OCBC Group Third Quarter 2024 Net Profit Rose 9% from the Previous Year to S$1.97 billion

OCBC Group Third Quarter 2024 Net Profit Rose 9% from the Previous Year to S$1.97 billion

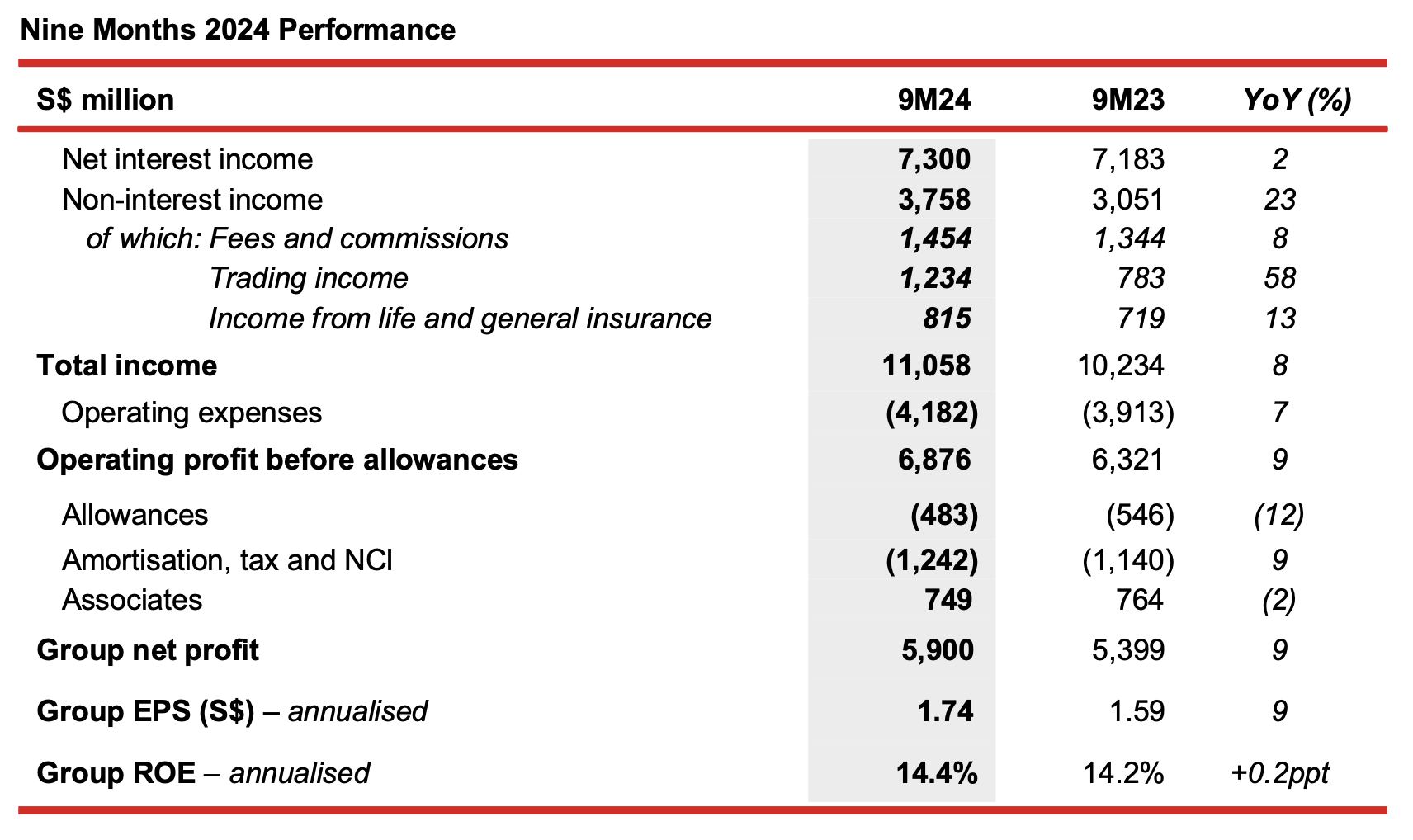

Nine months 2024 net profit up 9% to a new high of S$5.90 billion

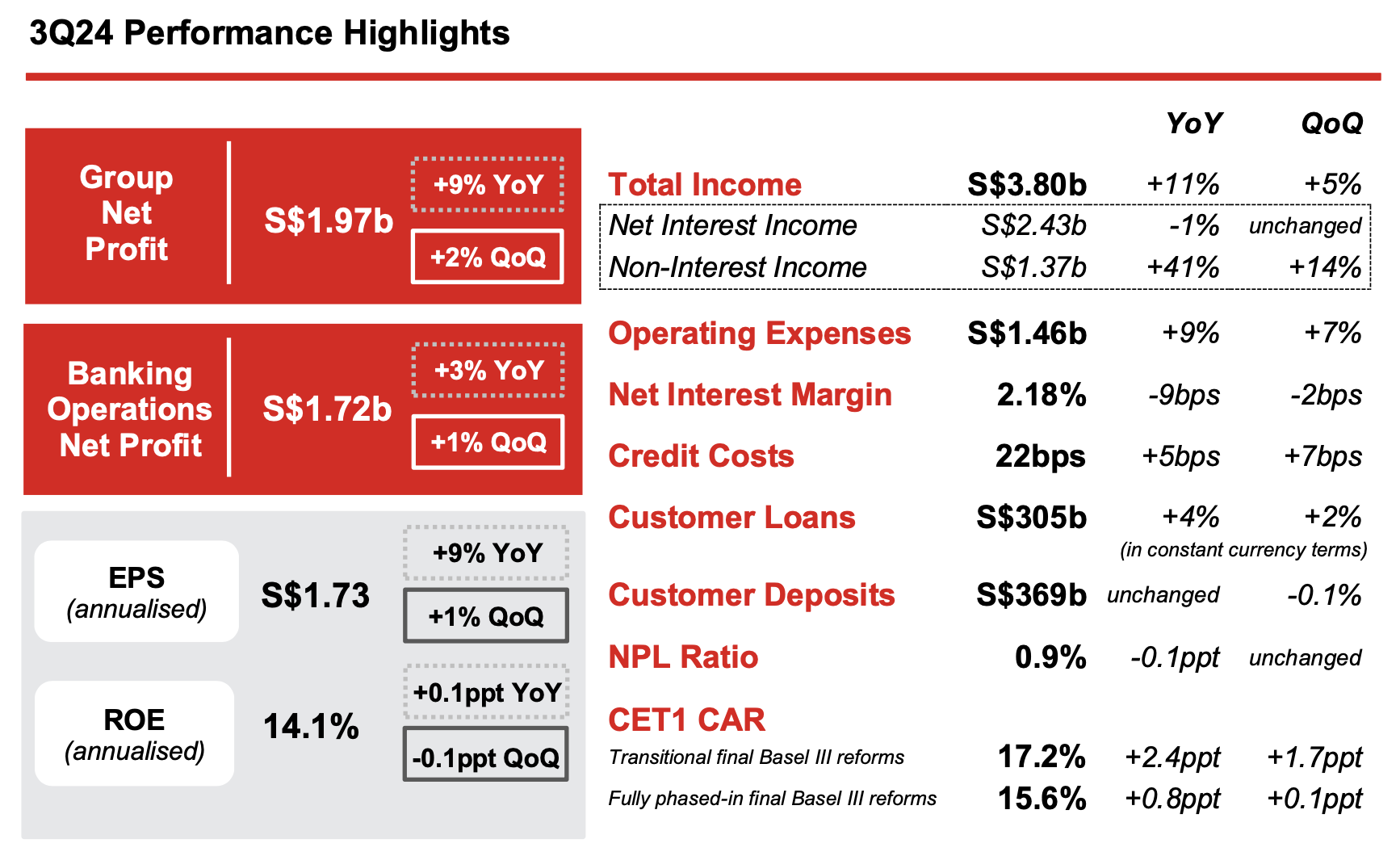

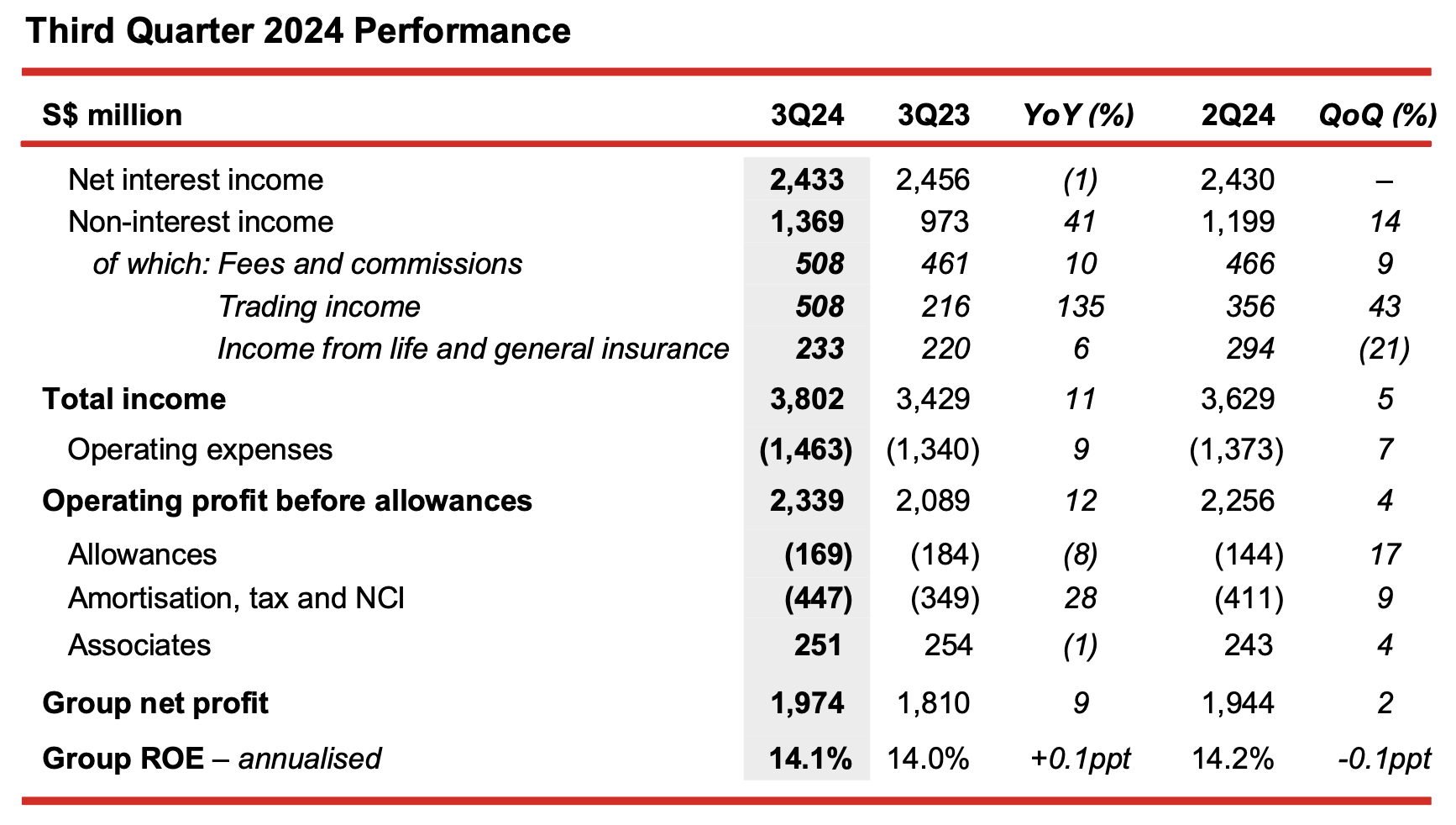

Singapore, 8 November 2024 – Oversea-Chinese Banking Corporation Limited (“OCBC”) reported net profit of S$1.97 billion for the third quarter of 2024 (“3Q24”), 9% higher than S$1.81 billion in the previous year (“3Q23”), and 2% above S$1.94 billion a quarter ago (“2Q24”). Net profit for the nine months of 2024 (“9M24”) increased 9% from a year ago (“9M23”) to S$5.90 billion.

The Group’s strong year-on-year performance for 3Q24 was driven by robust non-interest income growth and lower allowances. Increased wealth management activities lifted fee and trading income, with insurance income higher as well. Cost-to-income ratio (“CIR”) improved from the previous year to 38.5% on positive operating jaws. Asset quality remained resilient with non-performing loan (“NPL”) ratio declining to 0.9%. Customer loans grew 4% from a year ago, on a constant-currency basis. On an annualised basis, return on equity rose to 14.1% and earnings per share increased to S$1.73.

3Q24 Year-on-Year Performance

Group net profit rose 9% from a year ago to S$1.97 billion, led by higher non-interest income and lower allowances.

- Net interest income was S$2.43 billion, 1% lower than 3Q23. Average assets grew 3% while net interest margin (“NIM”) compressed by 9 basis points to 2.18%, as the rise in funding costs more than offset the higher asset yields.

- Non-interest income grew 41% to S$1.37 billion from broad-based growth.

- Net fee income rose 10% to S$508 million, underpinned by higher wealth management, investment banking and loan-related fees. In particular, wealth management fees climbed 25% from a year ago, reflecting increased customer activities across all wealth product channels.

- Net trading income more than doubled to a new quarterly high of S$508 million. Customer flow treasury income rose to a record S$306 million, driven by both corporate and wealth segments. Improved investment performance across Global Markets and Great Eastern Holdings (“GEH”) lifted non-customer flow treasury income.

- Insurance income from GEH increased 6% to S$233 million, supported by robust underlying business performance.

- The Group’s wealth management income, comprising income from private banking, premier private client, premier banking, insurance, asset management and stockbroking, was S$1.29 billion, 15% higher than the previous year, and contributed 34% to the Group’s total income. Group wealth management AUM was S$284 billion, up 5% from S$270 billion a year ago from both net new money inflows and improved market valuation.

- Operating expenses were S$1.46 billion, up 9% year-on-year. This was underpinned by higher expenses associated with increased business volumes, as well as IT-related expenses as the Group continued to drive its digitalisation initiatives. During the quarter, S$15 million of costs relating to the integration of PT Bank Commonwealth (“PTBC”) in Indonesia were also recorded. As income growth outpaced the increase in expenses, CIR improved to 38.5%.

- Total allowances dropped 8% from a year ago to S$169 million.

- Share of results of associates was S$251 million, 1% below 3Q23.

3Q24 Quarter-on-Quarter Performance

Group net profit of S$1.97 billion was 2% higher than the previous quarter.

- Net interest income of S$2.43 billion held steady from a quarter ago. The effect of a comparatively longer quarter compensated for the impact of a 2-basis point narrowing of NIM.

- Non-interest income grew 14% to S$1.37 billion from the prior quarter, driven by stronger fee and trading income. Net fee income was up 9%, largely attributable to a 16% increase in wealth management fees, and higher investment banking and loan-related fees. Net trading income rose by 43% from 2Q24.

- Operating expenses were 7% above 2Q24, led by a rise in variable staff compensation linked to higher business volumes.

- Total allowances of S$169 million were higher as compared to S$144 million in the previous quarter, largely from higher allowances for non-impaired assets.

- Share of results of associates rose 4% from 2Q24 to S$251 million.

9M24 Year-on-Year Performance

Group net profit increased 9% to S$5.90 billion, surpassing the previous nine-month high reported a year ago. This was driven by broad-based income growth and lower allowances.

- Net interest income grew 2% to a record S$7.30 billion, backed by a 4% rise in average assets from growth in customer loans and the deployment of liquidity into high-quality assets which were income- accretive but lower yielding. NIM contracted 6 basis points to 2.22%, mainly due to increased funding costs which outpaced the rise in asset yields.

- Non-interest income rose 23% to a new high of S$3.76 billion. Net fee income grew 8% to S$1.45 billion, largely attributable to a 21% increase in wealth management fees. Net trading income was 58% higher at S$1.23 billion, driven by both customer and non-customer flow income. Insurance income improved by 13% to S$815 million.

- Operating expenses were S$4.18 billion, 7% higher as compared to 9M23, largely due to increased staff costs and IT-related expenditure to support the Group’s business expansion. Integration costs of S$27 million for PTBC were also included in 9M24. CIR improved to 37.8% from 38.2% a year ago, as the 8% rise in total income exceeded expense growth.

- Share of results of associates was S$749 million, 2% lower than a year ago.

- Total allowances were S$483 million, 12% below S$546 million in 9M23, mainly due to a decline in allowances for non-impaired assets.

- On an annualised basis, ROE rose to 14.4% from 14.2% in the previous year, and earnings per share grew 9% to S$1.74.

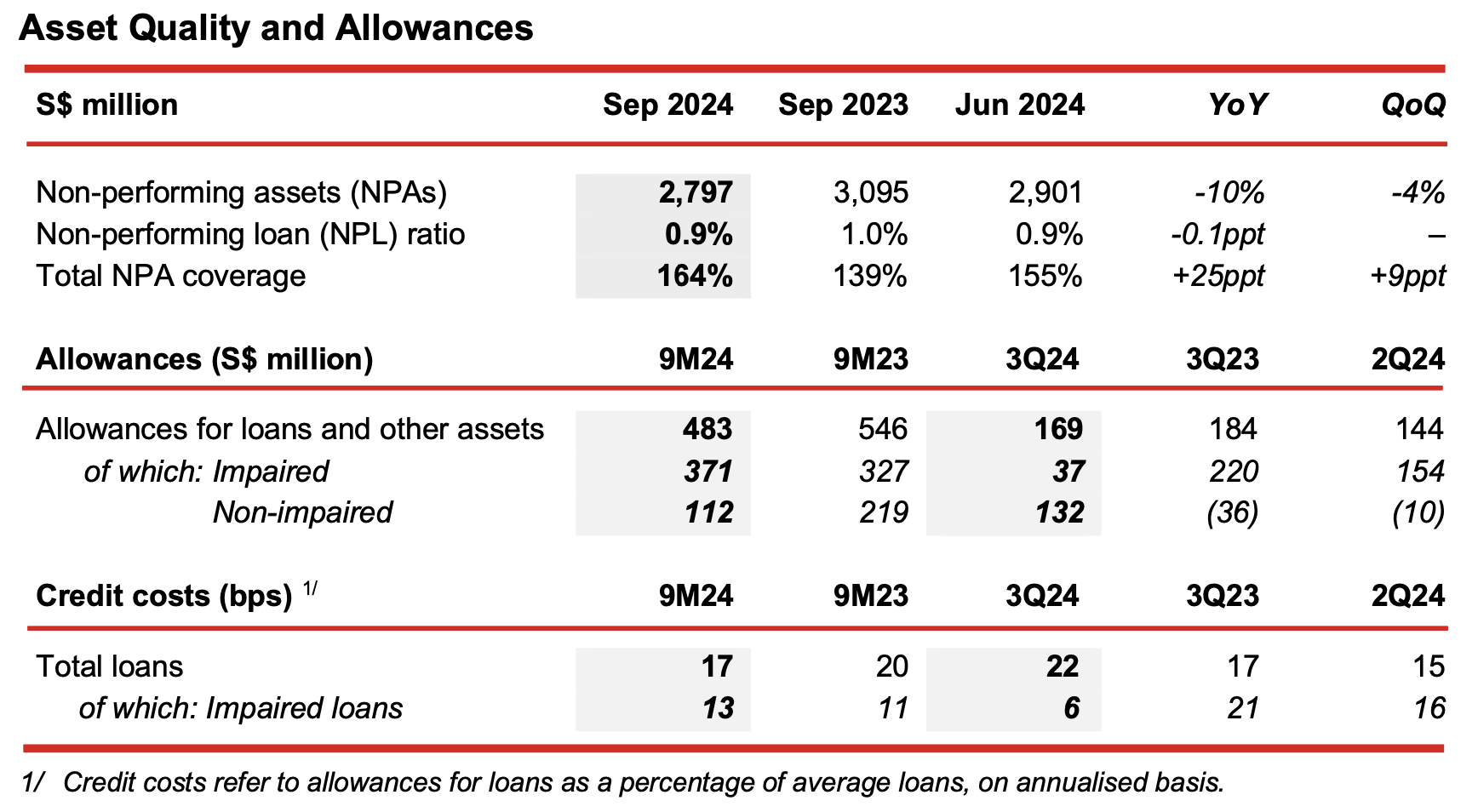

- Total NPAs as at 30 September 2024 were S$2.80 billion, 10% below the previous year and down 4% from the last quarter. The quarter-on-quarter drop in NPAs was driven by higher recoveries/upgrades and write-offs, which more than compensated for a rise in new corporate NPAs.

- NPL ratio was 0.9%, lower than a year ago and unchanged from the prior quarter. The allowance coverage for total NPAs was 164%, as compared to 139% in the previous year.

- Total allowances for 3Q24 were S$169 million, which comprised allowances for impaired assets of S$37 million and allowances for non-impaired assets of S$132 million.

- On an annualised basis, total credit costs for 9M24 were 17 basis points, lower as compared to 20 basis points in 9M23.

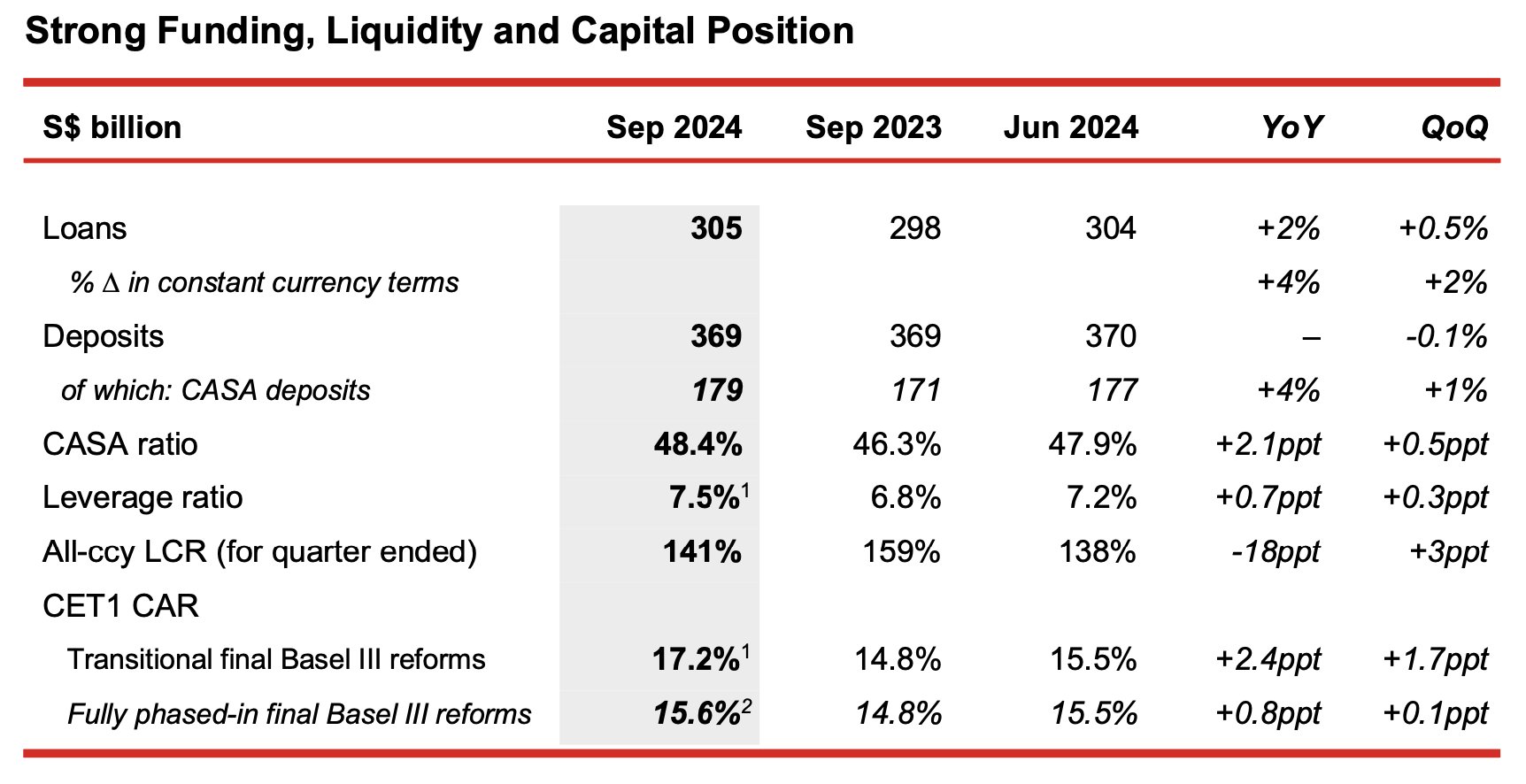

- Customer loans grew 4% from a year ago and 2% from the previous quarter in constant currency terms, to S$305 billion as at 30 September 2024.

- The year-on-year loan growth was led by an increase in corporate loans and mortgages. By geography, loan growth was largely driven by Singapore, Malaysia, and the Group’s international markets including the United Kingdom and Australia.

- Sustainable financing loans rose 31% from year ago to S$47.1 billion, and comprised 15% of total customer loans. The total sustainable financing loan commitments stood at S$64.7 billion as at 30 September 2024.

- Customer deposits of S$369 billion were lower than a quarter ago, mainly driven by a S$3 billion drop in higher-cost fixed deposits. CASA deposits increased to S$179 billion and CASA ratio rose to 48.4%.

- Loans-to-deposits ratio was 81.6%, higher as compared to 79.7% in the previous year and 81.1% in the prior quarter.

- The Group is subject to MAS’ final Basel III reforms requirements which came into effect on 1 July 2024, and are being progressively phased in between 1 July 2024 and 1 January 2029. Group CET 1 CAR as at 30 September 2024 was 17.2%, and was 15.6% on a fully phased-in basis.

Message from Group CEO, Helen Wong

“Our record earnings for the first nine months of 2024 underscored the robust performance across the Group’s diversified franchise. Loan growth momentum was sustained as we supported customers across our markets, while portfolio quality remained sound. The strong improvement in our wealth management business and trading income reflected the progress we have made in advancing our corporate strategy. We also saw solid profit contribution from Great Eastern Holdings (GEH), and we look forward to driving further collaboration and synergies with GEH.

Our shareholding in GEH is 93.72% after the expiry of GEH minority shareholders’ right under Section 215(3) of the Companies Act on 23 October 2024. I am pleased that we have also completed the merger between OCBC Indonesia and PT Bank Commonwealth in September 2024.

Looking ahead, we will continue to proactively manage our balance sheet to prepare for a lower interest rate environment. We are closely monitoring potential volatilities arising from uncertain geopolitical conditions. We remain confident in the resilience and long-term prospects of our key markets in Asia. With our well-established franchise and strong financial position, we are well-placed to drive value for all stakeholders.”