Retirement Planning

December 2019

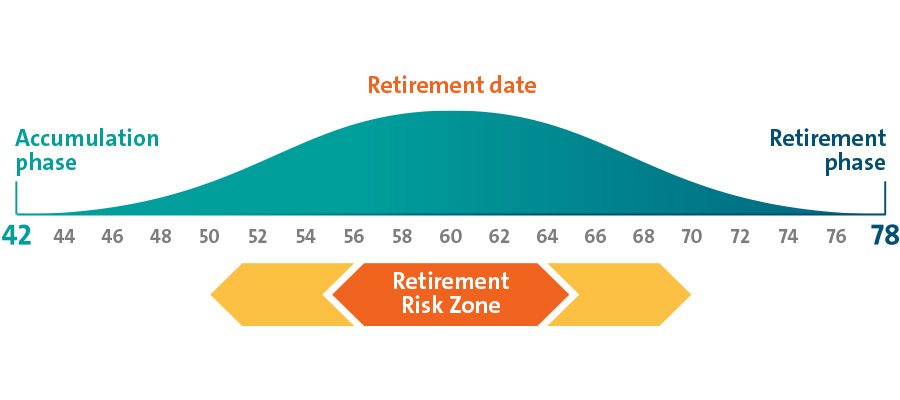

Is my retirement at risk?

No matter how well thought-out your retirement plan might be, it will have to undergo some changes in the five to ten years before you actually retire.

Earlier on in your career, your portfolio was designed to grow your wealth, even if it meant taking on greater risk.

But as retirement draws closer, you enter what is known as the “Retirement Risk Zone”. If you don’t make appropriate changes to your portfolio, you risk jeopardising your desired retirement lifestyle.

What is the Retirement Risk Zone?

The Retirement Risk Zone is a critical period when your investment portfolio becomes particularly vulnerable.

This is typically a period spanning five years before you plan to retire and the first five years after retirement.

At this stage, any market downturns can have a direct effect on your retirement mass, since you do not have another decade or two to ride out the ups and downs.

For instance, high-risk investment vehicles like individual stocks are extremely vulnerable to market fluctuations, but nonetheless can be good long-term investments if they appreciate in value in the long-term.

Younger investors who do not need to derive an income from their investments in the near future can afford to wait for market downturns to run their course.

However, when retirement is on the horizon, you do not want to run the risk of your investments suffering from market downturns, as they can have a lasting impact on your retirement income. Reducing the risk in your portfolio is crucial at this stage.

Fear not, however. You can safeguard yourself from the heightened risk during this period. The solution is simply to shift your focus from riskier, higher-yield investments to lower-risk, income-yielding ones.

Here are three easy steps you can take to adjust your portfolio to protect your wealth and mitigate the dangers of being in the Retirement Risk Zone.

1. Decide how to allocate your wealth and investments now that you are about to enter retirement.

Ideally, you want to reduce the percentage of your wealth held in risky products such as individual stocks or single country equity funds.

At the same time, you want to increase your allocation of stable, income yielding assets such as endowment plans and diversified multi-asset funds.

These assets are less vulnerable to market fluctuations, so your retirement will not suffer great blows even if there is a market downturn just before you wish to retire.

2. Examine your portfolio and reallocate your assets according to your new plan.

Now that you have come up with a well-thought out strategy, you will need to examine your portfolio and make changes so that your asset allocation follows the plan.

You are likely to find that the proportion of your wealth in riskier investment vehicles is too high for your liking. You will thus want to shift a portion of this to lower-risk vehicles.

Some examples of low-risk investments include structured deposits, multi-asset income funds or fixed maturity bond-funds. If you find that your portfolio contains too much risk, you should focus on lowering your risk by allocating a larger proportion of your investments to such vehicles.

3. Rebalance your portfolio regularly.

Rebalancing of your portfolio should be carried out at regular intervals. That is because over time, a larger and larger proportion of your portfolio is likely to creep towards higher-risk assets.

When you rebalance your portfolio, you are restoring your asset allocation to the original proportions according to your retirement plan. In doing so, you are once again lowering your risk to comfortable levels.

So long as you are careful to ensure that you are never taking on more risk than you should, you are protecting yourself from the dangers of the Retirement Risk Zone while ensuring you have a healthy cash flow to enjoy in retirement.

With the OCBC Bank’s approach to your Silver Years, we help you make the right decisions so that you stay protected and your funds are safeguarded while you’re in the Retirement Risk Zone. We help you mitigate the risks while achieving your retirement goals, so you can enter your Silver Years with a smile.

Click here to find out more about OCBC Bank’s approach to your Silver Years

This is for general information and does not take into account your particular investment and protection aims, financial situation or needs. You should seek advice from a financial adviser before committing to a purchase. Otherwise, you should consider the suitability of the investment.

The information provided herein is intended for general circulation and/or discussion purposes only. It does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The information in this document is not intended to constitute research analysis or recommendation and should not be treated as such.

Without prejudice to the generality of the foregoing, please seek advice from a financial adviser regarding the suitability of any investment product taking into account your specific investment objectives, financial situation or particular needs before you make a commitment to purchase the investment product. In the event that you choose not to seek advice from a financial adviser, you should consider whether the product in question is suitable for you. This does not constitute an offer or solicitation to buy or sell or subscribe for any security or financial instrument or to enter into a transaction or to participate in any particular trading or investment strategy.

The information provided herein may contain projections or other forward looking statement regarding future events or future performance of countries, assets, markets or companies. Actual events or results may differ materially. Past performance figures are not necessarily indicative of future or likely performance. Any reference to any specific company, financial product or asset class in whatever way is used for illustrative purposes only and does not constitute a recommendation on the same. Investments are subject to investment risks, including the possible loss of the principal amount invested.

The Bank, its related companies, their respective directors and/or employees (collectively “Related Persons”) may or might have in the future interests in the investment products or the issuers mentioned herein. Such interests include effecting transactions in such investment products, and providing broking, investment banking and other financial services to such issuers. The Bank and its Related Persons may also be related to, and receive fees from, providers of such investment products.

No representation or warranty whatsoever (including without limitation any representation or warranty as to accuracy, usefulness, adequacy, timeliness or completeness) in respect of any information (including without limitation any statement, figures, opinion, view or estimate) provided herein is given by OCBC Bank and it should not be relied upon as such. OCBC Bank does not undertake an obligation to update the information or to correct any inaccuracy that may become apparent at a later time. All information presented is subject to change without notice. OCBC Bank shall not be responsible or liable for any loss or damage whatsoever arising directly or indirectly howsoever in connection with or as a result of any person acting on any information provided herein.

The contents hereof may not be reproduced or disseminated in whole or in part without OCBC Bank's written consent. The contents are a summary of the investment ideas and recommendations set out in Bank of Singapore and OCBC Bank reports. Please refer to the respective research report for the interest that the entity might have in the investment products and/or issuers of the securities.

This advertisement has not been reviewed by the Monetary Authority of Singapore.

Cross-Border Marketing Disclaimers

Please click here for OCBC Bank's cross border marketing disclaimers relevant for your country of residence.