OCBC Group Full Year 2024 Net Profit grew 8% to a Record S$7.59 billion

OCBC Group Full Year 2024 Net Profit grew 8% to a Record S$7.59 billion

S$2.5 billion capital return over two years

Singapore, 26 February 2025 – Oversea-Chinese Banking Corporation Limited (“OCBC”) reported net profit of S$7.59 billion for the financial year ended 31 December 2024 (“FY24”), 8% higher as compared to S$7.02 billion in the previous year (“FY23”).

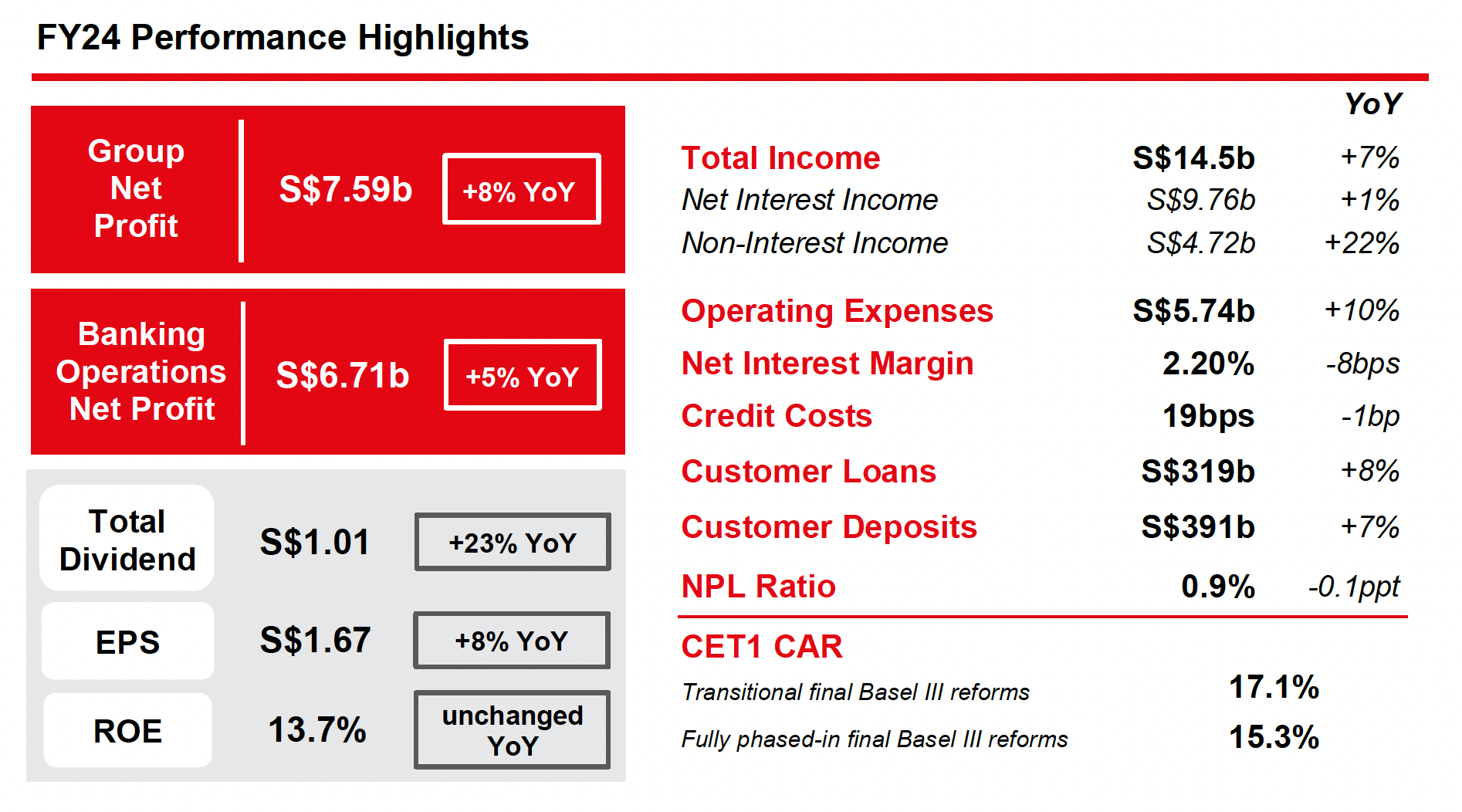

OCBC’s resilient performance demonstrated the strength of its well-diversified business franchise of Banking, Wealth Management and Insurance. Group net profit was driven by robust income growth across its three key businesses and lower allowances. Total income surged above S$14 billion for the first time, fuelled by record net interest income, and strong non-interest income propelled by a rise in wealth fees, a new high in trading income and an increase in insurance income. Asset quality remained sound with non-performing loan ratio at 0.9%.

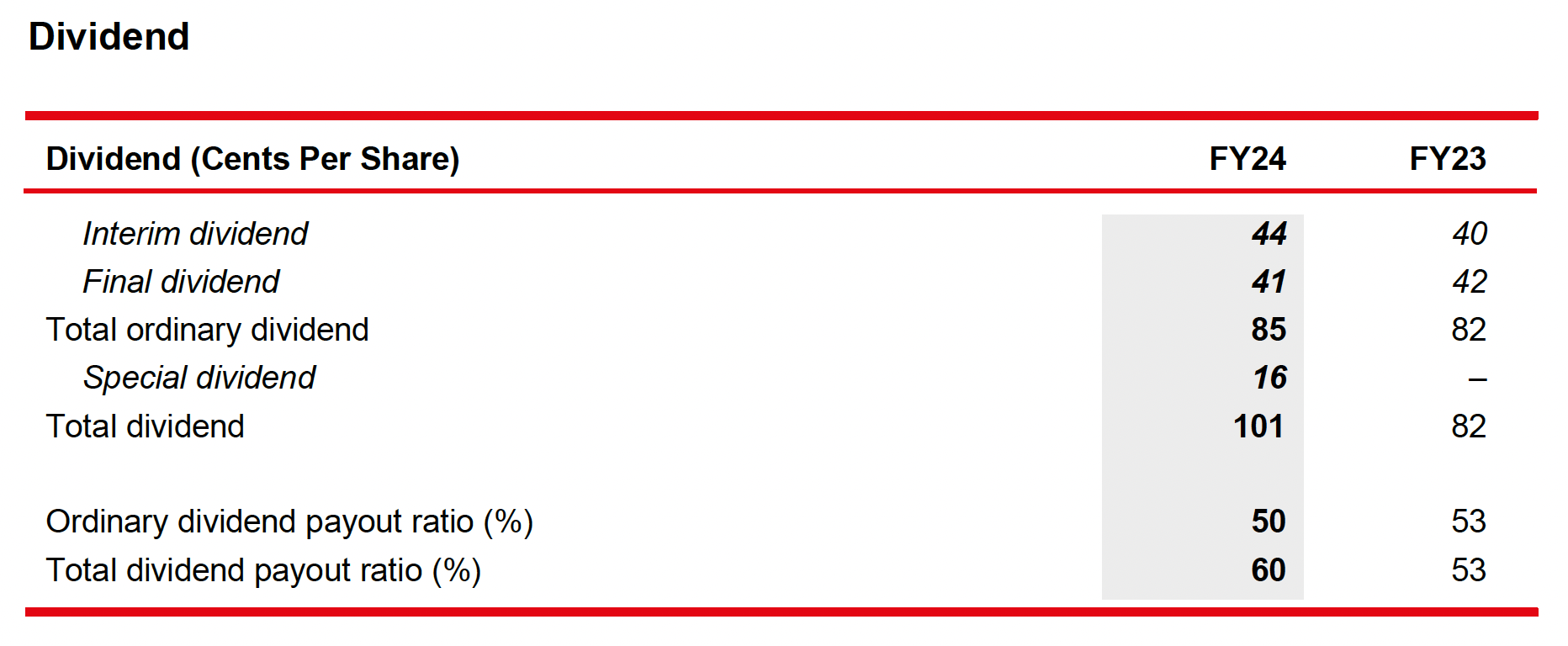

With OCBC’s sustained earnings growth and strong capital position, the Board has announced a comprehensive approach to return S$2.5 billion of capital to shareholders over two years via special dividends and share buybacks. The capital return comprises special dividends amounting to 10% of the Group’s net profit for FY24 and FY25, with the balance via share buybacks over two years, subject to market conditions and regulatory approvals. Together with OCBC’s target ordinary dividend payout ratio of 50%, the total dividend payout for FY24 and FY25 will amount to 60% annually. For FY24, a final ordinary dividend of 41 cents per share is proposed, bringing the total ordinary dividend to 85 cents per share, or payout ratio of 50%. The Board is also recommending a special dividend of 16 cents per share or payout ratio of 10% at the upcoming 2025 Annual General Meeting. This will bring the FY24 total dividend payout to 60% of net profit.

FY24 Year-on-Year Performance

Group net profit grew 8% to a record S$7.59 billion.

- Net interest income rose to a new high of S$9.76 billion, underpinned by a 5% increase in average assets from customer loans, and high-quality assets which were income accretive but lower yielding. Net interest margin (“NIM”) was 8 basis points lower at 2.20%, as the rise in funding costs outpaced the increase in asset yields.

- Non-interest income growth was broad-based, rising 22% to S$4.72 billion.

- Net fee income increased 9% to S$1.97 billion, bolstered by a 22% rise in wealth management fees across all wealth channels. Investment banking and loan-related fees were also higher.

- Net trading income surged 53% to S$1.54 billion. Customer flow treasury income rose to a new high, underpinned by both consumer and corporate segments. Non-customer flow treasury income more than doubled from a year ago, lifted by strong investment performance from Global Markets and Great Eastern Holdings (“GEH”).

- Insurance income grew 14% to S$917 million, led by higher income from the underlying insurance business and improved claim experience. Total weighted new sales rose 8% to S$1.80 billion, while new business embedded value (“NBEV”) was S$622 million.

- The Group’s wealth management income, comprising income from private banking, premier private client, premier banking, insurance, asset management and stockbroking, increased 13% to a record S$4.89 billion. Group wealth management income accounted for 34% of total income, up from 32% in the previous year. Our Banking wealth management AUM rose 14% to a new high of S$299 billion, driven by net new money inflows and positive market valuation.

- Operating expenses grew 10% to S$5.74 billion as the Group continued to invest in strategic initiatives and pursue business growth. Staff costs were higher, mainly attributable to headcount increase, higher variable compensation in line with income growth, as well as from annual salary increments. The increase in expenses was also partly due to the consolidation of PT Bank Commonwealth from May 2024, which was fully integrated into OCBC Indonesia in September 2024. Cost-to-income ratio for FY24 was 39.7%.

- Total allowances were 6% lower at S$690 million, and total credit costs of 19 basis points of loans were below the previous year’s 20 basis points.

- Share of results of associates rose 4% to S$994 million, from S$953 million a year ago.

- The Group’s return on equity of 13.7% was comparable to FY23, and earnings per share was 8% higher at S$1.67.

4Q24 Year-on-Year Performance

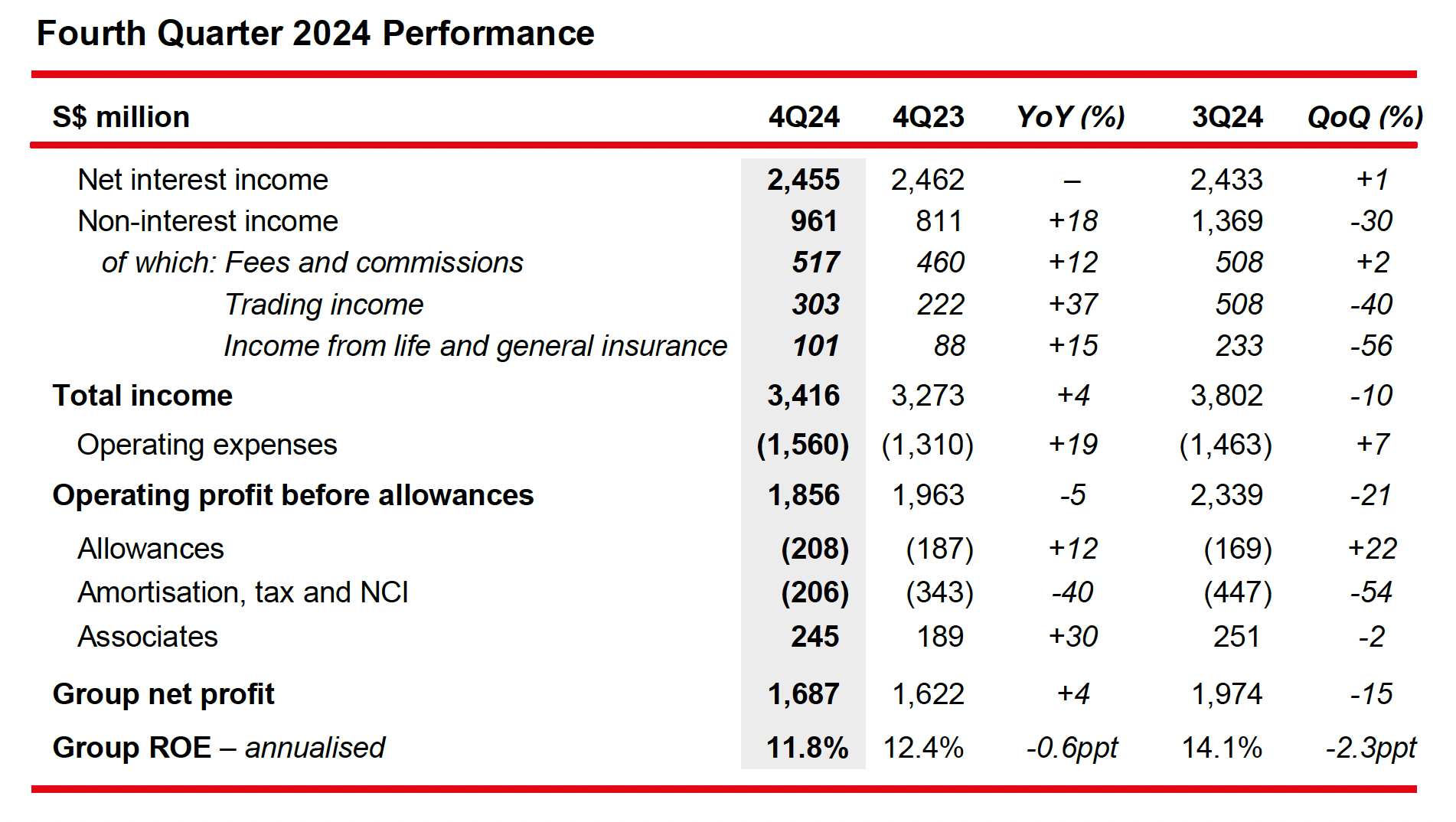

Group net profit of S$1.69 billion was 4% higher compared to S$1.62 billion a year ago.

- Net interest income was relatively unchanged at S$2.46 billion, as a 6% increase in average assets mitigated a 14 basis-point NIM contraction to 2.15%. The decline in NIM was the result of loan yields tightening at a faster pace than the drop in deposit costs, which were associated with federal funds rate cuts in the second half of 2024.

- Non-interest income grew 18% to S$961 million, boosted by improved fee, trading and insurance income.

- Insurance income of S$101 million was higher than S$88 million a year ago.

- Operating expenses grew 19% to S$1.56 billion, led by higher staff costs associated with a rise in headcount, variable compensation and annual salary increments.

- Total allowances were S$208 million as compared to S$187 million a year ago.

- Share of results of associates rose 30% to S$245 million.

4Q24 Quarter-on-Quarter Performance

Group net profit was 15% below the previous quarter. This was partly attributable to lower insurance income due to a negative impact from changes in the medical insurance environment in GEH’s key markets.

- Net interest income rose 1% from the previous quarter to S$2.46 billion, primarily attributable to a 2% increase in average assets which more than offset a 3 basis-point decline in NIM.

- Non-interest income was S$961 million, as compared to S$1.37 billion in the preceding quarter. Fee income rose 2%, while trading income was 40% lower than last quarter, partly due to seasonality.

- Insurance income of S$101 million was substantially lower than S$233 million in 3Q24, due to the above-mentioned negative impact recognised.

- Operating expenses increased 7% to S$1.56 billion, which included higher IT-related and year-end business promotion costs, as well as expenses incurred to invest in the Group’s strategic initiatives. A one-off payment totalling S$7.5 million to junior employees, to assist with ongoing cost-of-living pressures, was also set aside in the fourth quarter.

- Total allowances were higher quarter-on-quarter, with credit costs at 21 basis points.

- Share of results of associates was 2% lower than the previous quarter.

Non-performing assets (“NPAs”)

- Total NPAs declined 1% from a year ago to S$2.87 billion as at 31 December 2024. The 3% increase from the previous quarter was largely related to one Hong Kong corporate account in the commercial real estate sector.

- NPL ratio was 0.9%, below the NPL ratio of 1.0% a year ago and unchanged from the previous quarter. Total NPA coverage stood at 159%.

Allowances

- For FY24, total allowances were 6% lower year-on-year at S$690 million, with credit costs at 19 basis points.

- Total allowances for 4Q24 of S$208 million were higher as compared to S$169 million in 3Q24. This was attributable to an increase in allowances for impaired assets set aside, mainly for the above-mentioned Hong Kong corporate account, which more than offset the decline in allowances for non-impaired assets.

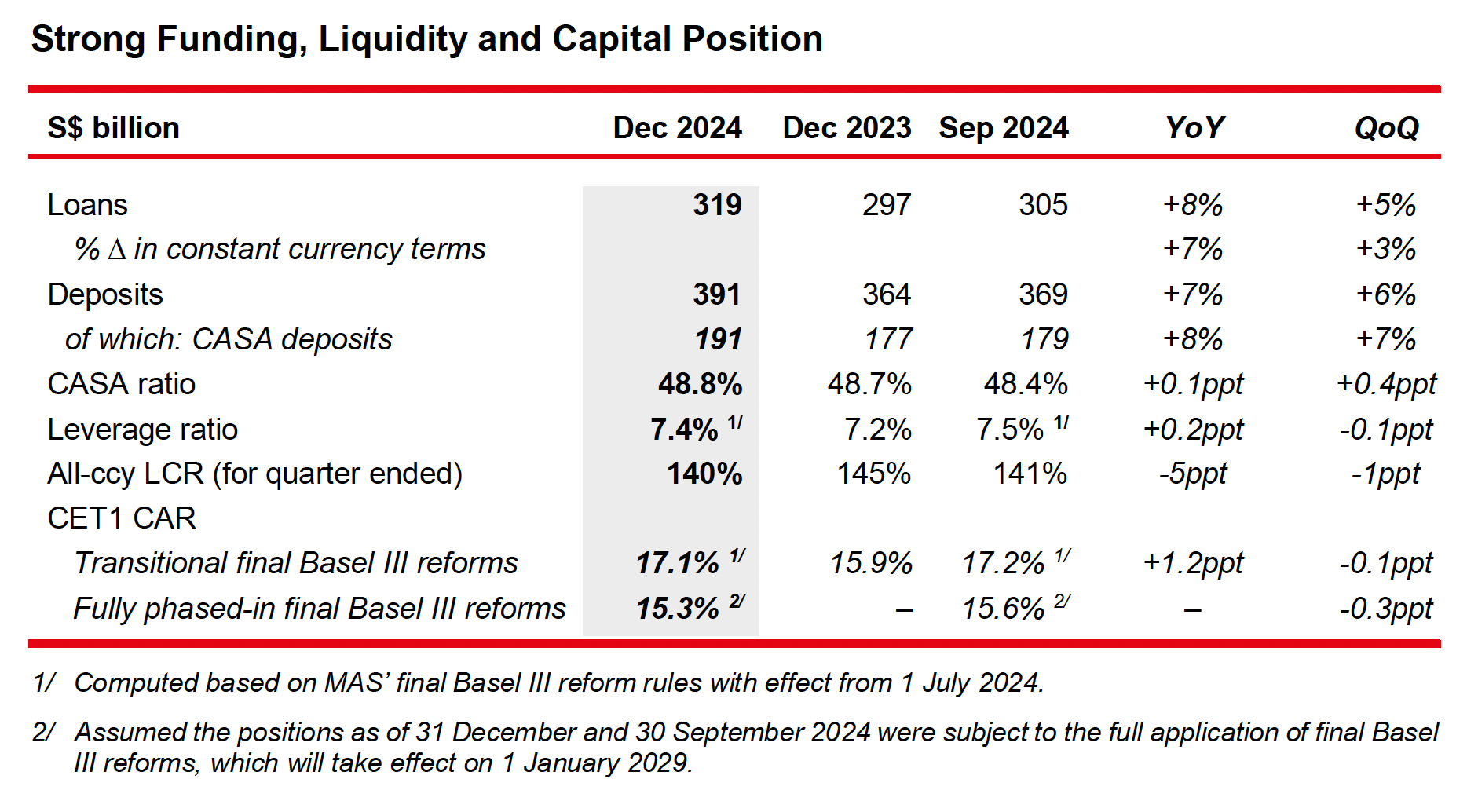

- Customer loans grew 8% from a year ago to S$319 billion as at 31 December 2024, lifted by loan growth across the Group’s core markets and key international markets.

- Loan growth for the year was broad-based across all industries and was driven by housing loans, as well as trade and non-trade corporate loans. The increase in non-trade corporate loans included lending to the technology, digital infrastructure, energy and transportation sectors.Sustainable financing loans rose 31% year-on-year to S$50 billion and accounted for 16% of Group loans, while total commitments increased 27% to S$71 billion.

- As at 31 December 2024, customer deposits rose 7% from a year ago to S$391 billion, from higher CASA and fixed deposits. Loans-to-deposits ratio was 80.7%, as compared to 80.5% a year ago.

- The Group’s CET1 CAR is subject to MAS’ final Basel III reforms requirements which came into effect on 1 July 2024 and are being progressively phased in between 1 July 2024 and 1 January 2029. Group CET1 CAR as at 31 December 2024 was 17.1%, and was 15.3% on a fully phased-in basis.

- The Board has recommended a final ordinary dividend of 41 cents per share for FY24.

- Together with the interim dividend, total ordinary dividend for FY24 will be 85 cents per share, higher than the 82 cents for FY23. The total payout will amount to S$3.82 billion, which is in line with the Group’s target payout ratio of 50%.

- A special dividend of 16 cents per share is proposed, bringing total dividend to S$1.01 per share, which represents a total payout ratio of 60% for FY24.

- The Scrip Dividend Scheme will not be applicable to the final ordinary and special dividend.

Message from Group CEO, Helen Wong

“I am pleased to report that OCBC has delivered a record profit for the third year in a row. Our well- diversified Banking, Wealth Management and Insurance franchise all contributed to total income reaching an all-time high this year. We effectively managed expenses with continued cost discipline, while strategically investing to drive growth. Our proactive and prudent risk management has kept our portfolio quality healthy and credit costs low.

We deployed capital to increase our stake in Great Eastern Holdings (“GEH”) to 93.72%. GEH has significantly contributed to OCBC’s performance and is a strategic pillar of OCBC’s wealth management business, while OCBC has provided GEH access to our extensive retail and commercial customer base. We also successfully integrated PT Bank Commonwealth, which strengthened our customer and talent base in Indonesia.

The Bank has set out a comprehensive plan to deliver capital returns through a combination of ordinary and special dividends, as well as share buybacks. This signifies our confidence in driving OCBC’s long-term growth, while affirming our commitment to rewarding our shareholders for their continued support of OCBC.

As we enter the new year, we remain cautiously optimistic on the regional growth outlook and are poised to seize growth opportunities as they arise. We will remain agile in navigating the increasingly complex geopolitical landscape, and volatile macroeconomic environment. We firmly believe our collective strength as One Group is key to steering OCBC to greater heights. With OCBC’s well-established franchise, prudent risk management and robust capital, we are confident in our ability to continue delivering strong results and long-term value to all stakeholders.”