Review by

Our Group CEO

Ms Helen Wong

Group Chief Executive Officer

Dear Fellow Shareholders,

I am pleased to report another record set of results. Building on the strengths of OCBC's unique makeup as one integrated financial services group, we were firing on all cylinders. This momentum continues from 2022, the year we launched our corporate strategy. Since then, with your unwavering support, we have been successfully executing this strategy.

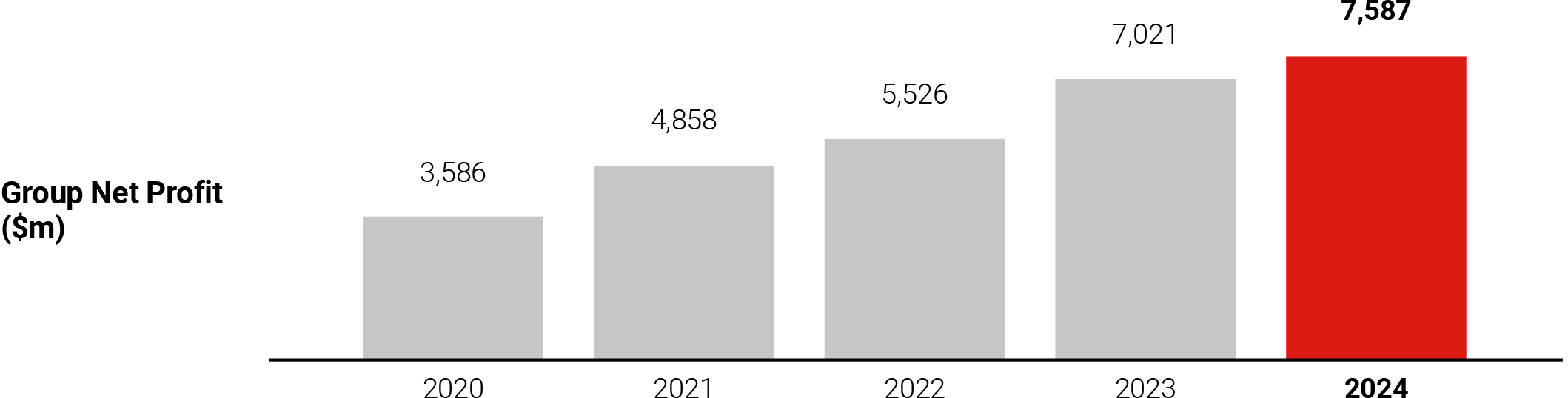

OCBC delivered sustained earnings momentum, with 2024 net profit rising 8% from a year ago to $7.59 billion. This marks our third record year in a row, which validates our strategy and reflects the meaningful advancements made towards delivering long-term shareholder value. The strong performance was achieved across our Banking, Wealth Management and Insurance businesses, which clearly underlines the advantages our diversified franchise.

Let me take you through our key earnings drivers for 2024. Total income rose 7% to a record $14.5 billion, fuelled by net interest income hitting an all-time high and solid non-interest income growth. While interest rates have trended down in 2024 as reflected by our lower net interest margin of 2.20%, our asset growth, proactive balance sheet management and well-diversified customer deposit franchise enabled us to defend net interest income effectively, which increased 1% to $9.76 billion. Non-interest income surged 22% to $4.72 billion, propelled by customer-driven growth. Wealth management fees were up 22%, underpinned by a rise across all our wealth channels.

Our trading income reached a new high, while insurance income increased 14%. At the same time, we were focused on investing in strategic initiatives and business expansion, but still delivered a cost-to-income ratio of below 40%.

Loans grew by a robust 8% to $319 billion for 2024, lifted by broad-based growth across all our core markets and key international markets, as we supported customers as One Group across our network. We grew our mortgages, and increased lending to customers in the new economy sectors such as technology and digital infrastructure, as well as in the energy and transportation industries. Sustainable financing loans grew 31% to $50 billion and accounted for 16% of our Group loans, while total commitments stood at $71 billion. We continued to be prudent in our risk management approach and asset quality remained resilient. Our 2024 Non-Performing Loan ratio improved to 0.9%, from 1.0% a year ago. Total allowances were 6% lower while Non-Performing Assets coverage ratio improved to 159%.

We ended 2024 with a strong balance sheet. Our funding, capital and liquidity positions were all robust. Common Equity Tier 1 Capital Adequacy Ratio (CET1 CAR) increased from 15.9% a year ago to 17.1%, led by a reduction in risk-weighted assets largely attributable to the adoption of MAS' final Basel III reform rules, effective on 1 July 2024. On a fully phased-in basis, our CET1 CAR would be 15.3%.

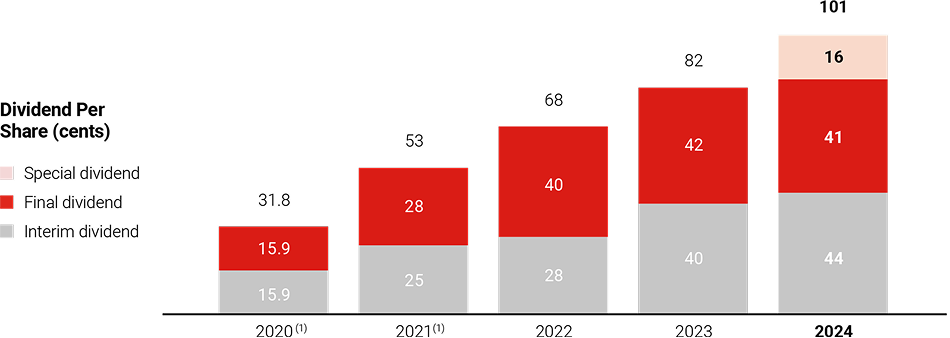

Given the consistently solid performance of our Group franchise and strong capital position, we want to continue to reward our shareholders for their support. Now that we have greater clarity on our capital plan , we announced a comprehensive approach to return $2.5 billion of capital back to shareholders over two years. This comprises paying out 10% of 2024 and 2025 Group net profit as special dividends, with the remaining of the $2.5 billion returned via share buybacks over two years, subject to market conditions and regulatory approvals. Combined with our target 50% ordinary dividend payout ratio, our shareholders will enjoy a 60% total dividend payout annually in 2024 and 2025. This allows shareholders to share in the growth of OCBC.

This 60% dividend payout is reflected in our 2024 total dividends. The Board has recommended a 16 cents special dividend per share and a final ordinary dividend of 41 cents per share. Together with the interim dividend, total 2024 dividends will amount to $1.01 per share, 23% above 2023. Our total shareholder returns have doubled over a five-year period as at end-2024, and the $2.5 billion capital return will further enhance returns to shareholders. This underscores our commitment to drive long-term value for you.

Winning as One Group

While OCBC is often associated with banking, we are much more than that. Together with the largest insurer in Singapore and Malaysia, a leading asset management company in Southeast Asia, and a standalone private bank that operates on the global stage, the OCBC Group offers a complete solution to our customers spanning banking, wealth management, insurance, and asset management.

This composition and synergistic nature of OCBC Group is not easily replicated. It is the result of a series of deliberate, strategic moves over decades.

Take our wealth management franchise for example. We are one of the biggest players, if not the biggest, in the region by assets under management when you combine OCBC Bank, Bank of Singapore and Great Eastern Holdings. But it was actually not too long ago – in 2010 – that Bank of Singapore was formed, following the acquisition of ING Asia Private Bank. Since then, Bank of Singapore has grown from strength to strength on the back of other acquisitions, as well as its synergy with OCBC Bank in supporting the entire wealth continuum. A customer can start in our consumer bank, move up from the personal segment, to Premier Banking and Premier Private Client, and then to Bank of Singapore. Some of Bank of Singapore's customers who are entrepreneurs are referred from our Global Wholesale Banking division, and vice versa. Referrals are also coming from Great Eastern Holdings.

This brings me to the importance of Great Eastern Holdings' role in the Group, especially within our wealth management franchise. Owning more of Great Eastern Holdings is to enable it to be tightly integrated with our banking units, relative to commercial bancassurance arrangements. With full alignment of strategic direction across the Group, we will be able to provide a comprehensive suite of banking, wealth, health and protection products, not just to banking customers, but also to the customers of Great Eastern Holdings.

As we continue to strengthen integration between OCBC banking units and Great Eastern Holdings, I expect stronger growth in new customer numbers, product sales and share of wallet.

