Top Fund

November 2020

Top Fund Ideas For Q4 2020

Amundi-OCBC Momentum Fund

Don’t miss the forest for the trees

Suitable for:

The current investment climate is likely characterised by (1) a moderate and drawn out economic recovery that returns to pre-Covid-19 levels of production and employment after 2021; (2) potential upside of a widely distributed vaccine within these two years; (3) moderately rising inflation; (4) marginally higher US treasury yields; (5) a weaker US Dollar; and (6) US Fed funds rates staying at near-zero levels for up to 5 years.

The steady, albeit long drawn, recovery in the global economy is the foundation for a broad-based and sustainable rebound in risk assets over the long run. However, the journey higher is seldom smooth in view of heightened uncertainty and various risk events on the horizon including the US presidential elections and Brexit.

Investors may be tempted to hold on to cash as they duck for cover, but with interest rates at crisis lows, the return on cash is abysmal. Meanwhile, haven assets like developed market government bonds are trading at negative real yields, which means that investors are effectively paying for safety. It does seem like investment options are limited and often point in the direction of taking more risk just to generate seemingly paltry returns. Hence, it is little wonder that the most pressing concern for investors is how to engage market opportunities in the time of turbulence.

Admittedly, there is no fool-proof way to generate positive returns consistently, but we can at least employ strategies to mitigate the downside risks. Dollar cost averaging is one such strategy. The concept is deceptively simple; buy more units of an asset as prices fall and buy less of the asset as prices rise. The strategy works by buying a fixed dollar amount of assets periodically, enforcing a disciplined approach to market entry. It also diversifies the timing of market entry, making volatility a friend, not a foe.

Does dollar cost averaging guarantee a better outcome over lump sum investments every single time? Not necessarily. In a rising market, a lump sum approach yields better returns as more funds are exposed to rising asset prices. But these are volatile times. A constantly rising market is not guaranteed.

Rather than sit on the side-lines, patiently waiting for the storm clouds to recede, it is a far better approach to stay invested and participate in financial markets in a systematic and prudent fashion. For this purpose, dollar cost averaging offers an easy way out. A relatively stable investment vehicle that incorporates such a strategy is certainly welcome to navigate a more precarious market environment while also providing decent regular pay outs and potential returns.

About the fund

The Amundi-OCBC Momentum Fund investment strategy begins with investing in a diversified portfolio of globally sourced quality fixed income assets that provide reasonable yields to minimise issuer and credit risks. The bonds portfolio carries an investment grade rating on average. However, do note the fixed income allocation allows up to a maximum of 25% into non-investment grade bonds.

The portfolio of bonds will then be re-allocated systematically and periodically (monthly) between the 4th to 15th calendar month into a basket of equity market exchange traded funds (ETFs) starting from January 2021, such that with time, the portfolio reaches its target balanced state of global fixed income (50%) and global equities (50%).

This dollar cost averaging strategy helps to average out price fluctuations and steadily increase exposure in risk assets that will benefit from a gradual and sustained improvement in the operational environment and economic outlook.

The ETFs chosen have relatively low total expense ratios to ensure the overall cost of managing the fund remains well-contained. Investing in a variety of ETFs also provides diversification benefits, not just across company names, but also across regional markets, sectors and investment themes.

In terms of income, investors can benefit from potential distributions of up to 3% per annum paid out quarterly. Income distributions are derived from the basket of well-diversified high-quality global bonds and (later) dividend paying equity ETFs.

The fund might also appeal to investors with a target return in mind as it contains a built-in profit-taking feature which terminates the fund when its total return (inclusive of pay outs and capital appreciation) hits 30% of the respective share classes’ initial offer price. Investors will receive the proceeds and may continue their investment journey with other investment products.

Investors should also be aware of the risks. Investments in bonds naturally carry credit and liquidity risks, and these might impact the performance of the fund in the face of company-specific shocks and potential deterioration in economic and market conditions. On an individual ETF basis, there are risks of tracking error as well. These instruments track broader market indices and the prices will ebb and flow as market conditions evolve.

Fidelity Enhanced Reserve Fund

A steady vessel to navigate rough seas

Suitable for:

There are several risk events to watch out for in the fourth quarter, chief among them being the US presidential elections in November and the final leg of Brexit negotiations before the expiry of the transition period on 31 December. The US presidential election is expected to inject a great deal of volatility into the markets, not least because there is a risk of a contested election in the event of a close race, which could prolong the period of uncertainty about the outcome. US-China tensions may also escalate amid rising political temperatures ahead of the elections. These events are happening as the global economy continues to fight through another fresh wave of Covid-19 cases, which will inevitably hamper efforts to normalise economic activity. Still, we remain constructive about the long-term outlook for risk assets on the back of a gradually recovering global economy and a supportive policy environment that remains conducive for growth. Investors should take advantage of relatively stable investment vehicles that are invested in quality assets that provide reasonable yields to navigate choppy markets ahead.

