Export Letter of Credit — How this versatile tool can help SME exporters

Export Letter of Credit — How this versatile tool can help SME exporters

Exporters face a common dilemma. Ideally, they would prefer the importer to pay upfront for an export shipment to avoid the risk of non-payment. On the other hand, if the importer pays upfront, the exporter might not ship the goods after receiving payment.

If the exporter and their customer are very familiar with each other, bridging this “trust gap” is less of a problem. They may trust each other enough to conduct business on an “open account” or “cash in advance” basis. But what if that is not the case?

This is where the trade finance instrument known as a Letter of Credit (LC) comes into play. It is a document issued by the importer’s bank (or LC issuing bank) to the exporter, to confirm that they will be paid by the bank once certain conditions are met.

In other words, the importer no longer needs to rely on trust to know whether the exporter will ship the goods. Instead, the LC issuing bank provides assurance to the exporter that the LC payment obligations will be fulfilled, once the bank receives proof that the exporter has shipped the goods and fulfilled the stated conditions in it.

This makes Export LCs a crucial instrument for an SME exporter – they help to eliminate the fear and uncertainty of global trade, reconciling the divergent needs of an importer and exporter.

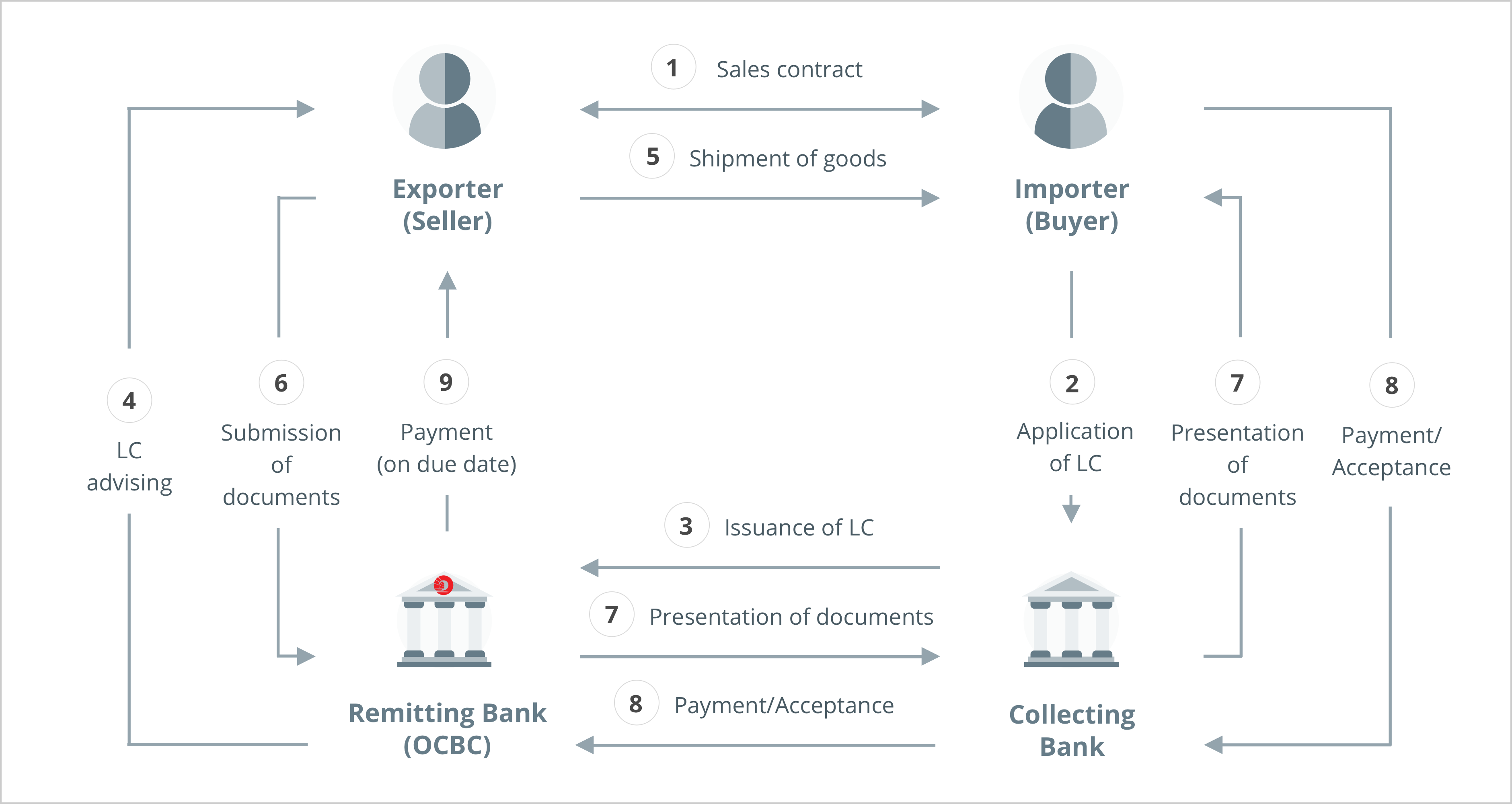

How Export LCs fit into the export-import process

Export LCs can be understood in nine broad steps, from the exporter’s perspective.

- Sales contract: You (the exporter) negotiate the terms of the deal, from goods to payment. This includes the use of LC as the payment method.

