Global Outlook

March 2025

Rising uncertainty

President Donald Trump’s second term is increasing volatility in financial markets. We think the outlook still favours US assets. The US economy is likely to experience a soft landing as inflation eases. The Federal Reserve may be able to cut interest rates again this year, and US corporates should benefit from sweeping deregulation and fresh tax cuts. But the US outlook is being clouded by the new government’s twists and turns.

The threat of fresh, widescale tariffs may hurt business sentiment, weaken consumer confidence and raise inflation expectations. At the same time, business sentiment may be dented if the Trump administration’s crackdowns on immigration tighten the US labour market, while attempts to downsize the federal government may hurt consumer confidence.

Investors should thus expect financial markets to stay volatile. Despite the uncertainty, we think investors should still favour equities. The prospects of tax cuts and deregulation in the US, further stimulus in China and greater spending on defence in Europe should benefit risk assets.

US – Stagflation fears cloud favourable outlook

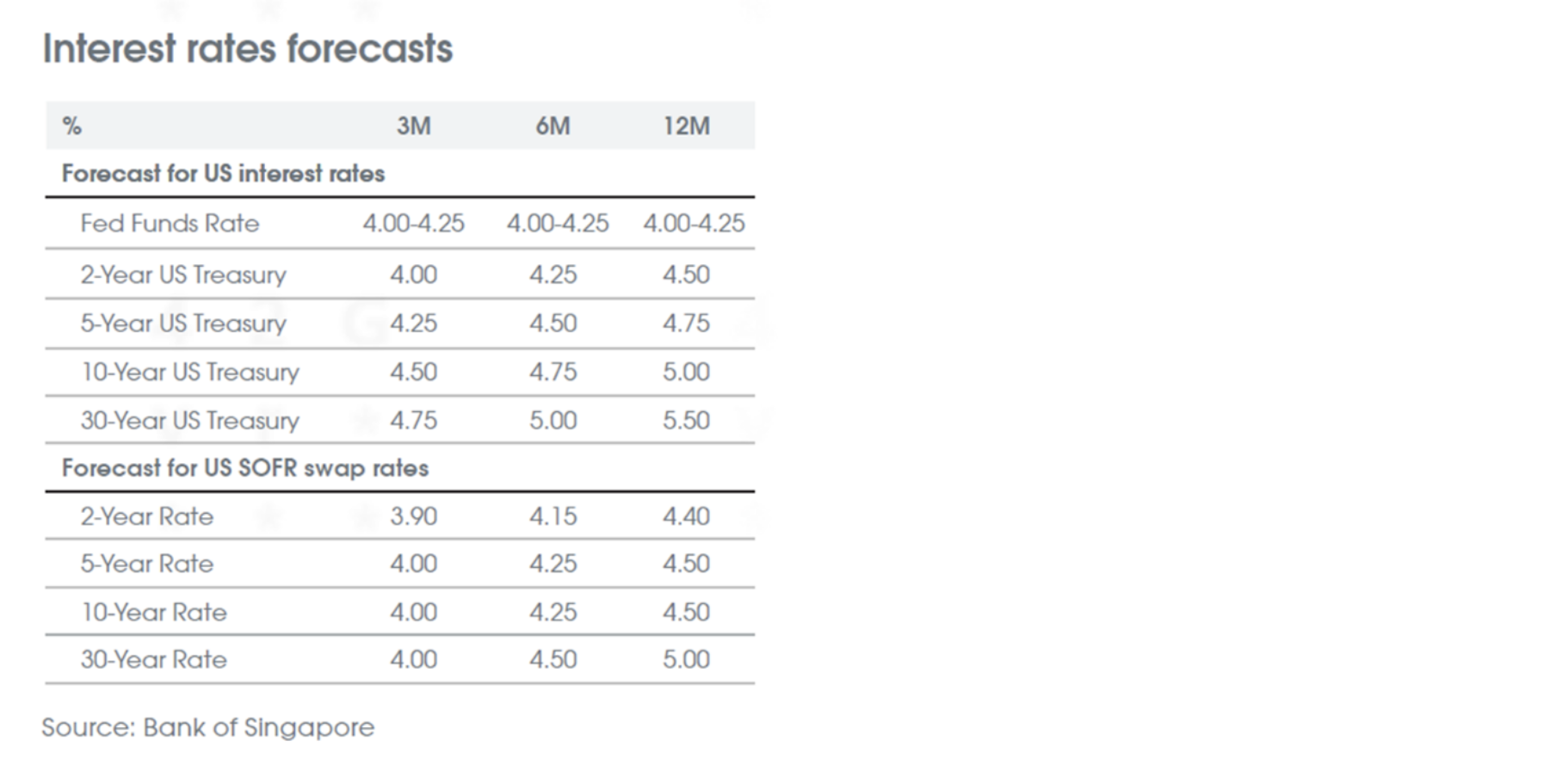

Financial markets have weakened after their strong start to 2025 with the S&P 500 Index falling from highs of 6,147 and 10Y UST yields down from 4.80% on fears that the Trump administration’s policies would hurt rather than help growth.

Deregulation and tax cuts should support activity. But President Trump’s tariff threats are creating uncertainty for firms and consumers. Tighter immigration may hurt the supply of labour, and the Department of Government Efficiency’s harsh cuts is likely to make federal government employees fearful for their jobs.

The latest data shows the downside risks to growth and upside risks to inflation from the White House’s policies.

US retail sales fell 0.9% in January despite excess savings accumulated during the pandemic remaining considerable. Meanwhile, the long-term 5Y-10Y inflation expectations hit 3.5% in February, their highest level this century according to the University of Michigan’s survey. In addition, US consumer confidence had its largest monthly fall in three years in February and weekly jobless claims rose sharply, increasing fears that federal government job cuts will raise unemployment.

We think it is too early, however, to say the favourable outlook for US markets has faltered. January’s retail sales were hit by bad weather in the US at the start of the year. February’s rise in jobless claims may only be seasonal and while the Atlanta Fed’s widely followed US GDP growth tracker currently forecasts the economy contracting in 1Q25, the model is likely to be distorted by this year’s surge in gold imports to beat US tariffs - boosting the US trade deficit and thus hurting GDP growth. In contrast, the New York Fed’s Weekly Economic Index shows growth is still firm above 2%.

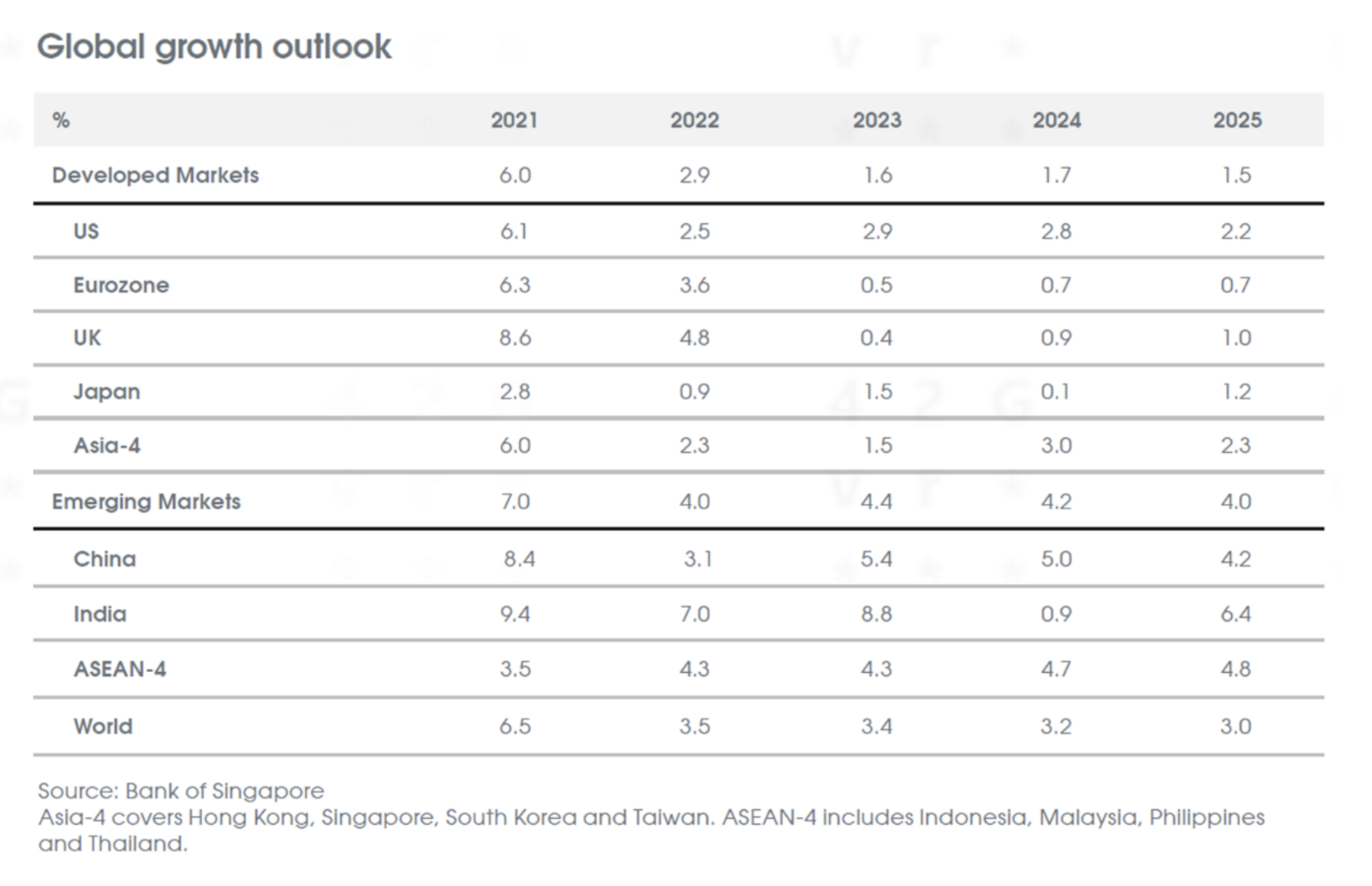

We thus think the US outlook of solid growth, easing inflation and potentially one further 25 basis points interest rate cut by the US Federal Reserve remains favourable for risk assets. But given all the uncertainty created by the Trump administration, we will continue to watch upcoming data closely to see if the US economy is at risk from unexpectedly suffering stagflation.

China – US tariffs the key risk this year

China’s economy recorded a firmer end to 2024. In 4Q24, China’s GDP beat forecasts, as sudden stimulus measures announced last year to support the economy, and the frontloading of exports to beat US tariffs this year, spurred activity.

China’s wide-ranging stimulus measures initiated from last September, including interest rate cuts, have begun to aid growth and ease fears of deflation. Inflation remains very low at just 0.5% in January, but the 10Y government bond yields have begun to rebound from their record lows of 1.60% seen at the start of this year.

Further stimulus, however, is needed to keep China’s recovery from faltering again. Though GDP growth in 2024 hit China’s 5% target, consumers remain scarred by the pandemic and property markets remain fragile. At the same time, the new US government imposed an additional 20% tariffs on Chinese exports.

At the start of China’s National People’s Congress (NPC) in early March, more fiscal stimulus was unveiled with the government promising greater efforts to support consumption and cushion the impact of an escalating trade war with the US on an economy that Beijing is determined to grow by another 5%-or-so this year.

The roughly 5% growth target for 2025 and a larger budget deficit plan of around 4% of GDP (3% previously) was an indication of the government’s commitment to try and boost growth.

The government said that it plans to issue 1.3 trillion yuan in ultra-long special treasury bonds this year, up from 1 trillion yuan in 2024. Local governments will also be allowed to issue 4.4 trillion yuan in special debt, up from 3.9 trillion yuan. The higher debt and spending figures aim to cushion the economy from the impact of US tariffs.

Europe –Three challenges for Europe’s economic outlook

Europe’s financial markets have been buoyed this year by hopes for a truce between Ukraine and Russia, and for more fiscal stimulus from Berlin after Germany’s elections. But the sudden tilt towards Russia by the Trump administration, the likely end of decades-long US commitments for Europe’s security and the threat of sweeping US tariffs are set to keep testing the Eurozone and the UK.

The first challenge for European countries is to ensure Ukraine’s security - and by extension the region’s; if Kyiv and Moscow agree to a long-term ceasefire or if Washington tries to impose a settlement on Ukraine.

The second challenge will be how quickly Germany can increase spending on defence and repairing fraying infrastructure after February’s elections were won by the centre-right CDU/CSU.

The last challenge is President Trump’s threat to impose 25% tariffs on Europe’s exports including cars. We estimate steep US levies would cut Eurozone growth by a full percentage point, offsetting any peace dividend from a Ukraine-Russian truce or looser fiscal policy in Germany.

Given Europe’s three key challenges, we think the outlook will remain testing this year. We thus keep our forecast for subdued GDP growth of 0.7% in 2025 and expect the European Central Bank (ECB) to keep cutting interest rates from 2.50% currently to 1.50% to support the economy.

Japan – Further interest rate rises set to help the Yen

The Bank of Japan (BOJ) has now raised interest rates three times over the past year from -0.10% to 0.50% as core inflation (after the shocks of the pandemic and the Ukraine and Gaza wars), has been above its 2% target since 2022.

We think inflation will still exceed 2% this year leading to two more 25 basis points rate hikes to 1% in 2025. We thus expect tighter BOJ policy to help the Yen keep recovering through 150 against the US Dollar.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

The information provided herein may contain projections or other forward looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. Investments are subject to investment risks, including the possible loss of the principal amount invested.

The Bank, its related companies, their respective directors and/or employees (collectively “Related Persons”) may or might have in the future interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. The Bank and its Related Persons may also be related to, and receive fees from, providers of such investment products.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent. The contents are a summary of the investment ideas and recommendations set out in Bank of Singapore and OCBC Bank reports. Please refer to the respective research report for the interest that the entity might have in the investment products and/or issuers of the securities.

Investments are subject to investment risks, including the possible loss of the principal amount invested. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

This document may be translated into the Chinese language. If there is any difference between the English and Chinese versions, the English version will apply.

Cross-Border Marketing Disclaimers

OCBC Bank's cross border marketing disclaimers relevant for your country of residence.

Any opinions or views of third parties expressed in this document are those of the third parties identified, and do not represent views of Oversea-Chinese Banking Corporation Limited (“OCBC Bank”, “us”, “we” or “our”).