Past Performance

| 1Y | -0.2% |

| 3Y | N.A. |

| 5Y | N.A. |

Why We Like the Fund

The fund might appeal to investors who want to invest but are not keen on taking too much risk amid an uncertain and turbulent market environment. The fund suffered a relatively shallow drawdown of about 3.8% during the March turmoil this year versus global stocks which plummeted more 30%. The fund has since clawed back all its losses. Year-to-date, it has delivered positive returns with less volatility compared to equity and higher-risk corporate bond indices. The fund’s resilient performance is largely attributed to its diversified portfolio composition. It is primarily invested in short-dated and high-quality global investment grade bonds, with some allocation into high yield credit. As at 31 August 2020, the portfolio has an average credit rating of A and targets a portfolio volatility of around 1%. Aside from aiming to provide an attractive level of risk adjusted total return, the fund also pays out regular monthly income.

About the Fund

| NAV as at 7 October 2020 | S$9.95 |

| Fund Inception Date | 26 March 2018 |

| Fund Size | S$1,797 mil |

| Annual Management Fee | 0.50% p.a. |

| Subscription Modes | Cash |

Top 5 Holdings

| % | |

| FID ILF USD FUND C ACC* | 9.03 |

| UST BILLS 0% 11/12/20 | 5.56 |

| UST BILLS 0% 02/18/21 | 3.89 |

| CHINA DEV BANK 2.97% 10/25/22 | 2.49 |

| CHINA CINDA 20 2% 03/18/23 RGS | 1.14 |

* This relates to the Fidelity Institutional Liquidity Fund (domiciled in Ireland) with underlying exposures predominantly in the US and developed Europe.

NAV Movement

Country Allocation

Source: NAV chart based on Bloomberg data as at 7 October 2020; fund information extracted from the fund’s factsheet provided by FIL Investment Management was as at 31 August 2020.

Note: Performance as at 31 August 2020, for the A-MINCOME(G)-SGD (H) share class, calculated on an offer-to-bid basis with all dividends and distributions reinvested, net of all charges payable upon reinvestment, if any. Performance figures exceeding 1 year, if any, were stated on an average annual compounded basis.

Fullerton USD Income Fund

Resist the frenzy. Go for quality.

Suitable for:

The Federal Reserve is expected to keep interest rates close to zero for a number of years, at least until actual inflation exceeds their 2% target. The lower for much longer interest rate environment will likely trigger a frenzied hunt for yield and may prompt investors to reach for riskier assets with higher returns. Amid the potential flurry of risk-taking behaviour, investors should remain prudent and guard against investing in products with flashy returns without fully assessing the risks. They should adopt a long-term view on their investments and focus on quality assets that can offer stable returns despite the difficult operating environment. They should also stay diversified and not concentrate their bets on a single security as they search of attractive yielding assets. Diversification is important to ride out the volatile environment ahead. A bond fund invested in a wide array of high-quality fixed income securities might be an appropriate solution that helps improve returns on idle cash amid the dismal interest rate environment and, minimise single issuer risks.

Past Performance

| 1Y | -0.15% |

| 3Y | 2.08% |

| 5Y | N.A. |

Why We Like the Fund

The fund’s investment strategy requires at least 70% of the portfolio to be invested in Investment Grade fixed income securities. These bonds should hold a minimum long-term credit rating of BBB- by Fitch, Baa3 by Moody’s or BBB- by Standard & Poor’s (or their respective equivalents). In addition, the fund manager has the flexibility to opportunistically invest up to 30% of the portfolio in non-Investment Grade High Yield securities. The fund is also able to tactically invest in local currency bonds to gain from potential yield pick-up that may enhance portfolio returns. The manager aims to invest at least 50% of the fund into US Dollar denominated bonds whilst aiming to provide regular quarterly income to investors with lower volatility relative to other asset classes. However, investors should note that a sharp deterioration in market conditions could adversely affect the fund’s overall performance.

About the Fund

| NAV as at 6 October 2020 | S$1.006 |

| Fund Inception Date | 15 April 2016 |

| Fund Size | S$846.00 mil |

| Annual Management Fee | 0.80% p.a. |

| Subscription Modes | SRS (for the SGD-Hedged share class only) / Cash |

Top 5 Holdings

| % | |

| Perusahaan Listrik Negara 4.125% May 2027 | 1.3 |

| Listrindo Capital Bv 4.95% Sep 2026 | 1.2 |

| Nanyang Commercial Bank 3.8% Nov 2029 | 1.1 |

| Malayan Banking Bhd 3.905% Oct 2026 | 1.1 |

| Parkway Pantai 4.25% PERP | 1 |

NAV Movement

Country Allocation

Source: NAV chart based on Bloomberg data as at 6 October 2020; fund information extracted from the fund’s factsheet provided by Fullerton Fund Management was as at 31 August 2020.

Note: Performance as at 31 August 2020, for Class A-SGD Hedged Share Class, calculated on an offer-to-bid basis with all dividends and distributions reinvested, net of all charges payable upon reinvestment, if any. Performance figures exceeding 1 year, if any, were stated on an average annual compounded basis.

Lion-OCBC Global Core Fund (Moderate)

Marrying the benefits of some active management with low cost investments

Suitable for:

Markets move and opinions change, but one adage has survived the test of time. A robust and diversified portfolio geared for the long term goes a long way. When focusing on the longer term, immediate market concerns – while notable – should not serve to distract from the initial investment goals. A robust portfolio diversified across various asset classes, as well as spread across an array of subclasses and industry sectors, may prove more resilient and is better able to weather different market conditions. The use of Exchange Traded Funds (ETFs) in a portfolio can be an added boost, as ETFs enable access to a huge range of investment options across asset classes, sectors and geographies. ETFs also add extra liquidity into a portfolio at a lower cost compared to traditional investment methods. Investors with a longer-term investment horizon but who do not wish to miss out on current market opportunities may choose to invest partially in a core portfolio and rotate selectively among other market driven strategies.

Past Performance

| 1Y | -6.8% |

| 3Y | -0.8 |

| 5Y | N.A. |

Why We Like the Fund

The Lion-OCBC Global Core Fund is a cost-effective, Exchange Traded Funds-based (ETF-based) investment solution that is diversified globally and across multiple asset classes. The portfolio is rebalanced regularly to stay relevant and adjust to changing market conditions. This concept of a fund of ETFs and relatively less active management allows the fund manager to charge investors a lower annual management fee of 0.6% per annum. The Moderate and Growth funds offer potential pay-outs, paid quarterly. However, it is important to note that these distributions are not guaranteed and are dependent on market conditions.

About the Fund

| NAV as at 7 October 2020 | S$0.900 |

| Fund Inception Date | 31 July 2017 |

| Fund Size | US$17.8 mil |

| Annual Management Fee | 0.6% p.a. |

| Subscription Modes | Cash, SRS (for SGD-H Class 0 share class) |

Top 5 Holdings

| % | |

| ISHARES USD SHORT DURATION HIGH YIELD CORP BOND UCITS ETF USD DIST | 17.7 |

| ISHARES USD TREASURY BOND 1-3YR UCI TS ETF | 17 |

| ISHARES MSCI USA MIN VOL FACTOR ETF | 8.9 |

| ISHARES USD HIGH YIELD CORP BOND UCITS ETF | 8.9 |

| ISHARES CORE HIGH DIVIDEND ETF | 8.8 |

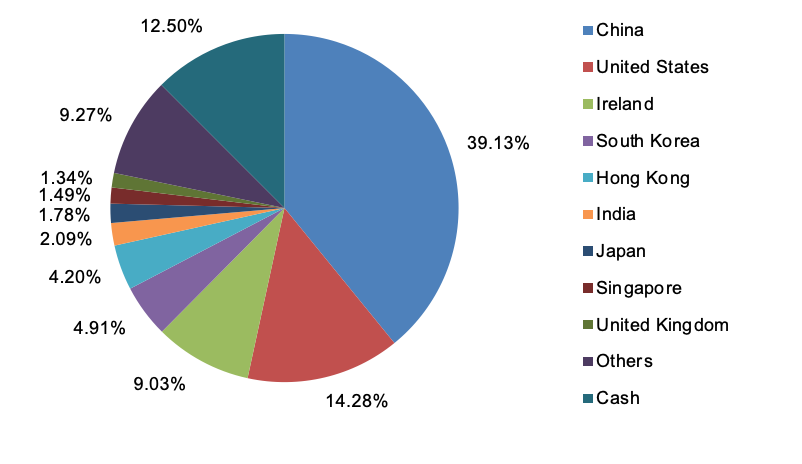

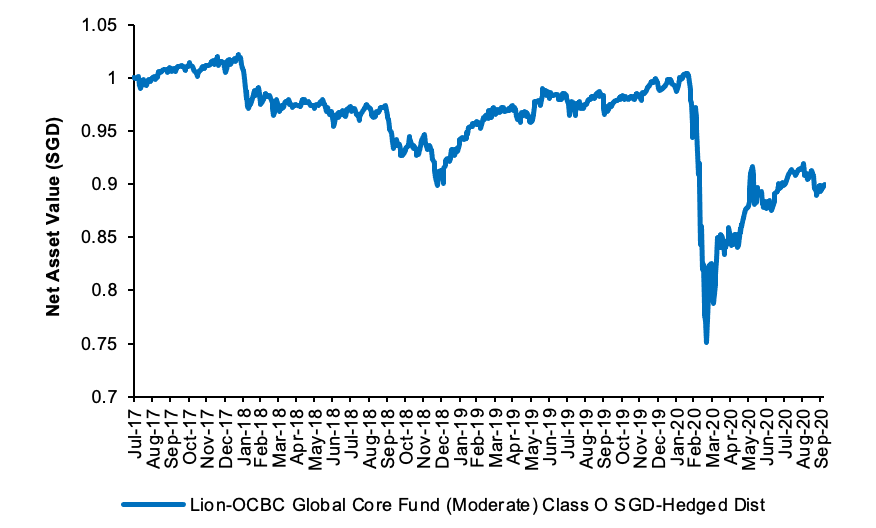

NAV Movement

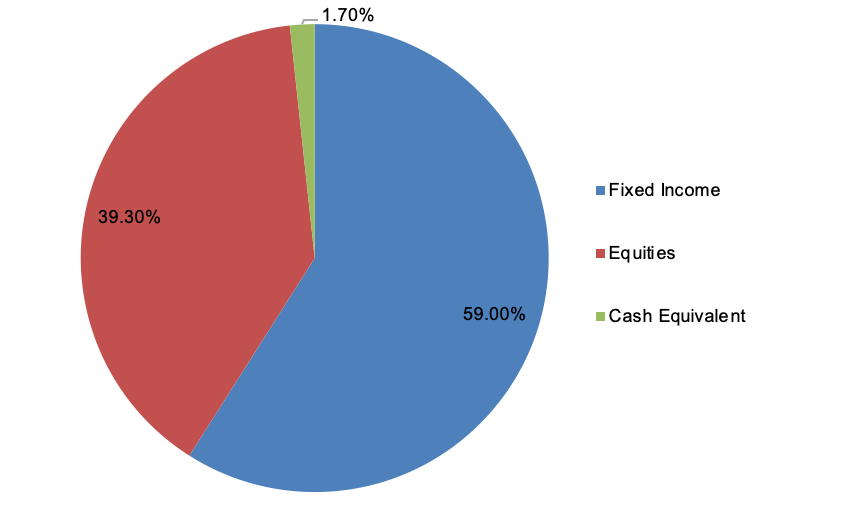

Asset Class Allocation

Source: NAV chart based on Bloomberg data as at 7 October 2020; fund information extracted from the fund’s factsheet provided by Lion Global Investors Limited was as at 31 August 2020.

Note: Performance as at 31 August 2020, for the Class O SGD-Hedged Dist Share Class, calculated on an offer-to-bid basis with all dividends and distributions reinvested, net of all charges payable upon reinvestment, if any. Performance figures exceeding 1 year, if any, were stated on an average annual compounded basis.

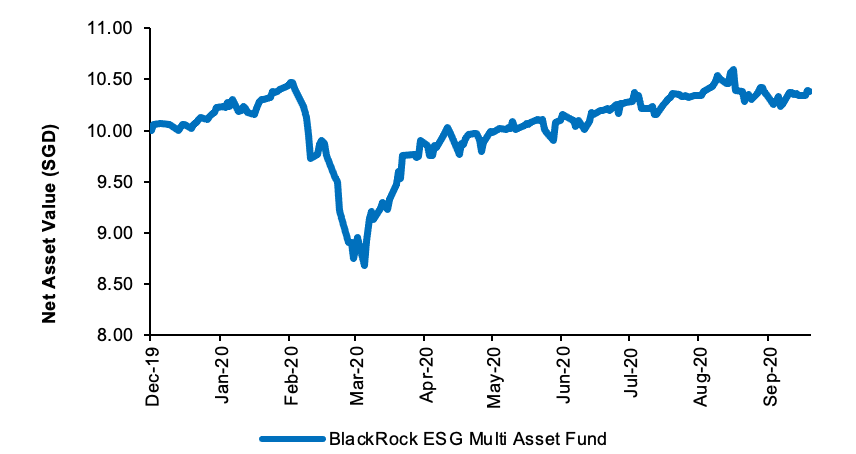

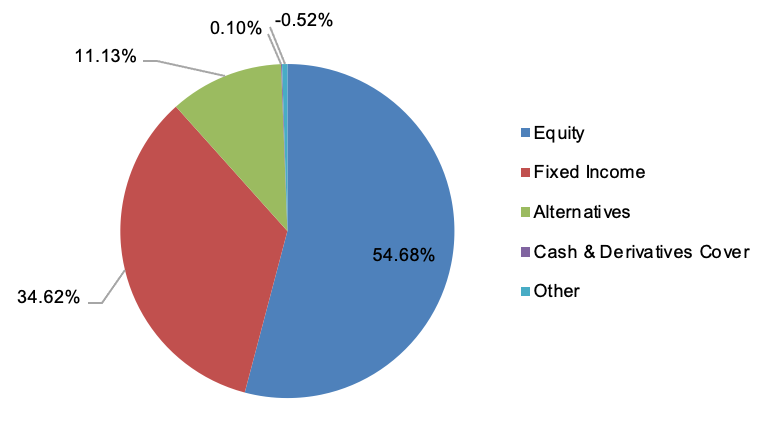

BlackRock ESG Multi-Asset Fund

Doing well by doing good

Suitable for:

Socially responsible investing or sustainable investing can be described as an investment approach that is guided by the aim of achieving a better and more sustainable future for society as a whole. The collective betterment of society is included as a key criterion when assessing an investment opportunity. More specifically and on a practical note, individual companies are judged and rated on Environmental, Social and Governance factors (also referred to as ESG) in the investment process. Taken loosely, ESG, sustainable investing and socially responsible investing are one and the same. The key idea is to invest in companies with good controls, healthy employment practices and socially responsible business models. Research shows that companies with better ESG profiles tend to be able to borrow more cheaply and enjoy higher credit rankings and lower cost of equity capital. Essentially, companies with better ESG scores are better quality assets. In addition, companies with the strongest ESG practices relative to their peers tend to be more profitable, have less volatile earnings and are better at mitigating serious business risk that can lead to large financial losses and bankruptcies. Such quality assets can provide some downside protection to portfolios in times of market stress.

Past Performance*

| 1Y | 4.21% |

| 3Y | 4.94% |

| 5Y | 3.70% |

*Based on Class A2 EUR share class

Why We Like the Fund

The fund follows an asset allocation policy that seeks to maximise total return in a manner consistent with the principles of environmental, social and governance (ESG) focussed investing. Within this framework, the fund aims to reduce risk through the exclusion of 9 controversial sectors and violators of the UN Global Compact, which is a non-binding pact to adopt sustainable and socially responsible policies. The fund seeks to boost portfolio resilience by investing only in firms with an ESG rating of BBB and above as well as focus on thematic investment opportunities that drive positive societal change. The fund invests globally in the full spectrum of permitted investments, including equities, fixed income and money market instruments. The fund also strives to pay a potential distribution of 3 – 3.5% per annum monthly.

About the Fund

| NAV as at 7 October 2020 | S$10.38 |

| Inception Date | 18 December 2019 |

| Fund Size | EUR 1,116.35 mil |

| Annual Management Fee | 1.20% p.a. |

| Subscription Modes | Cash |

Top 5 Holdings

| % | |

| TREASURY NOTE 1.5 02/15/2030 | 4.93 |

| ISH MSCI USA SRI ETF USD ACC | 4.6 |

| MICROSOFT CORP | 3.47 |

| ISHARES PHYSICAL GOLD | 3.4 |

| ITALY (REPUBLIC OF) 1.35 04/01/2030 | 2.68 |

NAV Movement

Asset Class Allocation

Source: NAV chart (for the A8 SGD Hedged share class) based on Bloomberg data as at 7 October 2020; fund information extracted from the fund’s factsheet (A8 SGD Hedged share class) provided by BlackRock Investment Management was as at 31 August 2020.

Note : Performance as at 31 August 2020, for the Class A2 EUR share class, calculated on an offer-to-bid basis with all dividends and distributions reinvested, net of all charges payable upon reinvestment, if any. Performance figures exceeding 1 year, if any, were stated on an average annual compounded basis.

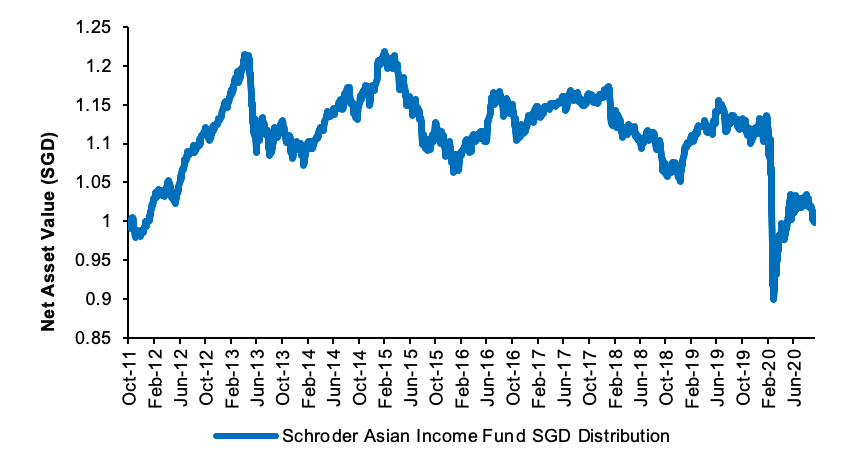

Schroder Asian Income Fund

Asia ex-Japan: Unbowed, unbent, unbroken

Suitable for:

Asia continues to lead the way in the effective handling of the Covid-19 pandemic. Although there has been a resurgence of cases in this side of the world as economies relax containment measures, it has not reached critical levels that merit the sorts of extreme actions we observed in the second quarter. Asia ex-Japan is largely expected to post positive GDP growth this year, mostly buoyed by China’s recovery, versus expectations of firmly negative growth in Europe and the US. Consensus forecasts likely reflects the “first in first out” effect as it relates to the Covid-19 crisis. Asia was also somewhat less affected by the September sell-off with the MSCI Asia ex-Japan index sliding just 1.68% for the month versus developed market stocks which fell 3.60%, as measured by the MSCI World Index. In light of risks emanating from escalating US-China tensions and lingering uncertainty about the US presidential elections, volatile market conditions will continue to sustain in the near-term. Still, we remain constructive on Asia ex-Japan’s long-term growth outlook and would engage opportunities in the region via an actively managed and diversified portfolio of stocks and bonds to ride out near-term turbulence.

Past Performance

| 1Y | -9.7% |

| 3Y | -1.1% |

| 5Y | 2.4% |

Why We Like the Fund

The fund aims to provide regular monthly income and potential capital growth over the medium to longer term by investing primarily in Asian equities and Asian fixed income securities. The fund prefers businesses that generate sustainable quality cash flows and pays out a sustainable yield. The fund is also defensively positioned with a focus on capital preservation, which increases the portfolio’s resilience against potential ructions in a turbulent market. Investors may benefit from the fund’s active asset allocation strategy, which seeks to maximise the yield and total return of the portfolio across different market environments. However, investors should note that past performance is not indicative of future performance. A sharp deterioration of market conditions amid potential flare-ups in trade tensions and geopolitical risks could affect the fund’s overall performance.

About the Fund

| NAV as at 6 October 2020 | S$1.005 |

| Fund Inception Date | 21 October 2011 |

| Fund Size | S$5,027.59 mil |

| Annual Management Fee | 1.25% p.a. |

| Subscription Modes | Cash/ SRS |

Top 5 Equity Holdings

| % | |

| HK Electric Investments Units Ltd | 2.4 |

| AusNet Services Ltd | 2.1 |

| Power Grid Corporation of India Ltd | 1.7 |

| Power Assets Holdings Ltd | 1.7 |

| Ascendas Real Estate Investment Trust | 1.4 |

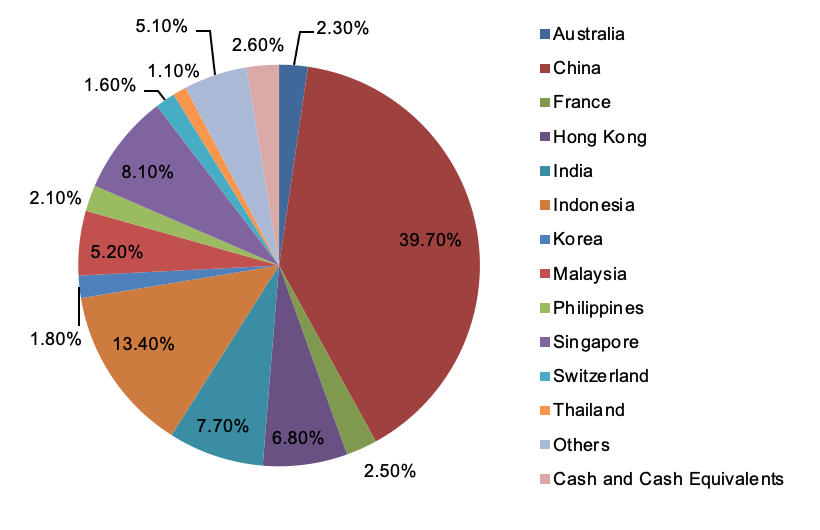

NAV Movement

Sector Allocation

Source: NAV chart based on Bloomberg data as at 6 October 2020; fund information extracted from the fund’s factsheet provided by Schroder Investment Management was as at 31 August 2020.

Note: Performance as at 31 August 2020 for the SGD Distribution share class only, calculated on an offer-to-bid basis with all dividends and distributions reinvested, net of all charges payable upon reinvestment, if any. Performance figures exceeding 1 year, if any, were stated on an average annual compounded basis.

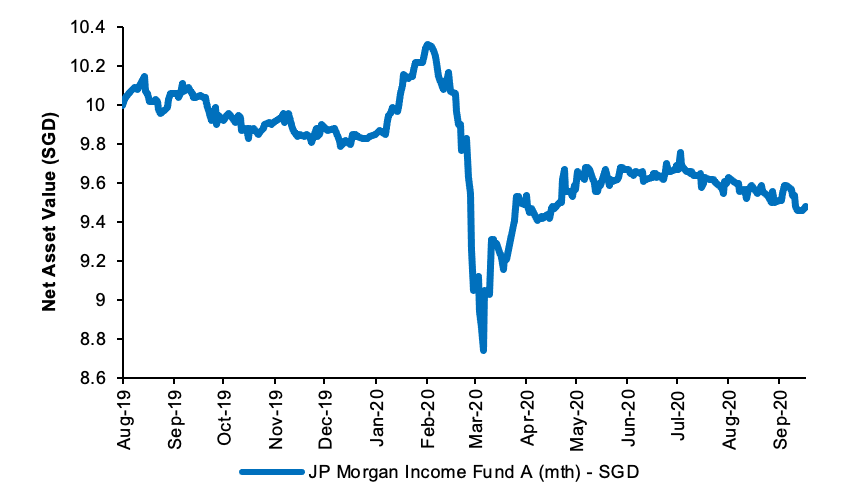

JPMorgan Income Fund

Predictable income in unpredictable times

Suitable for:

With stocks trading at fairly extended valuations, there is admittedly limited scope for robust gains via further capital appreciation, especially given that we are not working off a low base and that the economic outlook remains deeply uncertain. The volatile market environment complicates this prospect as well. As a result, income — via dividends from stocks and coupons from bonds — will become an important driver of total return. Amid the uncertain macro environment, troubled by a litany of risks including a resurgence of Covid-19 cases, political uncertainties associated with the US presidential and congressional elections and Brexit, finding a predictable and sustainable source of regular income might be tricky. Indeed, amid the challenging operational backdrop, creating diversified income streams through careful stock and bond selection remains crucial. However, this is often easier said than done. Rather than expend huge amounts of time and effort to do this from the ground up, investors can take advantage of the wide array of investment funds that have a proven track record of delivering consistent and predictable income.

Past Performance

| 1Y | -0.31% |

| 3Y | N.A. |

| 5Y | N.A. |

Why We Like the Fund

The JPMorgan Income Fund generates attractive and predictable monthly income while tightly controlling risk. The fund does this by employing an unconstrained and dynamic approach to source for the best investment ideas spread out across a wide range of fixed income assets, while actively managing duration risks. Doing so allows the fund to diversify risk premiums and deliver a high-yield-like income stream with lower volatility. Such diversification also provides some downside protection during periods of market stress. A key driving factor behind the fund’s ability to deliver such consistent and predictable pay-outs is its proprietary income bank or reserve, which helps smoothen out “lumpy” cash flow distributions and protects against possible fluctuations in interest rates.

About the Fund

| NAV as at 7 October 2020 | S$9.48 |

| Fund Inception Date | 14 August 2019 |

| Fund Size | US$6894.2 mil |

| Annual Management Fee | 1.00% p.a. |

| Subscription Modes | Cash |

Top 5 Holdings

| % | |

| FNMA (United States) MBS 01/06/50 | 6.5 |

| FNMA (United States) MBS 01/07/50 | 2.4 |

| JPM Global High Yield Bond Fund (Luxembourg) Corporate | 1.3 |

| FHLM (United States) MBS 15/01/49 | 0.9 |

| FHLM (United States) MBS 25/03/50 | 0.6 |

NAV Movement

Regional Allocation

Source: NAV chart based on Bloomberg data as at 7 October 2020; fund information extracted from the fund’s factsheet provided by JPMorgan Asset Management as at 31 August 2020.

Note: Performance as at 31 August 2020, for the A (mth) – SGD Share Class, calculated on an offer-to-bid basis with all dividends and distributions reinvested, net of all charges payable upon reinvestment, if any. Performance figures exceeding 1 year, if any, were stated on an average annual compounded basis.

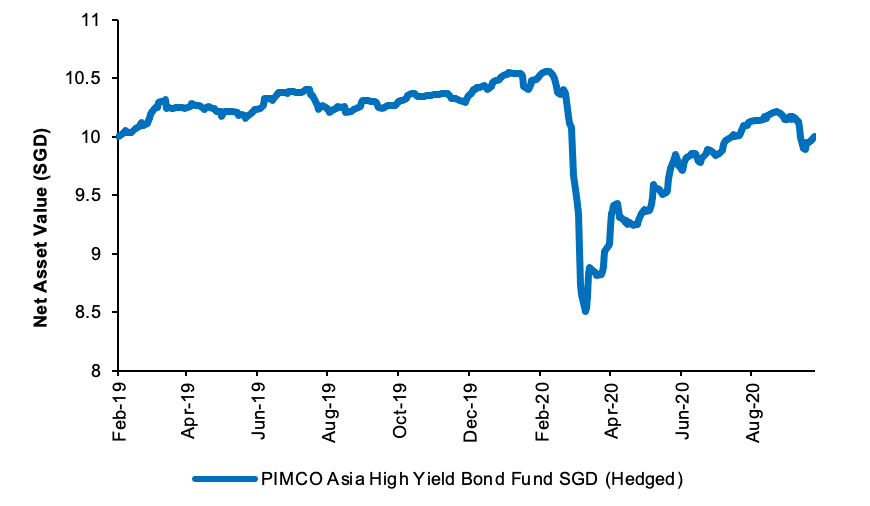

PIMCO Asia High Yield Bond Fund

Compelling case for Asian High Yield still intact

Suitable for:

We remain constructive on emerging market (EM) high yield bonds with a preference for Asia over the medium-term for a few reasons. First, the Federal Reserve’s dovish bent and accommodative monetary policy stance should remain supportive of bonds generally. Second, there are increasingly fewer compelling fixed income alternatives that offer similar, if not better, risk-adjusted returns. Third, the gradual economic recovery and the likely passage of an expansionary fiscal stimulus bill through Congress regardless who the next president is should provide a supportive growth tailwind for this asset class. Still, we are mindful of rising default risks in emerging markets due to the challenging, virus-stricken operating environment and increased volatility due to persistent US-China tensions. It is also important to note that in the coming weeks leading up to the US elections, EM high yield could underperform due to risk-off positioning amidst higher volatility. As such, we would pay careful attention to credit selection and advocate diversification across a wide range of issuers to mitigate these downside risks. An Asia-focussed High Yield fund would be useful to express these investment views.

Past Performance

| 1Y | -0.54% |

| 3Y | N.A. |

| 5Y | N.A. |

Why We Like the Fund

The fund seeks to maximise total return through investments in US Dollar denominated Asian High Yield credits. Each credit that the fund invests in is independently rated by PIMCO’s internal credit team. Importantly, the fund only invests in credits that PIMCO assesses to be fundamentally strong. As the fund is focused on maximising total returns as opposed to just delivering yield, they are not forced to invest in higher yielding credits which might exhibit weaker fundamentals just to maximise portfolio yield. Fundamentally, the fund provides exposure to the rapidly growing Asian High Yield market, which today offers attractive potential risk-adjusted return versus other credit asset classes. It also exhibits less interest rate sensitivity compared to global Investment Grade and Emerging Market bonds. Nevertheless, the fund is still subjected to credit risks in the event these companies default, and market risks should the value of its underlying fixed income securities fluctuate.

About the Fund

| NAV as at 7 October 2020 | S$10.00 |

| Fund Inception Date | 14 February 2019 |

| Fund Size | US$403.3 mil |

| Annual Management Fee | 1.55% p.a. |

| Subscription Modes | Cash, SRS (for the SGD-Hedged share classes |

Top 5 Holdings

| % | |

| CHINA EVERGRANDE GROUP CO GTD SR UNSEC | 1.7 |

| YUZHOU PROPERTIES CO LTD | 1.4 |

| THIRD PKSTAN INTL SUKUK REGS | 1.3 |

| KAISA GROUP HOLDINGS LTD SEC | 1.3 |

| CHINA EVERGRANDE GROUP SEC | 1.2 |

NAV Movement

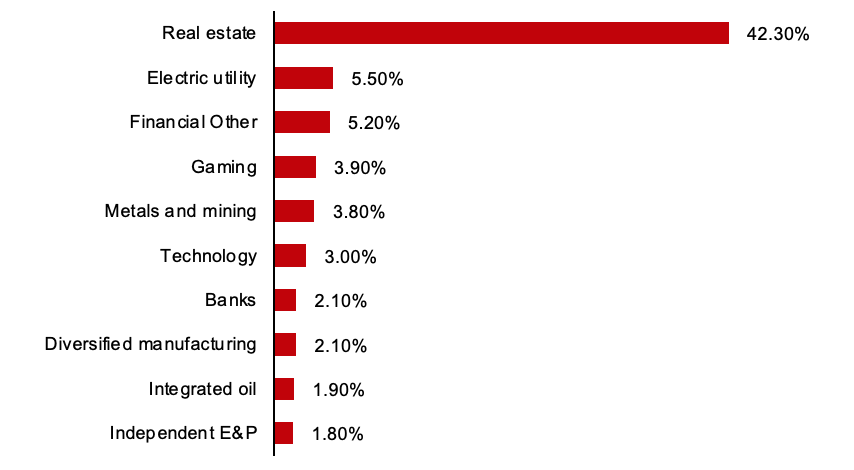

Top 10 Sector Exposure

Source: NAV chart based on Bloomberg data as at 7 October 2020; fund information extracted from the fund’s factsheet provided by PIMCO Funds as at 31 August 2020.

Note: Performance as at 31 August 2020 for the SGD (Hedged) Class E share class, calculated on an offer-to-bid basis with all dividends and distributions reinvested, net of all charges payable upon reinvestment, if any. Performance figures exceeding 1 year, if any, were stated on an average annual compounded basis.