- Application of LC: Once both parties have signed the sales and purchase agreement, the importer will then have to apply for a letter of credit from their bank (i.e. LC issuing bank).

- Issuance of LC: The importer’s bank issues the LC to your advising bank, in this case OCBC.

- Advising: OCBC will then confirm that it is authentic, before forwarding a copy of the LC to you.

- Shipment of goods: After receiving the Export LC, you can arrange for the shipment and obtain the necessary documents asked for in the LC. You should also obtain documentary proof that you have shipped the goods. This will typically be in the form of a Bill of Lading from the carrier.

- Submission of documents: Now, all you have to do is fill up the application form and present it along with the necessary documents asked for in the LC to OCBC, who will then check your documents (upon your request) to ensure its compliance with the LC terms and conditions. OCBC may also request for you to address any documentary discrepancies, should they arise.

- Presentation and acceptance of documents: Once any discrepancies have been settled, the documents will be sent to the LC issuing bank, where they are presented to the issuing bank and the importer for acceptance.

- Settlement of payment from the importer and possession of goods: The issuing bank verifies the documents and obtains payment from the importer, before transmitting payment to OCBC. The documents will then be used by the importer to obtain possession of goods.

- Settlement of payment to the exporter: OCBC will release payment to you.

3 ways Export LCs can benefit exporters

LCs help importers ensure timely possession of goods, which is vital for many complex businesses. It also allows them to confidently trade with new exporters from around the world, thus growing their business globally.

But what about exporters – what tangible benefits do they receive? Here are the three main ones.

1. Eliminate risk of buyer defaulting:

All LCs are irrevocable, meaning their terms cannot be altered without the consent of all parties involved – including you as the exporter. Once your importer’s bank has issued the LC, your risk is greatly reduced. As long as you have received a clean and acceptable LC and presented the appropriate documentary evidence that you have shipped the goods in line with the LC requirements, the importer’s bank must honour the payment obligations.

2. Better control over cash flow and working capital:

Most exporters are all-too-familiar with payment delays from importers, and the hassle they bring. They can disrupt your cash flow and working capital management, and potentially even cause you to have to delay your own payments to suppliers.

When using Export LCs, the payment terms are already predefined, and the payment obligation falls to the importer’s bank. This gives you greater assurance as to when you will receive the payment, enabling you to better manage your cash flow. Furthermore, removing the risk of payment delays also allows you to plan your working capital levels better, especially for big sales.

3. Allows you to expand your business safely:

As Export LCs can give you higher assurance in receiving payment for your goods, you can also have the confidence to forge new relationships and expand your business.

Key risks to consider when using Export LCs

Although Export LCs are an essential trade financing instrument for exporters, there are some things you should still watch out for.

The first important thing to understand is that LCs are almost solely document-based – the banks are only concerned with the documents, not the underlying goods. Any discrepancies in the documents could lead to payment delays or even non-payment in a worst-case scenario. This is why the validation and checking stage (as shown in step 6 above) is so important. A competent bank is crucial as it can help you identify any documentary discrepancies early on.

Secondly, a survey or inspection certificate issued by a reputable third party may be deemed prudent to avoid any commercial disputes (e.g. goods of substandard quality from what was indicated in the documents) between the importer and exporter.

Thirdly, LCs allow you to transfer the risk of default or non-payment from your importer to their bank. However, bear in mind that you will be taking on the risk of the LC issuing bank and country. This is crucial to keep in consideration as well.

It is important not to skip due diligence on the importer. Although export LCs transfer the risk of default or non-payment from the importer to their bank, you are still exposed to the risk of potential fraud. Always do proper due diligence on the importer – LC or not.

3 simple tips for exporters when using LCs

As much as Export LCs are a powerful instrument for managing risk and facilitating international trade, there are other considerations. As such, here are three best practices that exporters should follow when using LCs.

1. Pay extra care when negotiating the LC’s terms and conditions:

As payment from the importer’s bank is all stated in the documents, it is crucial to ensure you can meet all the LC’s terms and conditions. During the negotiation process, make certain you can fulfil each term before agreeing to add it to the LC.

2. Request a preview of the LC application:

As the saying goes, trust but verify. Before the importer submits their LC application to their bank, ask for a preview. Then, double check to see that everything is aligned with what you have previously agreed upon. Doing this will also help you spot any unintentional errors on the importer’s part and save you both a lot of hassle amending the LC later on.

3. Carefully check documents for consistency before submission:

Never blindly submit documents to your negotiating bank before checking them. Even a small documentary error could risk expensive payment delays. The last thing you want is to hear that the importer’s bank is unable to remit the payment because of some discrepancy in the documents, after you have already shipped the goods.

Let OCBC help you confidently export your goods and expand your business

Today’s business playing field is a global one, and opportunities can be found in every corner of the world. To navigate this landscape, you need a trusted trade financing partner by your side. OCBC is that partner for thousands of businesses – whether it is processing their incoming LCs or providing invoice financing or bank guarantees.

Disclaimer

You may be directed to third party websites. OCBC Bank shall not be liable for any loss suffered or incurred by any party for accessing such third party websites or in relation to any product and/or service provided by any provider under such third party websites.

The information provided herein is intended for general circulation and/or discussion purposes only. Before making any decision, please seek independent advice from professional advisors. No representation or warranty whatsoever in respect of any information provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake any obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same.

Discover other articles about: