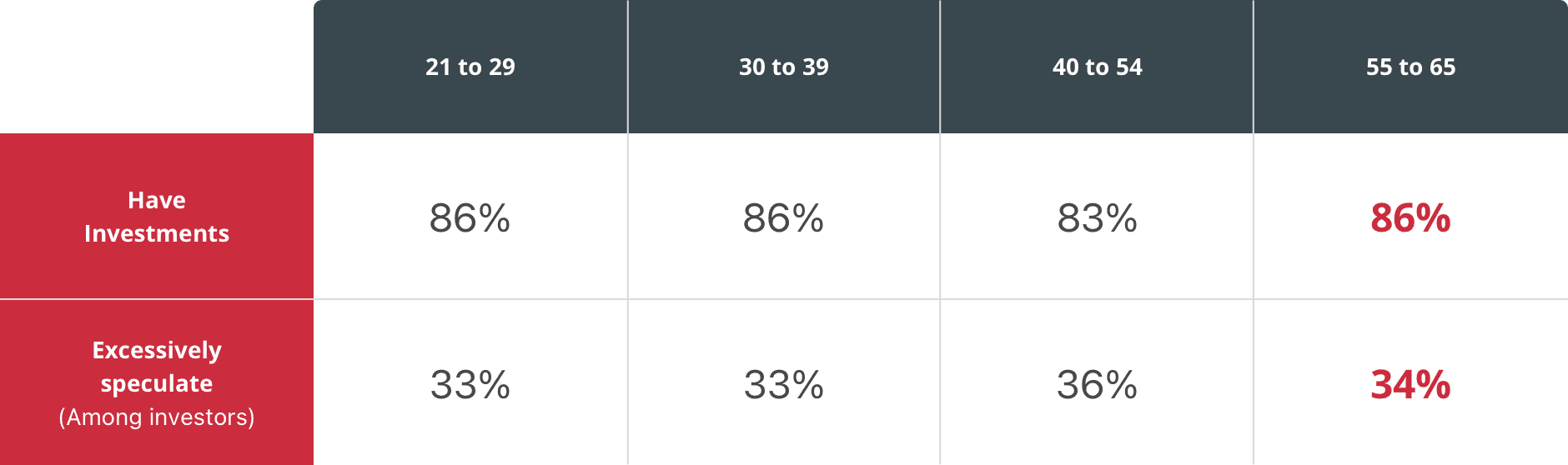

More seniors are speculating excessively in order to quickly close the gap to their retirement.

In fact, the top reason why they are investing is to build retirement funds.

Young Singaporeans (Gen Zs and millennials) are eager to retire more than a decade before Singapore’s official re-employment age of 68.

Although many have just started working, they desire to retire at an earlier age than other age groups.

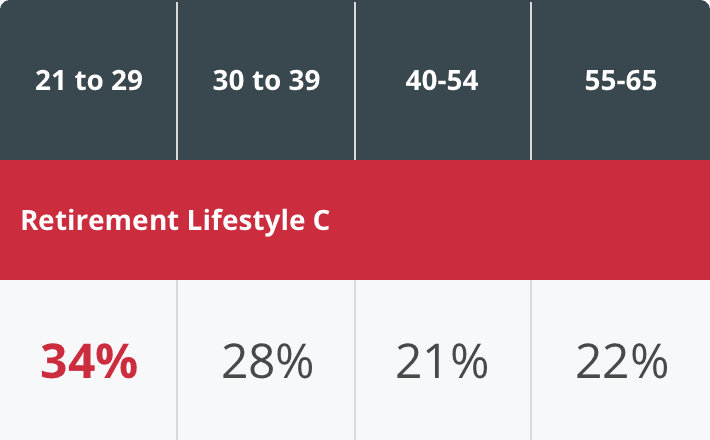

And they wish to do this in style. More young Singaporeans in their 20s chose the most luxurious lifestyle (Retirement Lifestyle C) than other age groups.

Yet they worry that they cannot meet their goals. Two-thirds of young Singaporeans worry that they do not have enough funds to retire well.

As such, they have turned to side incomes to build their wealth.

More young Singaporeans have a source of side income as compared to other age groups.

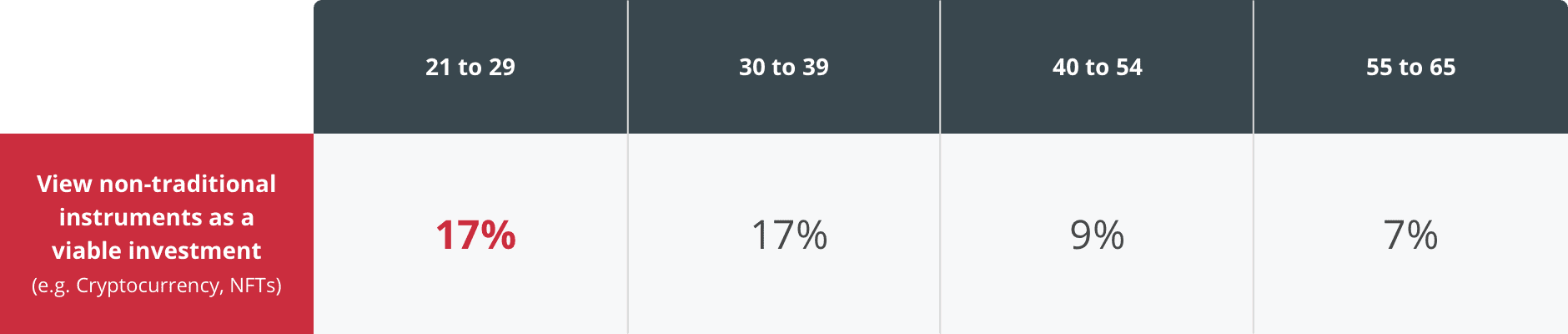

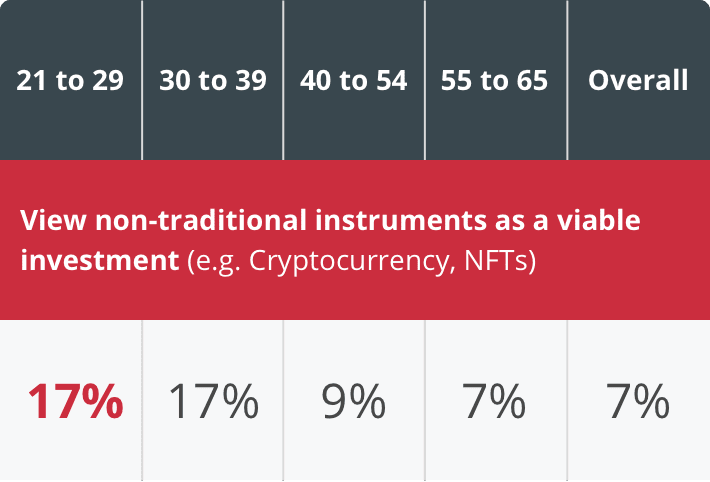

And more of them are investing in riskier products.

Despite crypto’s slump in 2022, 39% of crypto owners in their 20s are likely to invest more in the next 12 months.

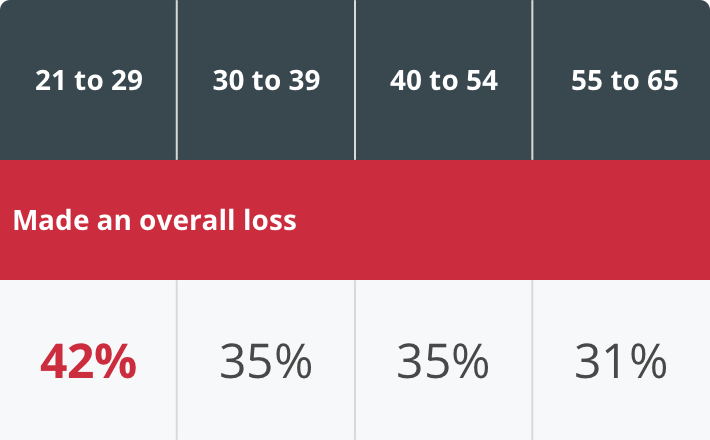

This year’s market downturn hit young Singaporeans in their 20s the hardest, with 42% making an overall loss in their investment portfolios.

This group also had the lowest rate of return on investments compared to other segments.

Read the OCBC Financial Index 2022 media release.

Discover how your peers are faring.

I am