Proyeksi Global

April 2025

Trade shock

President Trump shocked financial markets by imposing a 10% baseline tax on all US imports and steep additional reciprocal tariffs.

Investors had expected across-the-board US tariff hikes of around 10%, but the reciprocal tariffs were much worse than feared. US tariffs on Chinese exports are set to rise by a further 34% on top of the 20% extra tariffs imposed earlier in 2025. European Union (EU) exports will face 20% tariffs and Japanese goods a 24% tax. We see four key implications here for the economic outlook.

First, if the new US tariffs remain throughout 2025 and foreign countries retaliate as China already has, then a recession will ensue. But we think tough negotiations are likely over the next few months to roll back the US reciprocal tariffs while its universal 10% tariffs remain. We thus expect two quarters of stagflation – weak growth and higher inflation – rather than the worst-case scenario of a recession.

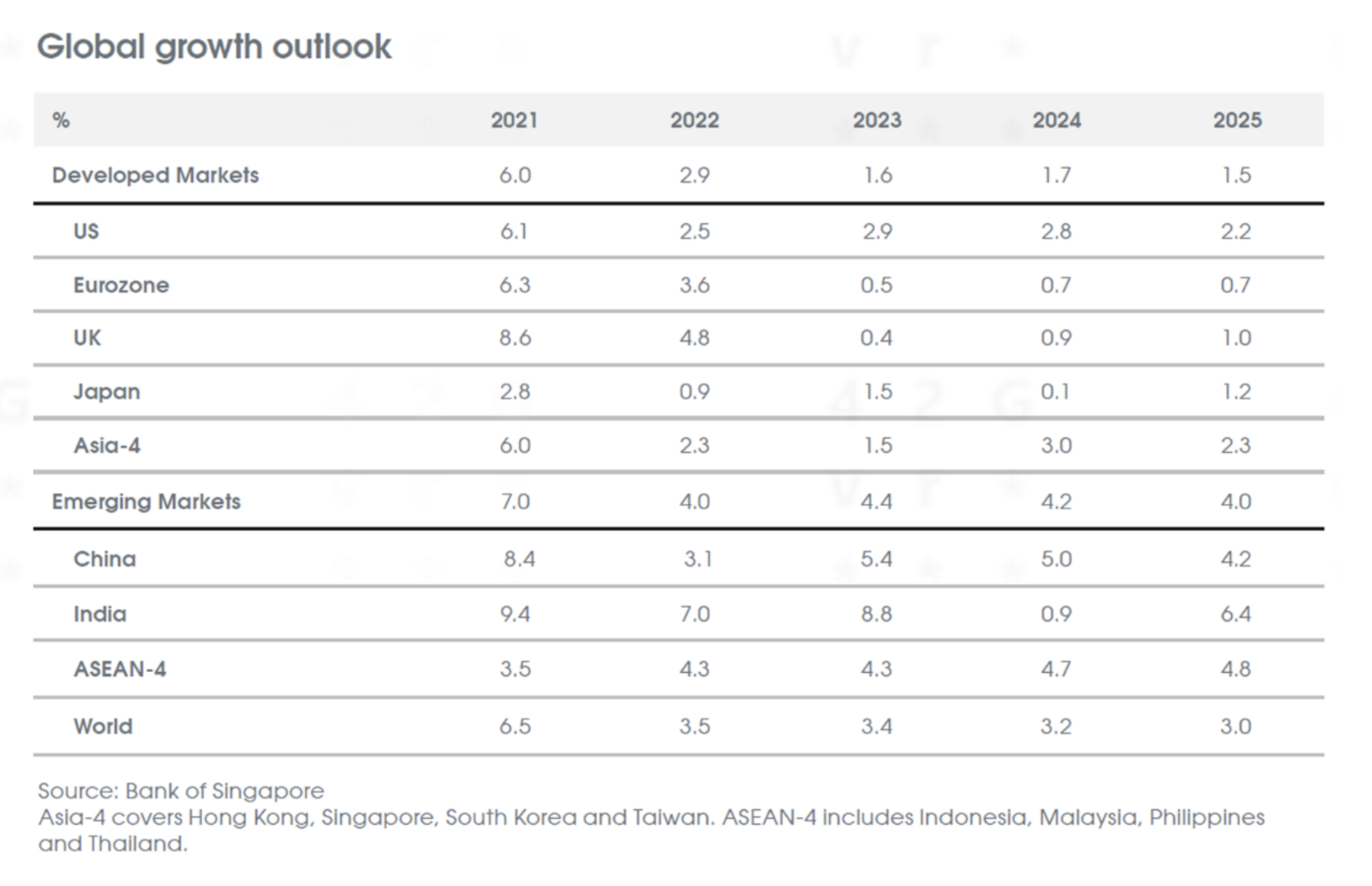

We have downgraded our US outlook from a soft landing of 2.2% growth in 2025 to a sluggish 1.5% rate as uncertainty over tariffs has already caused 1Q25 US growth to be near 0% and 2Q25 growth is likely to be flat too. We also see two quarters of little or no expansion in the Eurozone, UK and Japan, keeping 2025 growth weak below 1.0%. In contrast, we still forecast 4.2% growth for China as we had expected 20-30% US tariff rises and we see scope for further fiscal stimulus from Beijing.

Second, US tariffs will push inflation up globally as import costs rise.

Third, central banks will face a tough choice between curbing inflation and supporting growth.

Last, safe havens will stay in demand over the next few months until a truce in the trade wars is reached but the long-term outlook for US Treasuries (USTs) remains challenging as inflation rises and the US fiscal deficit worsens further.

US – Fed is not coming to the rescue

The shock to global trade from President Trump’s tariff hikes is set to weaken US growth sharply while lifting inflation.

In the worst case of US tariffs staying throughout 2025, we expect the US and global economies to fall into a recession. But even in our base case of negotiations leading to a trade war truce over the next few months, growth will still likely be flat or very weak for the next two quarters.

At the same time, inflation is set to increase as tariffs drive up import costs. We expect core inflation will now end 2025 higher in a 3-4% range. The Fed and other central banks will thus have to set interest rates while facing stagflation this year.

In his latest speech on 4 April, Fed Chairman Powell emphasised how uncertain the outlook had become after the US tariff announcements. He warned inflation may not be transitory and officials would need to wait for more clarity first before considering changing interest rates.

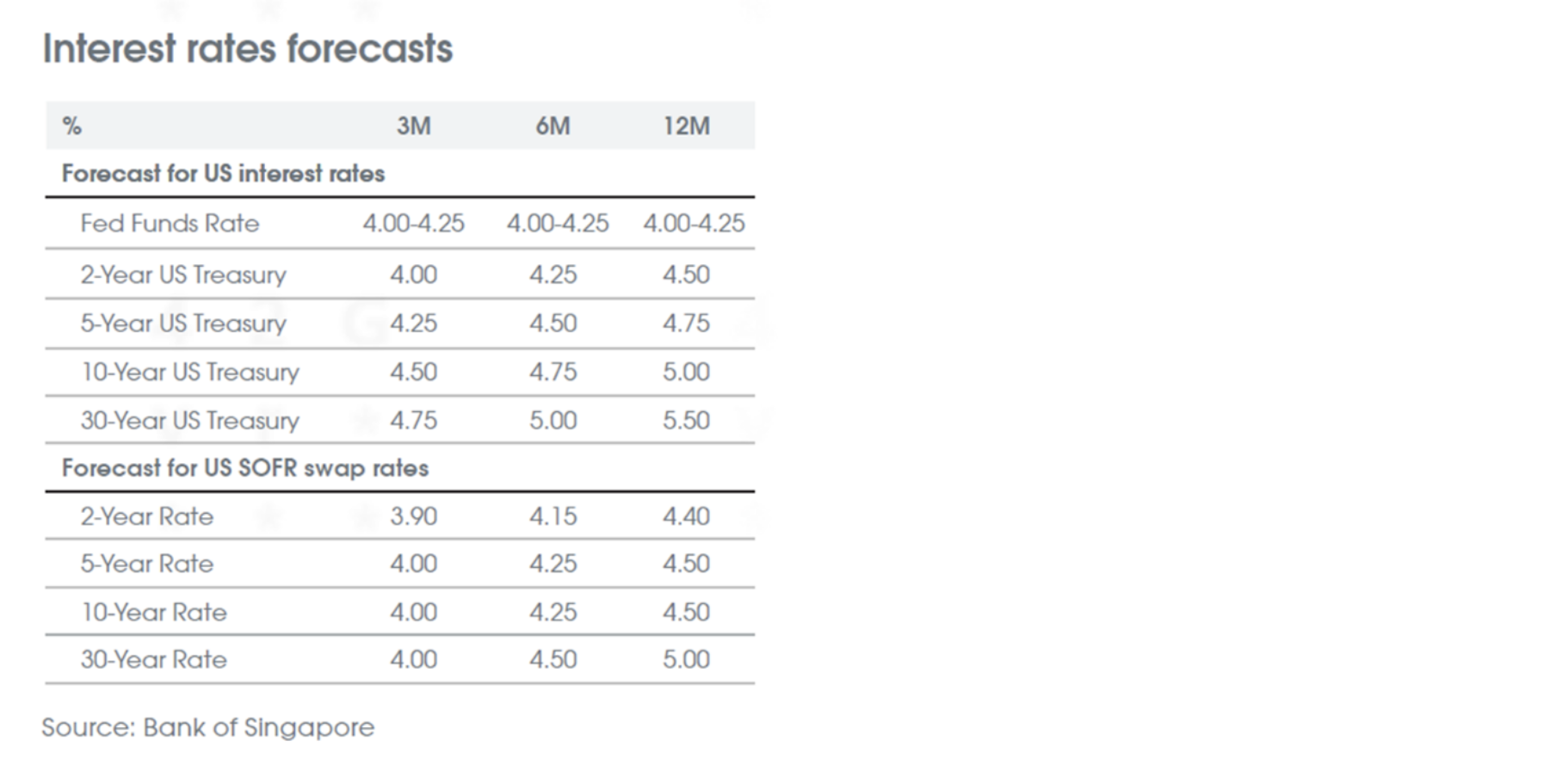

We thus expect the Fed will continue holding its fed funds rate at 4.25-4.50% while assessing if the US will suffer stagflation and thus need interest rates to stay elevated to curb inflation or whether a recession will require several interest rate cuts this year instead.

With core inflation still above its 2% target at 2.8% and likely to end 2025 well over 3%, we think the Fed may only cut interest rates once this year unless the unemployment rate starts to rise sharply from its current low level of 4.2%.

In contrast, financial markets are pricing in a US recession and four Fed rate cuts in 2025. US Treasury (UST) yields have plunged with 10Y UST yields down from 4.80% earlier this year to below 3.90% at one stage in April. We expect 10Y UST yields may stay low, close to 4.00%, in the near term given uncertainty about growth prospects now. But any trade truce over the next few months will cause yields to rebound given the risks of higher inflation and rising US fiscal deficits. We thus keep our forecast of 10Y UST yields reaching 5.00% over the next 12 months.

China – Beijing retaliates against Washington’s tariffs

The US government has sharply increased tariffs on Chinese exports this year, causing Beijing to retaliate. First, the Trump administration imposed two rounds of 10% tariffs on all Chinese goods. Then, Washington imposed further rounds of tariff hikes, raising the total tariff rate to 125% on Chinese exports.

In response, China has imposed an 84% tariff on US goods while also tightening up exports. Thus, the trade war between the world’s two largest economies has escalated sharply.

In contrast to most other major economies, however, we have kept our 2025 GDP forecasts unchanged for China. We still expect growth to slow from 5.0% last year to 4.2% this year as we had assumed the US would impose large tariff hikes on Chinese exports when President Trump won his re-election in November last year.

We also expect that Beijing’s ability to retaliate against US firms operating in China for its vast domestic market will make it more likely both sides will come to a truce over the next few months. Last, we see scope for Beijing to provide fresh fiscal stimulus to support growth. We therefore keep our view that China’s economy will slow down significantly this year but not suffer a major crisis because of steeply higher US tariffs. We also expect Beijing to keep tightly managing the CNY rather than devaluing the currency.

Europe – The EU is set to retaliate, the UK will decline

The EU is poised to retaliate after the US imposed a 10% baseline tariff on all imports and an additional 20% tariff on EU exports. We expect that the EU is likely to impose equivalent tariffs to force the US administration to negotiate a truce in its trade war over the next few months.

In contrast, the UK has signalled it will not retaliate after Britain’s exports were “only” hit with new 10% baseline tariffs. Both the Eurozone and the UK, however, are likely to see growth weaken from the shock to global trade. We forecast the GDP in each of Europe’s two major economies will stagnate, with growth staying below 1.0% this year.

In response to weaker growth, we expect the European Central Bank (ECB) will keep cutting interest rates from 2.50% to 1.75% over its next three meetings during the summer. We also see the Bank of England (BoE) making three rate cuts from 4.50% to 3.75% this year as it continues to reduce interest rates once a quarter.

Despite weaker growth and lower interest rates, however, we expect both the Euro and Pound to keep strengthening against the US Dollar to 1.17 and 1.38 respectively now as global investors turn to Europe as an alternative to the US in the wake of Washington’s volatile policies.

Japan – The Bank of Japan (BoJ) will likely pause its interest rate hikes

Despite being one of US’s closest allies, Japan’s exports will face a 24% US tariff pending a 90-day negotiation period. We expect Tokyo will seek to make a deal with Washington, but the trade shock will still hurt Japan’s growth. We now forecast its GDP will expand by less than 1.0% in 2025. We also see the BOJ pausing its rate hikes at 0.50% given the uncertain global outlook. But we expect the Yen to keep rebounding as Japanese investors become more reluctant to go abroad. We now forecast the Yen to rise to 139 against the US Dollar as the greenback weakens globally.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

The information provided herein may contain projections or other forward looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. Investments are subject to investment risks, including the possible loss of the principal amount invested.

The Bank, its related companies, their respective directors and/or employees (collectively “Related Persons”) may or might have in the future interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. The Bank and its Related Persons may also be related to, and receive fees from, providers of such investment products.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent. The contents are a summary of the investment ideas and recommendations set out in Bank of Singapore and OCBC Bank reports. Please refer to the respective research report for the interest that the entity might have in the investment products and/or issuers of the securities.

Investments are subject to investment risks, including the possible loss of the principal amount invested. The information provided herein may contain projections or other forward-looking statements regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures, predictions or projections are not necessarily indicative of future or likely performance.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

This document may be translated into the Chinese language. If there is any difference between the English and Chinese versions, the English version will apply.

Cross-Border Marketing Disclaimers

OCBC Bank's cross border marketing disclaimers relevant for your country of residence.

Any opinions or views of third parties expressed in this document are those of the third parties identified, and do not represent views of Oversea-Chinese Banking Corporation Limited (“OCBC Bank”, “us”, “we” or “our”).