It is a long-standing conviction of ours that we can achieve much more when Great Eastern Holdings is a close-knit part of the Group. Great Eastern Holdings was an associate company in 1958 and is now one of our principal subsidiaries in which we hold a close to 94% stake. This follows our $1.4 billion voluntary unconditional general offer in 2024, which was for the 11.56% stake in Great Eastern Holdings that we did not own at the time. Long-time market watchers would not have been surprised by this as it built on earlier efforts to bring Great Eastern Holdings further into the fold. In 2004, we had increased our stake in Great Eastern Holdings to 81.1%, up from 48.8%. We then progressively increased our stake leading up to 2024. Today, OCBC's stake in GEH is 93.72%.

Great Eastern Holdings is a strong earnings contributor to the OCBC Group, which hit as high as 22% over the last decade. It is also accretive to OCBC's return on equity and provides risk diversification across our businesses. With our increased ownership and consolidation of Great Eastern Holdings, our Group earnings are enlarged, allowing us to deliver higher returns to shareholders.

You can see from the charts that our One Group strategy has helped us to grow and enhance shareholder value over the long run. This is especially so in the last few years. We remain steadfast in our belief that this is the right way forward.

Capturing opportunities in ASEAN and Greater China

Our One Group capabilities are very much focused in ASEAN and Greater China. This is the right place to be, now and for the future.

The importance of these two regions stems from rising intra-Asia trade and investment flows. Since 2019, ASEAN has surpassed the European Union to become China's largest trading partner. China-ASEAN bilateral trade accounts for about 15% of China's total goods trade, which is significant especially considering the size of the Chinese economy.

Yes, the onset of Trade War 2.0 under the Trump administration does bear watching, but with ongoing supply chain diversification, ASEAN continues to benefit from inflows of foreign direct investments. Outbound foreign direct investments from China into ASEAN should remain robust.

Indeed, what we see is an evolving China plus one strategy into a China plus n strategy. China and China-based companies are diversifying supply chains across multiple markets. Our Chinese customers are investing in Vietnam for general manufacturing and in Malaysia for advanced manufacturing. They also value Indonesia's large population and natural resources. At the heart of it are Singapore and Hong Kong SAR. Many Chinese companies make Hong Kong SAR their first stop for fundraising. As they expand into ASEAN, they turn to Singapore as a hub for financing and managing investments in the region.

As a Singapore-headquartered bank with Hong Kong SAR as a twin hub, and more than 400 branches and representative offices in ASEAN and Greater China, we are therefore very well-positioned for this opportunity. Not forgetting our associate company Bank of Ningbo, which has a complementary network of around 480 branches, sub-branches and offices in mainland China. Their customer base suits us well as they bank a lot of the medium-sized, export-oriented companies that are already looking to expand outside of China.

We have thus been successful in "following the flow", supporting Chinese businesses into Hong Kong SAR and Singapore, and then into other parts of ASEAN. In 2024, we saw an almost 30% year-on-year increase in new-to-bank customers who are Chinese companies coming to ASEAN.

Wealth flows within Asia are also rising. Over the last decade, depending on which Asian country you are in, GDP may have grown by around 5%, say in Indonesia. Individuals then invest, and their wealth grows faster. We have observed more of our customers entering the ranks of the wealthy as a result. Therein lies the opportunity for us to grow our Premier Banking segment under consumer banking to serve these customers. Already, in Hong Kong SAR, our Premier Banking customer base grew more than 35% year-on-year. In Indonesia, it was close to 20%. As more customers turn to digital means to manage their wealth, this is an increasingly important play for us too. Improvements to the OCBC app including to the wealth dashboard contributed to an over 70% increase year-on-year in Singapore digital wealth revenue.

Bank of Singapore has likewise seen strong growth, recording double-digit growth in assets under management in two of its key client segments – ultra-high net worth individuals and financial intermediaries. Notably, there was strong momentum in alternative investments, with 80% growth in inflows compared to a year ago.

While the opportunities in Asia are broad based, I am sometimes asked if I see specific pockets of opportunities. To this, I would say that Indonesia is a market worth watching. It is with this belief that we completed our acquisition and integration of PT Bank Commonwealth (PTBC) last year. We already had a strong wealth presence through OCBC Indonesia, and PTBC enhances this with demonstrated wealth management capabilities and a complementary base of customers, whom we have now welcomed into the OCBC family.

Investing and transforming for the future

While we are confident about our One Group strengths across Greater China and ASEAN, we are mindful of the competition. Deepening our advantage is therefore a priority.

To that end, we announced a HK$1.5 billion ($260 million) investment over three years to shore up our technology platforms and facilities across Greater China. We have also embarked on expanding our regional engineering hub in China to attract top tech engineering talents. These complement our other investments which aim to boost our capabilities in the region. Over the years, we have expanded our Greater China Business Office network to cover Singapore, Malaysia, Thailand, Indonesia and Vietnam. And in tandem with the development of the Johor-Singapore Special Economic Zone, we have set up cross-border dedicated teams in Singapore and Malaysia to support our small and medium enterprise (SME) customers that want to start and grow their businesses in this zone. Meanwhile, Bank of Singapore is on track to hit its target relationship manager strength of 500 by 2025 globally.

We formed a new division in 2024 — Group Strategy and Transformation Office (Group STO) — led by Group Chief Strategy and Transformation Officer. Group STO will drive the Group's strategy, innovation, and transformation, underpinned by data, customer-centricity, and operational excellence.

While this may be a new division, we are no strangers to transformation and innovation. Artificial Intelligence (AI) is a good example; our AI Lab unit, which today is part of Group STO, was first established in 2018 and gave us a good grounding. We are in a good position to leverage AI – in particular, Generative AI. While relatively low on the maturity scale in terms of business adoption, compared to cloud computing or applied AI for example, we have seen early successes and have strong conviction in its business value. We envision it can hyper-personalise wealth recommendations and enhance productivity, allowing our colleagues to focus on higher-value tasks. So far, we have deployed over 30 Gen AI applications to boost productivity, creating up to 50% productivity gains for some tasks.

This is just the beginning for AI. We see new “reasoning models” such as DeepSeek giving the ability to tackle complex problems by thinking through steps and providing detailed explanations. The human-like logical reasoning will allow AI to support deeper analysis and nuanced decision-making which can help in advanced processes like financial needs analysis.

2024 also saw us make a major commitment to accelerating innovation – a $500 million investment in Singapore's Punggol Digital District (PDD). This will fund our innovation hub, OCBC Punggol, set to be completed in the first quarter of 2027. The investment includes a strategic partnership with Singapore Institute of Technology (SIT), which will drive fintech innovation and nurture talent through a learning lab and scholarships. Hopefully through this, we can attract some of SIT's top talents too. This investment complements our seven-year digital core roadmap to modernise our technology architecture, with over $250 million invested in the first phase from 2019 to 2022 and an additional $300 million planned for the second phase from 2023 to 2025.

Equally important to OCBC Group's future is climate change. In 2023, we unveiled our sectoral net-zero targets as part of our commitment to achieve net zero in financed emissions by 2050. Steady progress has been made since then. Sustainable finance has become business-as-usual, with our sustainable finance loan commitments reaching $71 billion at the end of 2024. The conversations with our customers are becoming deeper. We are discussing transition efforts, which is important especially for those in hard-to-abate sectors. SMEs are crucial to managing this climate crisis too. At end 2024, we were supporting close to 4,000 SMEs across the region with sustainable financing.

While we must move quickly with our transformation efforts, I would like to emphasise the importance of having our Purpose and Values at the heart of every decision. That is non-negotiable. We have and will always put our customers, community and shareholders first.

Appreciation

2024's stellar results reflect the hard work and expertise of over 30,000 colleagues at OCBC Group. I extend my heartfelt thanks and congratulations to them, including my capable management team. Our achievements also owe much to the stewardship of our Chairman and the Board of Directors, whose support have been invaluable. We are grateful to our customers and the communities we serve too, as their support has shaped OCBC into what it is today.

Last but certainly not least: to you, our shareholders, thank you for your trust on this journey. We look forward to building a stronger OCBC Group together.

Helen Wong

Group CEO

February 2025

Note: 2022 was restated with the adoption of SFRS(I)17. Comparatives for 2019 to 2021 were not restated.

Note: In July 2020, the MAS called on locally-incorporated banks headquartered in Singapore to cap total dividends per share for 2020 at 60% of that for 2019. In July 2021, the dividend cap was lifted for the 2021 dividend.